With anemic global economic growth, investors have become leery about U.S. companies’ ability to grow earnings and increase dividends.

Indeed, S&P 500 earnings declined for the fifth consecutive period in the second quarter of 2016 and even if the third quarter results are positive, the growth rate is likely to be very small. A potential consequence of this “earnings recession” is that future dividends could be at risk. Earnings are an essential driver of dividends, and ultimately returns, so there is good reason for concern.

But there’s an exclusive group of companies that may provide an answer. The S&P 500 Dividend Aristocrats® Index includes high quality companies that have increased their dividends every year for at least 25 consecutive years. How are these companies able to continually grow dividends? One answer is by delivering earnings growth. The S&P 500 Dividend Aristocrats have delivered positive annual earnings growth for the first two quarters of 2016 in amounts that were substantially higher than the broad market.

Source: Morningstar, ProShares, May 2, 2005–June 30, 2016. Index performance is for illustrative purposes only and does not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest in an index. Past performance does not guarantee future results.

The Take Away

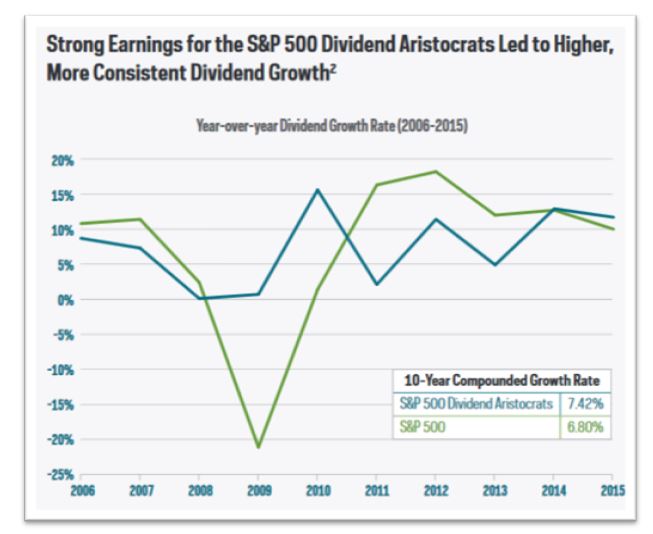

Historically, the Dividend Aristocrats have grown their dividends on a more consistent basis and at a higher compound rate than the broad market, underscoring their quality and potential for strong performance. Since inception of the index, the Aristocrats have delivered higher returns with lower volatility than the S&P 500.