Roger McNamee, the American businessman and sometime musician said “We need to stop thinking about infrastructure as an economic stimulant… [since] economic stimulants produce Bridges to Nowhere. Strategic investment in infrastructure produces a foundation for long-term growth.” In 2013, Transportation for America identified that one in nine U.S. bridges—a jaw-dropping 66,000 of them—are deficient, and they are a striking example of the USD 1 trillion per year global infrastructure spending gap identified by the World Economic Forum last year.

If—as McNamee trumpets—infrastructure investment promotes growth, owners of large pools of capital should, by design, be interested. Global pension assets are one such reservoir, totaling around USD 40 trillion and predicted to increase to USD 65 trillion1 by 2020, yet less than 1% of aggregate pension assets are invested in infrastructure, and those funds that are sold on the investment benefits are finding a persistent gap between actual investment (2.9%) and their target allocations (3%-5%).2 The asset class is attractive to institutional investors looking for growth and inflation hedging, with investment return expectations for “Core” and “Core Plus”—investments in societal staples such as bridges, rail, roads, and airports—near 7%-13% per year.3

So why is the channel between spending requirements and return seekers seemingly unbridged? Three possibilities exist. First, the availability of suitable investment opportunities seems limited, as characterized by unallocated investment capital, which is at a record level of USD 100 billion.4 Second, the median pension fund infrastructure investor size is USD 6 billion,5 pointing to expertise and governance requirements many funds consider beyond their scope. Third, in a pensions management world where there is persistent and relentless focus on cost, specialized infrastructure manager fees of 2% and 10% of excess return over 8%6 are out of kilter. Infrastructure returns—in this context—seeming to have high barriers to entry.

But do they? A growing globally listed equity market now capitalized at approximately USD 3.5 trillion, with daily average trading volumes of USD 15 billion,7 affords funds the liquidity many desire, as well as a “governance advantage” due to the stringent regulatory demands and reporting requirements of listing. So far so good then—but what do the returns look like when holding liquid investments for the long term?

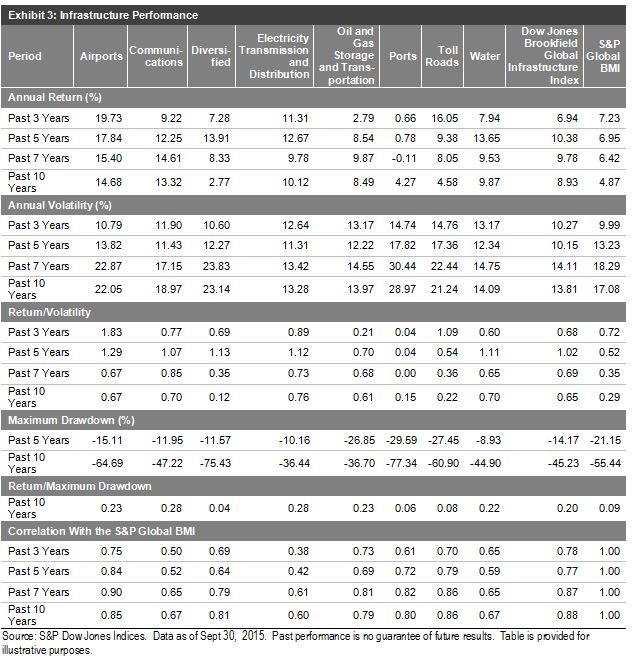

Two interesting outcomes can be observed. First, 10-year annualized returns—as represented by the Dow Jones Brookfield Global Infrastructure Index—compare favorably to the top end of the “Core Plus” range of return expectations (10%-13%).

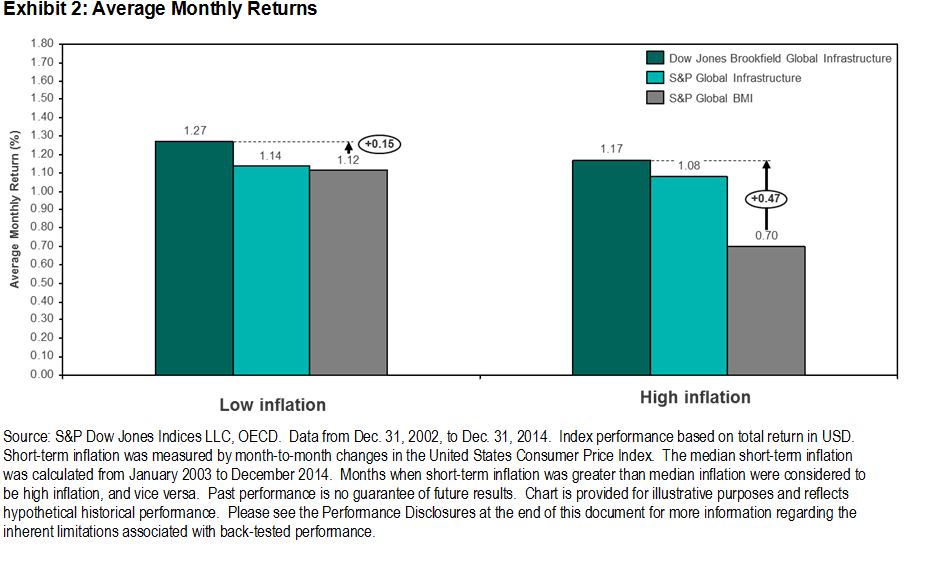

Second, discernible inflation-hedging characteristics—one of the most desirable characteristics of infrastructure investing5—are present for historical infrastructure equity buy and hold approaches, with a 47 bps monthly excess return in high inflation scenarios seen over broad equity from 2004-2014.

Of course, equity exposure comes with equity risk, although the average 10-year annualized volatility of 13.8% for infrastructure equity versus 17% for global broad equity, along with the notably reduced maximum drawdowns for infrastructure, is observed.

In recent times, such notable names as AP4 and NZ Super have invested in infrastructure through listed securities.8 With exposure to desirable characteristics of return and inflation protection also possible in the cost efficient, indexed manner so many pension funds now embrace, listed markets could bridge the perceived governance and expertise gap bringing the asset class in closer reach to even the smallest funds without the (toll) fees that have historically been the norm.