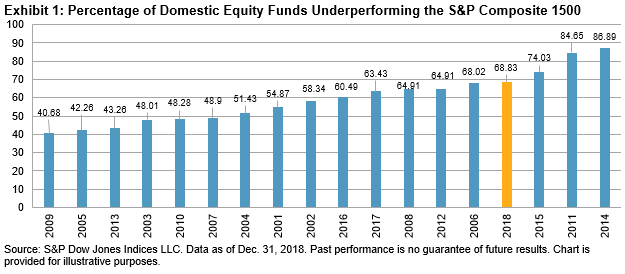

Contrary to the myth that active managers tend to fare better than their benchmarks during volatile markets, 68.83% of domestic equity funds lagged the S&P Composite 1500® during the one-year period ending Dec. 31, 2018, making 2018 the fourth-worst year for active U.S. equity managers since 2001 (see Exhibit 1).

Evidence from the SPIVA U.S. Year-End 2018 Scorecard puts a question mark over the ability of active managers to generate alpha during market turmoil. In 2018, heightened volatility accompanied by below-average dispersion might have handcuffed active managers in terms of stock picking, and the investment outcome in general seemed more random than usual, as indicated by a relatively large standard deviation of return distribution.

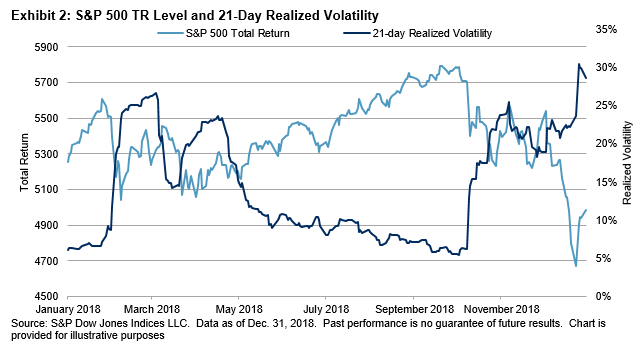

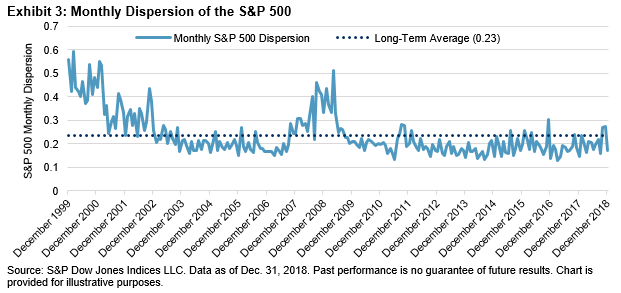

Last year was a rollercoaster ride for financial markets (see Exhibit 2). The S&P 500® (-4.38%) finished 2018 with its first calendar-year loss in a decade, while the S&P MidCap 400® (-11.08%) and the S&P SmallCap 600® (-8.48%) posted even larger losses. Despite elevated volatility levels in 2018, monthly dispersion—the difference between winners and losers—of the S&P 500 remained generally below its long-term average since 2009 (see Exhibit 3). The combination of high volatility and low dispersion in 2018 created a challenge for active managers to generate alpha through stock selection.

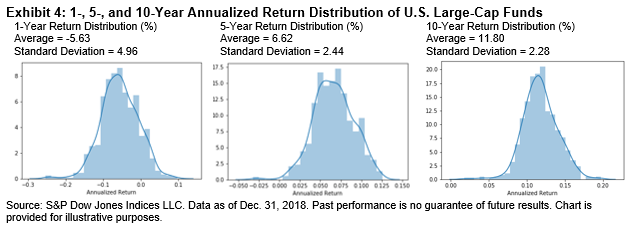

Outcomes from active investment decisions in 2018’s market conditions seemed more random than usual. The one-year return distribution of all U.S. large-cap funds showed higher standard deviation compared with medium- and long-term distributions (see Exhibit 4).

For the ninth consecutive year, the majority (64.49%) of large-cap funds underperformed the S&P 500. Similarly, small-cap equity managers found it more challenging to navigate 2018’s market environment compared with 2017’s range-bound market movements; 68.45% of all small-cap funds lagged the S&P SmallCap 600 over the one-year horizon. Mid-cap mutual funds fared better; for the second consecutive year, the majority (54.36%) beat the S&P MidCap 400. Over the fifteen-year investment horizon, however, 80% or more of active managers across all categories underperformed their respective benchmarks.

The posts on this blog are opinions, not advice. Please read our Disclaimers.