- The energy fundamentals, helped by Hurricane Harvey, are now in place for solid rebalancing and for potentially continued strong performance.

- Metals have reflected bullish sentiment but have recently been hindered by Chinese growth and credit concerns.

- Agriculture has been well oversupplied on better than expected weather and from improving farming technologies.

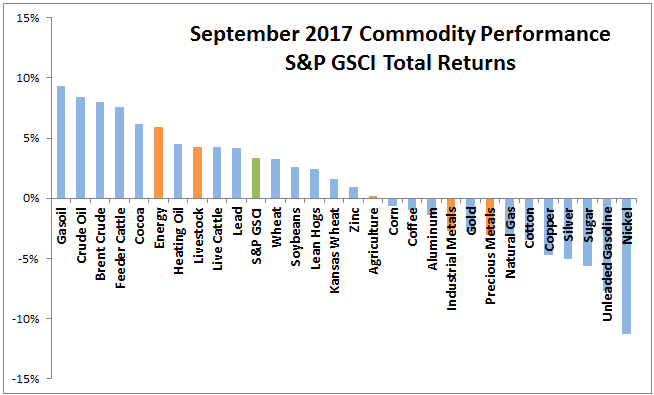

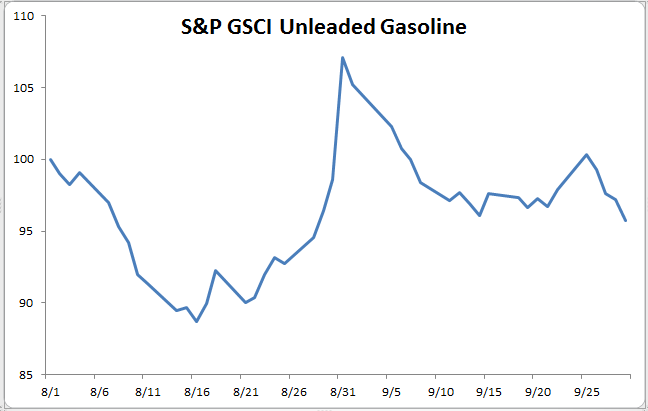

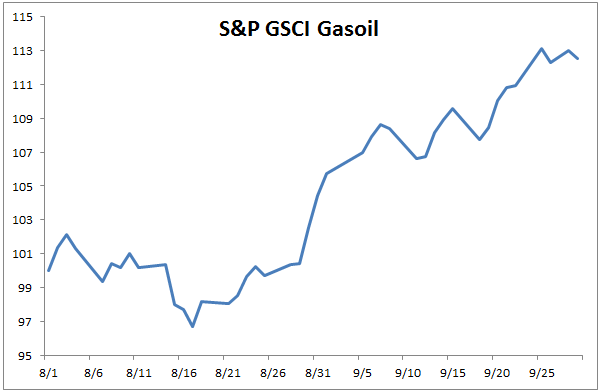

In September, three of five sectors were positive and thirteen of twenty four commodities were positive in the S&P GSCI Total Return that had an overall return of 3.3% in the month, 7.2% for the third quarter and -3.8% year-to-date. Energy was the best performing sector for the month, returning 5.9%, while the precious metals sector lost the most, down 3.0% in September. Gasoil was the winning single commodity for the month with a gain of 9.3%, and nickel lost 11.3% in the month, making it the most losing single commodity.

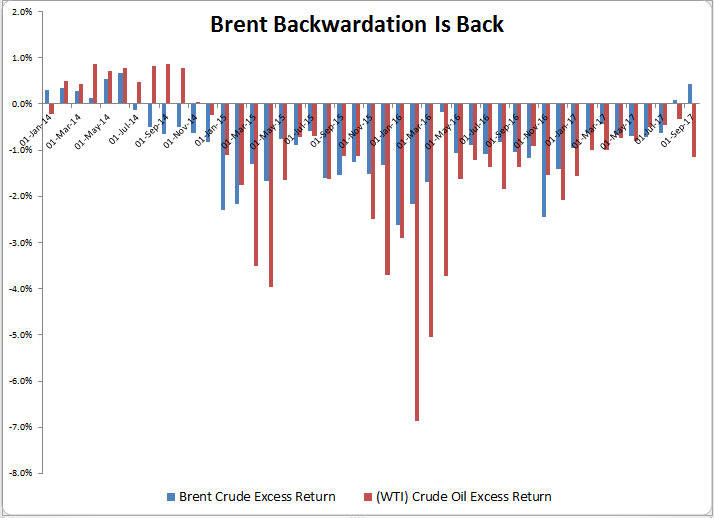

During the month, oil entered a bull market since the June 21, 2017 bottom with Brent Crude up 26.1% and (WTI) Crude Oil up 21.5% from better OPEC compliance, hurricane Harvey, and strong demand growth. Brent backwardation is the most since June 2014, and WTI crude oil contango was smallest since Dec 2014, before the storm but refinery disruptions and demand slowdown boosted the contango again to the highest since Jan 2017.

The after-effects of hurricanes generally have an impact on the commodities market. Hurricane Harvey caused gas prices to rise because the infrastructure needed to transport the gas to the refineries in Texas was badly damaged, but the price has come down as refineries come back online.

On the other hand, gasoil has continued to rise from not just the supply disruption, but also from the increased demand of fuel for machinery in construction for the rebuilding in the aftermath of the hurricanes.

Overall, the disruption to the energy supply led energy to have its best month yet in 2017, and again could be a solid foundation for the market to rebalance. On the flip side precious metals lost 3.0% in September, led by gold down 2.8%, posting the worst month (for both precious metals sector and gold single) not just this year but since Nov, 2016. This is from a rising dollar and expectations of a rate hike. This split shows the fundamentals are overtaking the aggregate demand in driving commodities today.

For more on quarterly performance, please see this article and this one too.

The posts on this blog are opinions, not advice. Please read our Disclaimers.