The ‘belly’ of the municipal bond curve or the 5 – 10 year maturity range has done well this year, almost as well as the longer maturity range. Returns for non-callable investment grade municipal bonds tracked in the 5, 7 and 9 year range all have demonstrated good returns in this low rate environment.

The S&P AMT-Free Municipal Series 2024 Index shows non-callable municipal bonds maturing in 2024 have an average yield of 2.16% and have returned 3.5% year-to-date. This range has outperformed the composite S&P National AMT-Free Municipal Bond Index and has nearly kept pace with longer bonds tracked in the S&P Municipal Bond 20+ Year Index.

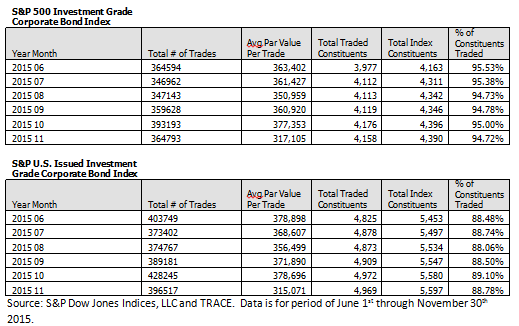

Table 1: Select Municipal Bond Indices Yields and Returns: