Over the last decade, beta commodity exposure has offered investors inefficient access to the commodity market, mostly due to front-month roll methodologies and fixed commodity weights. The Dow Jones RAFI Commodity Index is a broad commodity index based on Research Affiliates’ commodity strategy that utilizes price momentum and roll yield to provide (1) dynamic commodity weighting exposure and (2) intelligent futures contract selection.

The Dow Jones Commodity Index, as one of the oldest and most recognizable broad commodity indices, provides diversified broad commodity exposure to 24 commodities. Research Affiliates utilizes the Dow Jones Commodity Index as the starting point to build the Dow Jones RAFI Commodity Index, which is intelligently built to offer equal weight exposure to the energy, metals and agricultural sectors in order to maximize diversification.

The Dow Jones RAFI Commodity Index utilizes a dynamic roll process that considers both roll yield and contract liquidity in selecting which commodity contract to own. In addition, the strategy reevaluates contract selection on a monthly basis to ensure the optimal contract is owned.

Understanding How Roll Yield and Momentum Affect the Dow Jones RAFI Commodity Index

The Dow Jones RAFI Commodity Index utilizes two key factors in constructing its commodity strategy: High Roll Yield and High Momentum.

Roll Yield takes into consideration the shape of a commodity’s futures curve. The shape of the curve can serve as an important indicator of a commodity’s inventory levels. Low inventories can potentially create positive roll yield scenarios, where an investor can theoretically purchase a contract further out on the curve at a lower price than what they could purchase at a nearer-term contract. The strategy is designed to increase its exposure to commodities with a positive roll yield. Conversely, high inventories can potentially create negative roll yield, where an investor purchases a contract further out on the curve at a higher price than what they could purchase at a nearer-term contract. The strategy is designed to decrease its exposure to commodities with a negative roll yield.

Momentum takes into consideration the price movement of commodities. Imbalances in supply or demand can create positive or negative price momentum which may persist over time. A decrease in supply created by a crop drought, for example, can drive prices higher. Conversely, a new discovery of oil can drive prices lower. The strategy is designed to increase its exposure to commodities with high price momentum.

Why Fundamental Commodities?

- Strong hedge against Inflation

- Broad, dynamic commodity exposure

- Low cost, transparent institutional solution

- Protection against negative roll yields

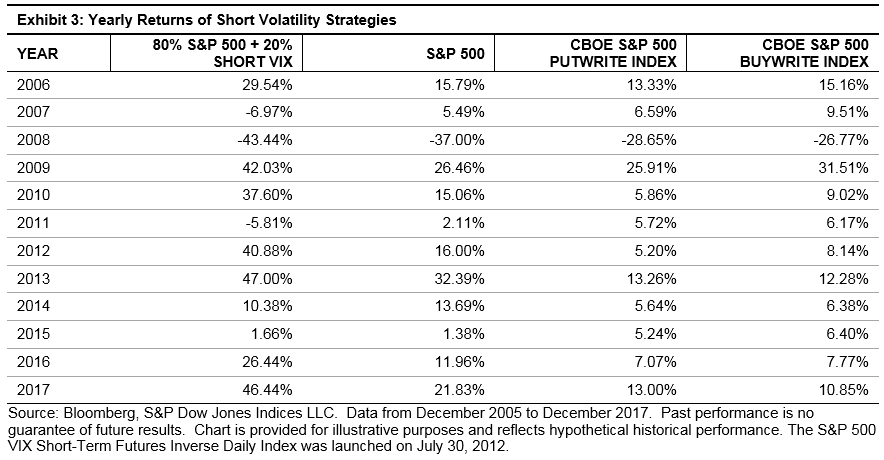

A Top Performing Broad Commodity Strategy

In 2017, The Dow Jones RAFI Commodity Index finished as the top performing* popular broad based commodity index. In addition, the Index provided superior return/risk statistics relative to both the Bloomberg Commodity Index and the S&P GSCI Index. While past performance is no guarantee of future results, the strategy of the Dow Jones RAFI Commodity Index has thus far proven to be one of the most intelligent strategic beta strategies in the broad commodity space.

*Source: Bloomberg L.P. as of 12/29/2017. All data based on total return figures.

The posts on this blog are opinions, not advice. Please read our Disclaimers.