For most of 2018, the S&P 500 Low Volatility Index® underperformed its parent S&P 500. Through the first nine months of 2018, the S&P 500 climbed 11% while the S&P 500 Low Volatility Index was up only 6%. Then October came and, in one month of acute volatility, the low volatility index recaptured parity with the benchmark. Both indices were up around 3% year to date through Oct. 31, 2018. (This reversal trend continued into November and the S&P 500 Low Volatility Index now has the lead.)

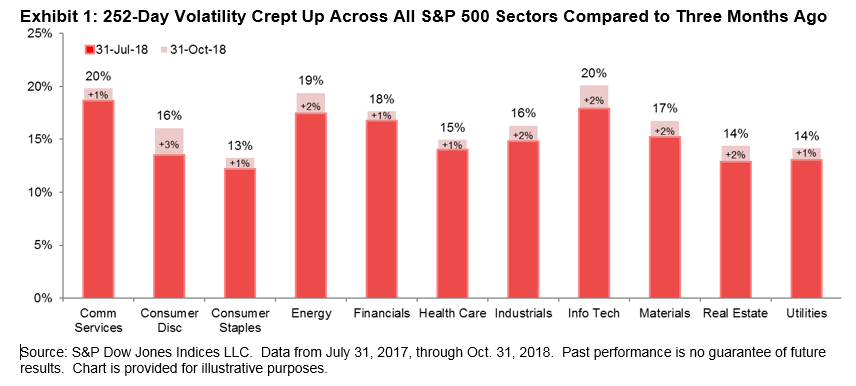

Volatility rose across all sectors of the S&P 500 (see Exhibit 1) and this gives us partial insight into the latest rebalance (reflecting data as of Oct. 31, 2018 and effective after market close Nov. 16, 2018) for the S&P 500 Low Volatility Index.

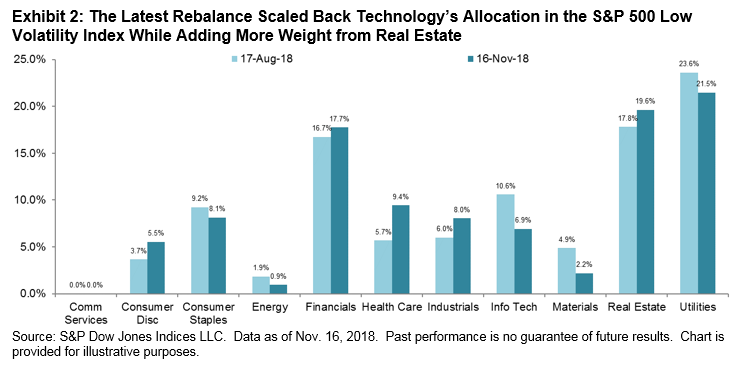

Exhibit 2 shows the sector allocations for the low volatility index after the most recent rebalance compared to three months prior. As a side note, the GICS reshuffle at the end of September 2018 resulted in a newly named Communication Services sector (combining the old Telecommunication Services sector with some companies shifted from Consumer Discretionary and Technology). However, as it relates to the S&P 500 Low Volatility Index, this change was mostly cosmetic. The index held no Telecom companies three months ago and this rebalance also yielded no stocks from the Communication Services.

Outside of the GICS restructure, the most significant changes were in Health Care and Technology, an addition and a reduction of 4%, respectively. A few names dropped from the Technology sector but the sector’s current standing within the index is still fairly significant from a historical context. Real Estate continued to gain ground, now almost on par with Utilities’ weight in the index. It is the second consecutive rebalance where Utilities scaled back; the sector now has a 21% allocation. Consumer Discretionary’s addition of 2% was somewhat counterintuitive, as the sector was among those that rose the most in volatility, pointing to specific stocks with lower relative volatility in this sector.

The posts on this blog are opinions, not advice. Please read our Disclaimers.