This Wednesday, the Fed announced that they would begin raising rates, a decision that has left many investors with questions about how they will fare in this changing environment. Knowing that conventional, fixed-rate securities sometimes lose value when interest rates increase has some investors looking to floating-rate securities instead. Floating-rate securities are designed to mitigate interest rate risk by regularly adjusting to keep pace with the movements of short-term rates. In short, that means floating-rate securities should exhibit minimal price sensitivity to changes in interest rate levels. To see how floating-rate securities have performed in anticipation of this announcement, we will take a look at examples in the preferred stock and senior loan markets over the last year.

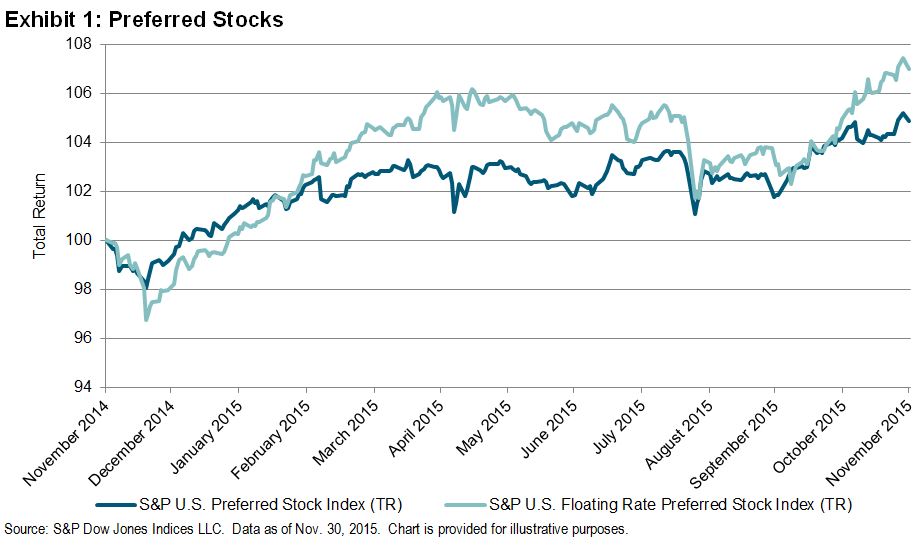

Preferred stock is a class of capital stock that generally pays dividends determined by a fixed rate, variable rate, or a floating rate. The S&P U.S. Preferred Stock Index comprises preferred shares of each dividend payment type. When comparing the S&P U.S. Preferred Stock Index to the S&P U.S. Floating Rate Preferred Stock Index, we can observe that while both have positive returns, floating-rate stocks have outperformed stocks that are more interest rate sensitive by 2.71% in the past one-year period (see Exhibit 1).

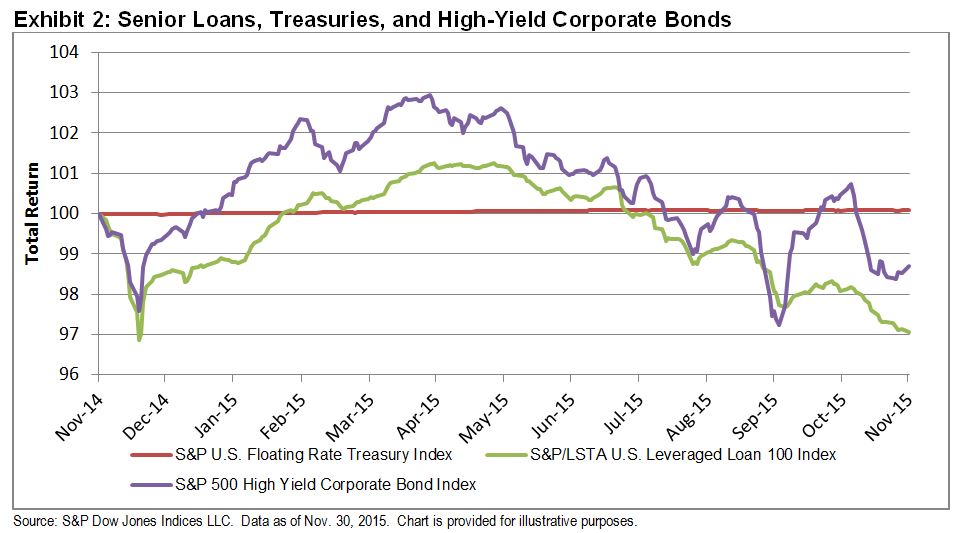

The preferred stock example helps us understand why there is an expectation for floating-rate securities to perform well given this environment. However, the senior loan market’s underperformance this year has shown that floating rates act as protection from only one of many confluent pressures. Senior loans have felt the detrimental effects of supply outpacing demand most months this year. New issuances have expanded the overall size of the market, while retail investors continue to be net sellers of loans on the year. According to S&P Capital IQ LCD, institutional and retail allocations alike have stalled in response to volatility in the broader markets and are likely refraining from shifting capital back in until it is clear the Fed intends to consistently raise rates through 2016. Consequently, the S&P/LSTA Leveraged Loan 100 Index has taken a -1.55% hit YTD, demonstrating that floating-rate securities can actually sink in a rising rate environment and even underperform fixed-rate securities.