On May 16, 2014, the Lok Sabha election results were announced and Mr. Narendra Modi’s Bharatiya Janata Party got a clear mandate to form the government. Narendra Modi was sworn in as the Prime Minister of India on May 26, 2014. Since taking charge, the Narendra Modi government has made several landmark policy decisions. Some of these initiatives are listed below.

- GST: The Goods and Services Tax is the biggest tax reform since Indian independence.

- Aadhaar Linking: Linking Aadhaar to bank accounts, PAN Card, mobile number, etc.

- Jan-Dhan Yojana: Aimed at bringing banking services to every household in India.

- EPFO Investment in ETFs: Employees’ Provident Fund permitted to invest in ETFs.

- Demonetization: Aimed at cracking down on black money.

- Digital India: Aimed at digitizing India and moving to cashless transactions.

- Make in India: Aimed at making India a global manufacturing hub.

- Skill India: Aimed at providing skill development training to youth.

- Startup India: Aimed at promoting entrepreneurship.

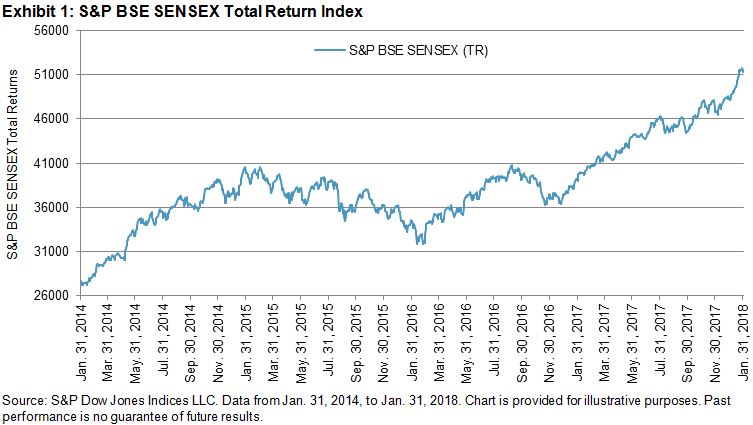

The S&P BSE SENSEX is the oldest and most-tracked index in India, and it acts as an indicator of India’s economic growth. Any national or international change in economic activity is likely to have an impact on the S&P BSE SENSEX.

The S&P BSE SENSEX’s total return index value increased from 27,648.13 on Jan. 31, 2014, to 51,281.74 on Jan. 31, 2018, and the highest close was at 51,729.13 on Jan. 29, 2018. This represents a four-year CAGR of 16.70% for the period.

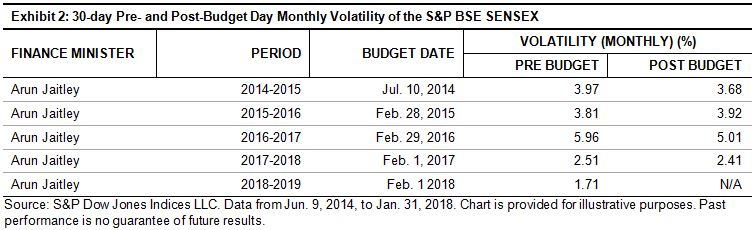

Every year, the Finance Minister presents the Union Budget, which is perhaps the most important economic activity in India. “Budget Day” comes with a lot of expectations, and it therefore has a bearing on the capital markets in both the pre- and post-budget sessions. Mr. Arun Jaitley has been the Finance Minister since this Government was formed. Arun Jaitley has presented four budgets during this term and will be presenting his fifth budget on Feb. 1, 2018.

In Exhibit 2, we can see that in most years, the S&P BSE SENSEX witnessed high volatility in the 30-day pre- and post-budget sessions. The highest 30-day pre- and post-budget volatility was observed in the budget year 2016. The lowest volatility in the 30-day pre-budget session was seen in 2018.

To conclude, we can say that the budget sessions are usually volatile for capital markets in India. The pre-budget movement is caused by market participant expectations for the budget, while the post-budget movement is based on the actual budget presented by the Finance Minister. The budget may be the most important economic activity affecting capital markets in India, and its relevance is captured in the movement of S&P BSE SENSEX.

The posts on this blog are opinions, not advice. Please read our Disclaimers.