As a follow up to the previous article, Bond Connect officially launched on July 3, 2017. Bond Connect allows international market participants to trade China’s interbank bonds through the Hong Kong Stock Exchange. It marked a milestone in China to further open up its capital market, following the China Interbank Bond Market (CIBM) announcement last year. Let’s take a closer look at the recent developments of China onshore bond market.

Similar to other existing channels, like RQFII and CIBM, Bond Connect allows market participants to access China’s onshore bond market, yet through the trade custody and settlement infrastructure connect features, Bond Connect is more cost and time effective for some market participants. As expressed by Bond Connect Company Ltd*, it significantly reduces the account opening time to three working days and improves the price discovery with electronic trading.

According to Mr. Pan*, Deputy Governor from People’s Bank of China, a total of 479 financial institutions invested in the China bond market with over RMB 800 billion under several schemes. The participation of overseas market participants is still low, around 3.9% in government bonds and 1.2% in overall bond markets. It is unparalleled to the size of the China bond market, which was RMB 53 trillion as tracked by the S&P China Bond Index, hence there is further room for internationalization.

In terms of market performance, the total return of the S&P China Bond Index fell -0.49% year-to-date (YTD), while its yield-to-maturity tightened 23 bps to 4.31% during the same period, data as of July 3, 2017. The index currently tracks the performance of 9,650 government and corporate bonds from China. The S&P China Government Bond Index represents over 66% of the overall exposure, with a market value of RMB 35 trillion.

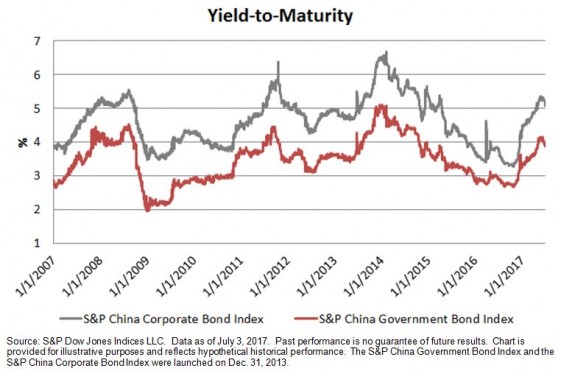

The S&P China Corporate Bond Index has expanded rapidly in the past 10 years, as the market value tracked by the index was RMB 18 trillion, which has increased 34-fold since the index’s first value date on Dec. 29, 2006, and the yield-to-maturity stood at 5.04% with a modified duration of 2.44 (see Exhibit 2 for the yield comparison).

On the back of the growth story, attractive yields, and diversification, the allocations in China’s onshore bonds are poised to rise in the coming years, particularly with the new accesses through Bond Connect and CIBM.

Exhibit 1: Market Value of the S&P China Corporate Bond Index and S&P China Government Bond Index

Exhibit 2: Yield-to-Maturity of the S&P China Corporate Bond Index and S&P China Government Bond Index

*Source: Bond Connect Investor Forum on July 3, 2017.

The posts on this blog are opinions, not advice. Please read our Disclaimers.