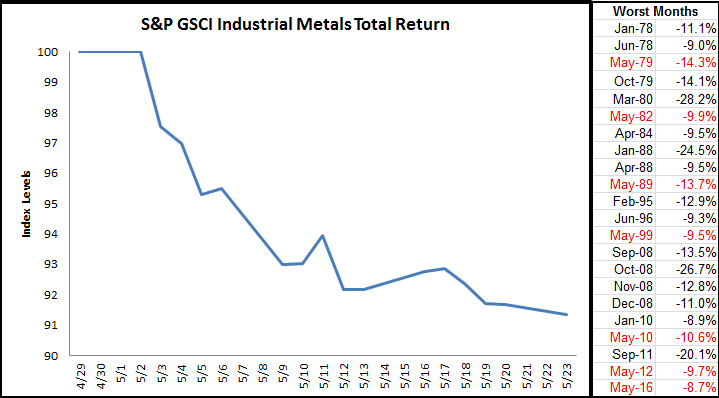

While most of the markets have calmed as investors wait for Brexit and the Fed rate decision, industrial metals are crashing. The S&P GSCI Industrial Metals Total Return is down 8.7% month-to date (through May 23, 2016,) and on pace to record its worst month since May 2012, when it lost 9.7%. At this rate, the sector is having not only its worst month in four years but its 7th worst May since 1978, when the index history started.

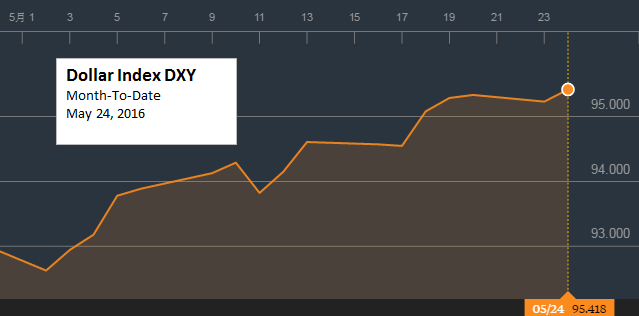

There has been little correlation of Chinese GDP growth to industrial metals, even copper, but two other factors may be causing the recent drop. The first is the rising dollar.

Industrial metals are some of the most sensitive commodities to the US dollar. In fact, of all 24 commodities, nickel tops the list of the single most susceptible to the rising dollar, dropping 1.9% for every 1% rise in the US dollar. Sure enough nickel is the biggest loser in the index so far in May, down 12%. The other industrial metals are pretty sensitive too. For every 1% rise in the US dollar over the past ten years, lead, aluminum, copper and zinc lost 1.3%, 1.1%, 1.0% and 0.4%, respectively. Month-to-date in May, lead, aluminum, copper and zinc lost 8.5%, 8.0%, 9.6% and 5.1%, respectively.

The other reason for the loss in the industrial metal sector is from rising inventories. It is difficult for producers to supply exactly the amount needed. After some mining closures and supply reductions, prices rose to cause suppliers to bring more of the metals to the market. This month inventories rose significantly for copper and lead that together comprise about half the weight in the sector.

As for the interest rate decision, all else equal, if rates rise, the dollar may strengthen so will likely hurt the sector but suppliers may adjust again to limit the price drops. On the other hand, if the dollar strengthens, its power to lift the industrial metals is far greater. In the past 10 years, for every 1% move down in the US dollar, gains in lead, nickel, copper, zinc and aluminum have been 7.2%, 6.1%, 5.3%, 4.6% and 2.2%, respectively. That’s a pretty strong upside potential to downside risk from the US dollar.

The posts on this blog are opinions, not advice. Please read our Disclaimers.