The decision to claim social security benefits is not as straightforward as it seems and involves a number of key considerations. Given that it is a one-time decision and locks in one’s benefits permanently, aside from periodic cost of living adjustments, it is important for retirees to rethink whether there is an optimal timing and strategy for claiming Social Security benefits.

As a source of retirement income, the rules for claiming Social Security benefits are fairly straightforward. The rules are designed such that they are actuarially equivalent, no matter when one chooses to receive the benefits. Once one has earned enough credits to qualify for benefits, retired-worker benefits can be claimed as early as 62 or as late as 70. Collecting Social Security benefits early will permanently reduce one’s monthly income amount, while choosing to delay benefits has the effect of a permanent increase. Exhibit 1 shows the reductions and increases at different ages when filing for Social Security benefits for someone whose full retirement age is 66.

Collecting Social Security benefits early results in a benefit reduction of 6.67% per year for up to 36 months before full retirement age, and a rate of 5% per year beyond that. Conversely, choosing to delay benefits after full retirement age has the effect of an 8% increase per year, and this delayed retirement credit can accumulate until age 70. Beyond age 70, no more credits are granted.

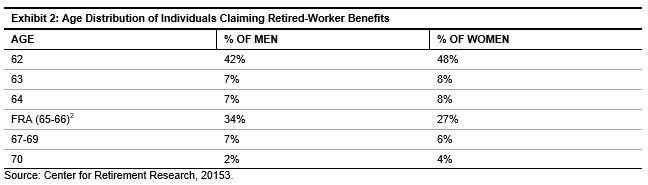

The Social Security Administration does not advocate any particular age on the timing of the claiming of the benefits. However, it does publish the benefit claiming data in its Annual Statistical Supplements report. The Center for Retirement Research at Boston College analyzed the data for the 2013 claim year.[1] The results are presented in Exhibit 2.

Despite the fact that the benefit amounts would be significantly higher when delayed beyond the full retirement age, 90% of retirees begin collecting Social Security benefits at or before their full retirement age. It is fair to say that most retirees choose not to maximize their Social Security benefits.

While there is no one-size-fits-all single timing strategy, retirees who are considering claiming Social Security benefits should consider the following key factors to weigh any tradeoffs. The relevant factors to consider are:

- level of the benefits,

- longevity or mortality assessment,

- current financial needs, and

- marital status.

[1] Source: “Trends in Social Security Claiming” by Alicia H. Munnell and Anqi Chen, Center for Retirement Research at Boston College, May 2015, Number 15-8)

[2] The Full Retirement Age (FRA) increased by two months for workers who turned 65 in 2003 and continued to rise at this pace each year until reaching 66. As a result of the shift in the FRA, Table 6.B5 in the Annual Statistical Supplement 2014, Social Security Administration, reports distributions from age 65 to the FRA and at the FRA. Exhibit 2 combines these two claiming groups into one group: FRA (65-66).

The posts on this blog are opinions, not advice. Please read our Disclaimers.