One of the classic scenes from the original Top Gun movie recounts the exchange Maverick (Tom Cruise) had with a MiG-28. Maverick corrects Charlie’s (Kelly McGillis) intelligence report on the Russian fighter jet with his eyewitness account. When she asks how he saw a MiG-28 perform a 4G dive from above, he responds: “Because I was inverted.” Goose (Anthony Edwards) interrupts Mav that it was “we,” not “I.”

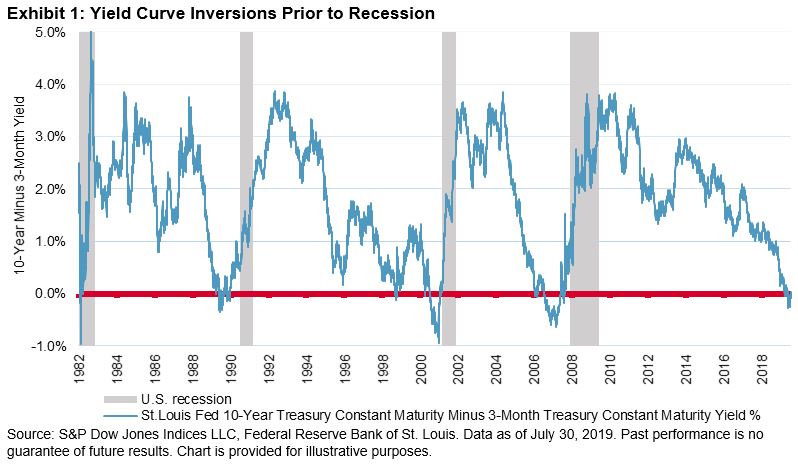

Fed Chairman Jerome Powell could have responded the same way when asked why he cut rates today. The treasury yield curve was inverted for the first time since the dark days of 2007. This is cause for alarm as the previous three recessions occurred after the 10-year U.S. Treasury Note yield fell below the three-month yield, as is the case today.

By cutting rates, the Fed is hoping to be ahead of the curve to stave off another recession. History has shown precedent for this. Looking at the S&P U.S. Treasury Current 10-Year Index yield minus the S&P U.S. Treasury Current 2-Year Index yield, the curve inverted the previous two recessions, but it hasn’t fallen below zero in the current cycle, unlike the 10-year/3-month curve.

Then there’s the Maestro. It was former Fed Chair Alan Greenspan’s deft use of the overnight rate during the previous longest bull market in history that gave him the nickname “Maestro” (not less brave than Maverick’s move, by the way). In 1994, Greenspan cut rates despite the strong equity market performance. The S&P 500® climbed 88% from the October 1990 lows and it rallied another 42% before the Fed would tighten monetary policy again. With a bull market long in the tooth and a similar political landscape (an incumbent gearing up for his reelection campaign), Jerome Powell is taking a page out of the Maestro’s songbook by cutting before the yield curve inverts.

History has shown that maintaining exposure to equities during an easing cycle can still be profitable despite substantial prior gains. Throughout the 1990s, Greenspan cut rates a total of 23 times. The S&P 500 responded positively each time, averaging a 16% annual return following each cut. However, his same approach did not work as well in the 2000s after the yield curve inverted and the bull market ended.

It remains unclear whether the Fed is channeling the Maverick move by pushing the limits or Alan Greenspan’s “Maestro” of the 1990s with sustained economic success. Market participants can only wait to see what the consequences of the Fed’s moves might be. For now, investors will have to follow the bond market for clues on the next Fed move.

The posts on this blog are opinions, not advice. Please read our Disclaimers.