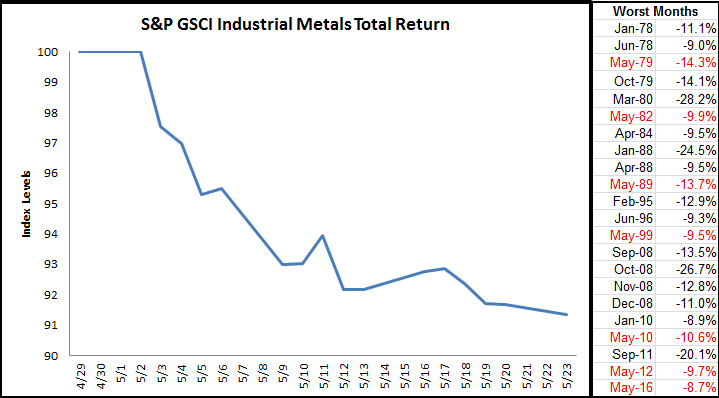

Commodities are starting summer hot and early. Ending May, the Dow Jones Commodity Index (DJCI) was flat, but the S&P GSCI gained a total return of 2.2%, making it the third consecutive positive month for the index. This is the first time commodities have gained three months in a row since the period ending in Apr. 2014, and this is the biggest three month gain, 18.1%, for commodities since the period ending in July 2009 when they returned 20.9%.

Although the industrial metals sector lost 7.1%, posting its worst month in a year, and the precious metals sector lost 6.3% in its first negative month of 2016, the energy sector, currently comprising near 70% of the index, gained 4.6% in May, for a three month return of 30.4%. It’s the biggest three month gain for energy since the period ending in Jun. 2008 when it gained 37.5%. Also, livestock and agriculture gained 3.2% and 1.3%, respectively in May. However, what is interesting is the roll return (measuring backwardation in the sector) turned positive in agriculture for the first time since May 2015 and has improved in energy from -5.6% in Feb. to just -1.5% in May. There has not been an increase in roll yield this quickly in energy in seven years, since May 2009.

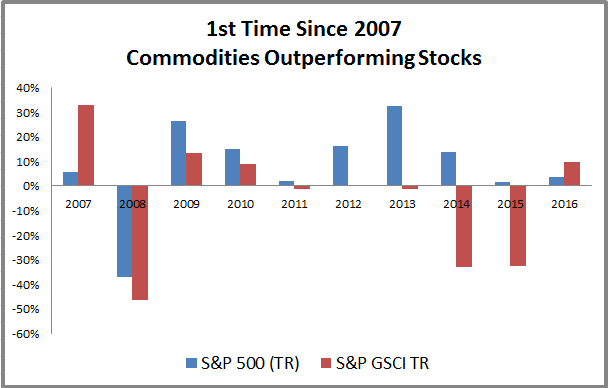

Year-to-date, the total return of the S&P GSCI is positive 9.8%, and has gained 26.2% off its bottom in Feb. Commodities are now outperforming stocks for the first year since 2007.

If this outperformance holds through the year’s end, it will break the longest number of consecutive years that stocks outperformed commodities. Following the last time equities outperformed commodities for near as long in 1980-86, seven consecutive years, commodities returned almost 300% through 1990 when the trend reversed. (The bottom index level of the S&P GSCI Total Return on April 16, 1986 was 716.51. The index returned 299.8% to reach a high level of 2864.40 on Oct 9, 1990.)

The posts on this blog are opinions, not advice. Please read our Disclaimers.