In this blog, the third in our introduction to the S&P High Yield Dividend Aristocrats®, we will cover sector composition, performance attribution, and factor exposure.

Sector Composition

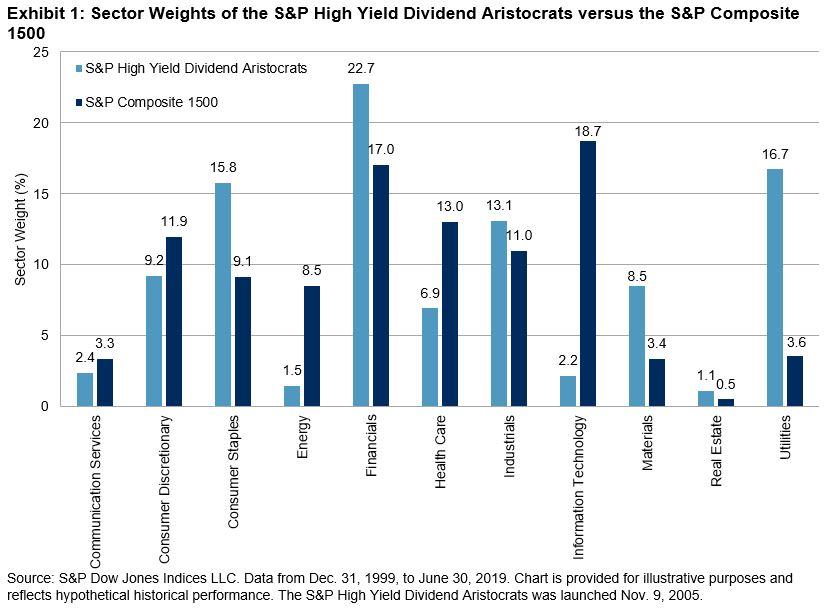

As shown in Exhibit 1, the S&P High Yield Dividend Aristocrats has diversified sector exposures, with some sector bets, given different dividend-paying practices among sectors. Historically, the S&P High Yield Dividend Aristocrats has had higher exposure to the Financials, Utilities, Consumer Staples, Industrials, and Materials sectors, in terms of absolute weight and weights relative to the S&P Composite 1500®. In contrast, the index has had much lower exposures to the Energy, Information Technology, and Health Care sectors.

Performance Attribution

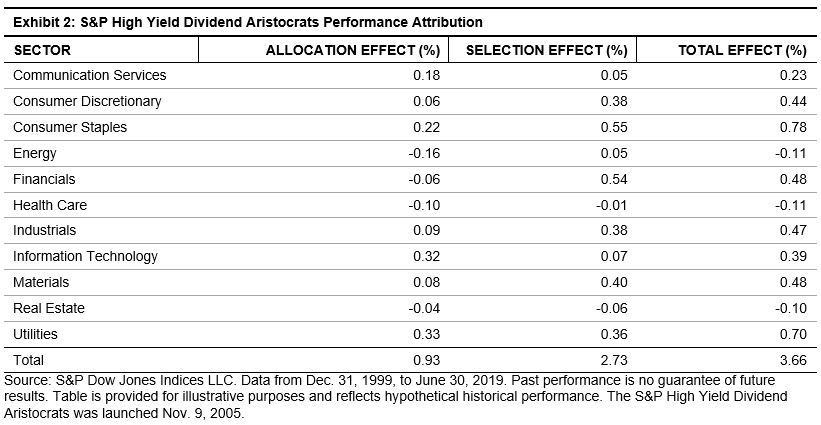

We analyze the sources of the historical excess returns of the S&P High Yield Dividend Aristocrats versus the S&P Composite 1500. Grouping by sectors, we look at the sector allocation[1] and individual stock selection effects (see Exhibit 2).

Performance attribution shows that individual stock selection contributed to 75% of monthly active returns, while sector allocation contributed to 25%. Thus, the outperformance of the S&P High Yield Dividend Aristocrats mainly came from stock selection rather than sector allocation.

Factor Exposures

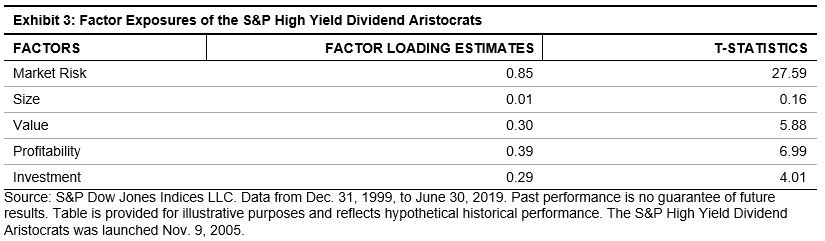

We used the Fama-French Five-Factor Model[2] to dissect the historical returns of the S&P High Yield Dividend Aristocrats (see Exhibit 3). From the factor loading estimates and associated t-statistics, we can see that the S&P High Yield Dividend Aristocrats constituents had positive exposures to lower beta, better value, higher operating profitability, and more conservative investment growth. Profitability and investment growth are considered to be quality factors.

The empirical results show that the constituents had better valuation and quality characteristics than the overall market. From business operations and financial perspectives, high quality fundamentals form the foundation for consistent dividend increase.

From our three-blog installment, we can conclude that the S&P High Yield Dividend Aristocrats has consistently had higher yields than its benchmark. Further, performance attribution and factor exposure analyses showed that the strategy’s outperformance was mainly due to stock selection and that its constituents have had good value and quality characteristics. In return, such solid fundamentals have driven its long-term favorable risk-adjusted returns and defensive characteristics.

For more information, see the two previous blogs in the installment.

- S&P High Yield Dividend Aristocrats Part I: Strategy Characteristics

- S&P High Yield Dividend Aristocrats Part II: Risk/Return

[1] The sector allocation effect is the portion of portfolio excess return attributed to taking on sector bets in comparison with the benchmark. Individual stock selection effect is the portion of portfolio excess return attributable to individual stock selection when the sector weight is the same as that of the benchmark.

[2] Fama, E. and K. French. “Dissecting Anomalies with a Five-Factor Model.” The Review of Financial Studies, Volume 29, Issue 1, 2016, pp. 69-103.

The posts on this blog are opinions, not advice. Please read our Disclaimers.