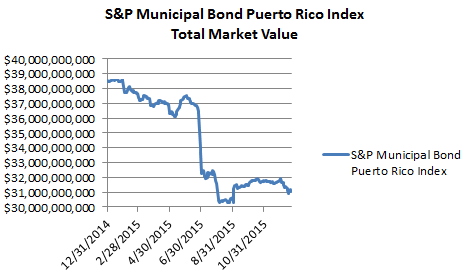

As the fiscal saga continues for Puerto Rico and it’s residents the impact has been crushing for the bond holders in 2015. The total market value of bonds tracked in the S&P Municipal Bond Puerto Rico Index has fallen by over $7.5billion.

Chart 1: Total Market Value of Bonds in the S&P Municipal Bond Puerto Rico Index 2015

Source: S&P Dow Jones Indices, LLC. Data as of December 22, 2015.

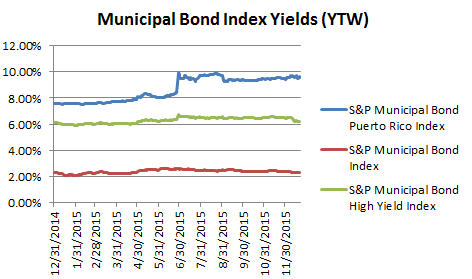

Yields for bonds in the S&P Municipal Bond Puerto Rico Index have ended at 9.62% which is 205 basis points cheaper than year end 2014. Prices of bonds in the index have been volatile to the down side for most of the year and yields reached their cheapest point on June 29th when they got as high as 9.9%.

Chart 2: Select Municipal Bond Index Yields (Yield to Worst)

Source: S&P Dow Jones Indices, LLC. Data as of December 22, 2015.

Some aspects about the index that impact this result:

- Defaulted bonds remain in this index

- Bonds that have matured that were not in default are removed from the index

- News issues are added based on inclusion criteria