Chinese authorities will allow market participants to buy onshore bonds through transactions carried out in Hong Kong, which will further broaden foreign access to China’s onshore bond market. While no additional details have been provided, a “bond connect” scheme that provides cross-border cash bond trading is anticipated by market participants.

Despite currency volatilities, China bonds offer better yields and diversification benefits. However, foreign investors are concerned with the potential credit risk. Besides the non-parallel rating systems between local and the international standards, the implicit government guarantees prevented bond defaults, which had made it difficult to analyze the true underlying credit risk.

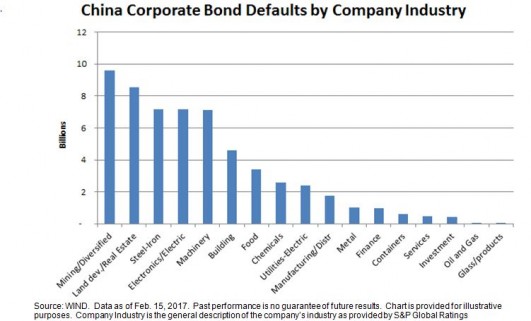

However, following the first bond default in 2014, the number of bond defaults has been accelerating, including those of state-owned enterprises. According to WIND data, over 60 bonds defaulted in 2016, with the affected sectors including land development, mining, steel-iron, and oil & gas. The biggest default in 2016 was from China City Construction, a Chinese construction and development firm, with a collective defaulted amount of CNY 8.55 billion. In the first two months of 2017, bond defaults amounted to CNY 4.1 billion from Dongbei Special Steel, Dalian Machine Tool, and Inner Mongolia Berun.

From 2014 to February 2017, China recorded a total of CNY 58 billion of bond defaults, which is equivalent to 0.11% of the current overall market value, as tracked by the S&P China Bond Index. The top two industries that had the highest default amounts were mining/diversified and landing development/real estate, reflecting the sharp slowdown in Chinese manufacturing and construction.

The defaults are perceived to be healthy for the long-term development of China’s onshore bond market. In the search for higher-quality corporate bonds, we adopted a two-tier screening approach in our index design and launched the S&P China High Quality Corporate Bond 3-7 Year Index. As per the index methodology, issuers must first be investment-grade rated by at least one of the international rating agencies, and then securities must be rated ‘AAA’ by at least one of the local Chinese rating agencies.

Exhibit 1: China Corporate Bond Defaults by Company Industry (Total Par Amount)

The posts on this blog are opinions, not advice. Please read our Disclaimers.