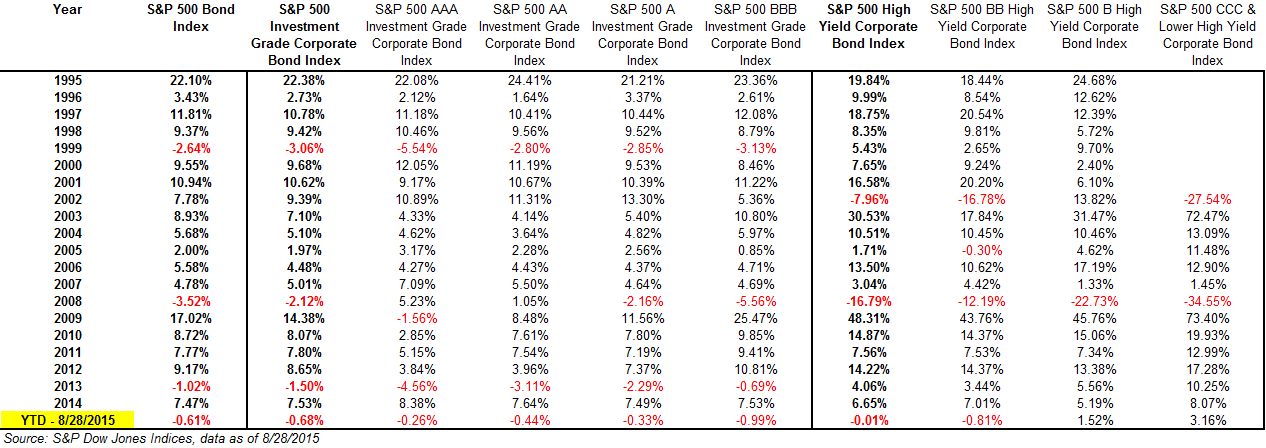

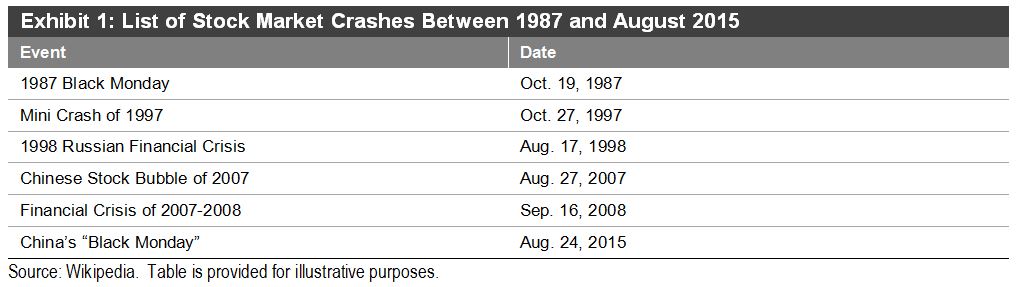

On Monday, Aug. 24, 2015, the global stock market tumbled, with the Dow Jones Industrial Average® losing 1,000 points in seconds. We have seen similar turbulence in the equity markets in 1987, 1997, 1998, 2007, and 2008.

We know that the stock market is an important leading indicator, as it reports on the health of companies’ earnings estimates and the health of the global economy. Housing prices can also be considered leading indicators, as a decline in housing prices can be representative of excess supply and inflated prices.

The S&P/Case-Shiller Home Price Indices use the repeat sales methodology, which has the benefit of directly measuring changes in home prices by only including homes that have been sold twice. The indices are calculated monthly, using a three-month moving average. Index levels are published with a two-month lag.

I want to use this post to see if the sharp declines in equity prices (using the S&P 500® ) are reflected in the S&P/Case-Shiller Home Price Indices, and, if so, in what time frame and at what magnitude? The dates evaluated are depicted in Exhibit 1.

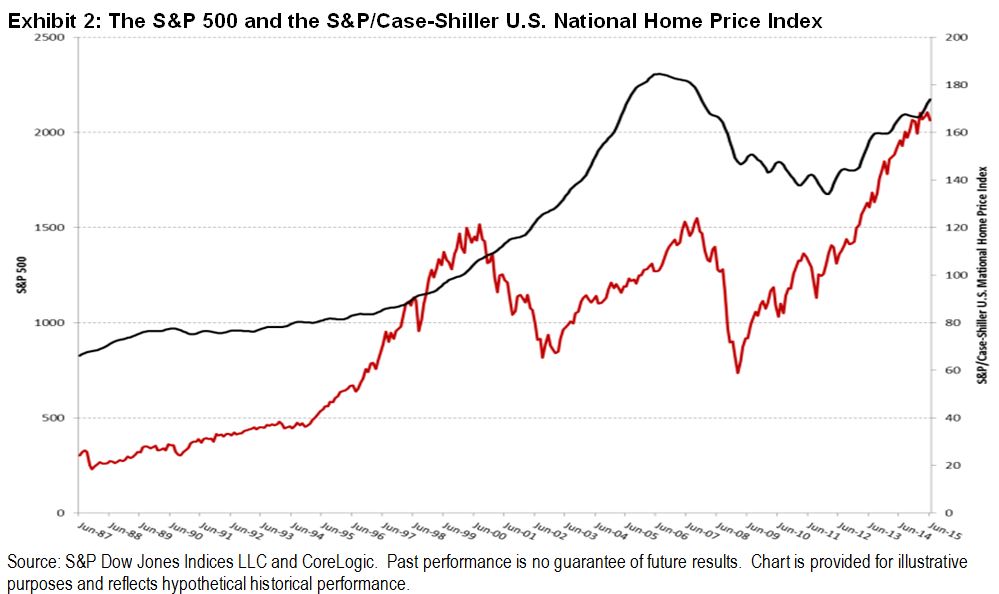

Exhibit 2 charts the levels of the S&P 500 against the levels of the S&P/Case-Shiller U.S. National Home Price Index.

While the indices moved in the same general direction, one clear difference was that the volatility in the equity market was not reflected in the housing market. The next step was to drill into the returns near the dates of the previous stock market crashes presented in Exhibit 1.

Prior to the stock market crash of 1987, the housing market had been exhibiting modest gains, and it did not turn into negative territory until August 1990, which was a period of recession in the U.S. Between that period and the crash of 1997, out of the 120 monthly return observations, the S&P/Case-Shiller U.S. National Home Price Index only reported 35 declines, and it proceeded to remain positive past the 1997 and 1998 crashes. The index went into negative territory in August 2006 (after a strong upward trend), one year before the August 2007 crash, and it stayed there through the September 2008 crash. It did not turn positive until 2010, and it continued to alternate between months of gains and months of losses until the present. By analyzing this data alone, it appears that the S&P/Case-Shiller Home Price Indices are more sensitive to mass economic crises and recessions than to turbulence in the equity market.

David Blitzer, Managing Director and Chairman of the Index Committee at S&P Dow Jones Indices, summed it up nicely saying, “Stock market correction is unlikely to do much damage to the housing market; a full-blown bear market dropping more than 20% would present some difficulties for housing and for other economic sectors.”

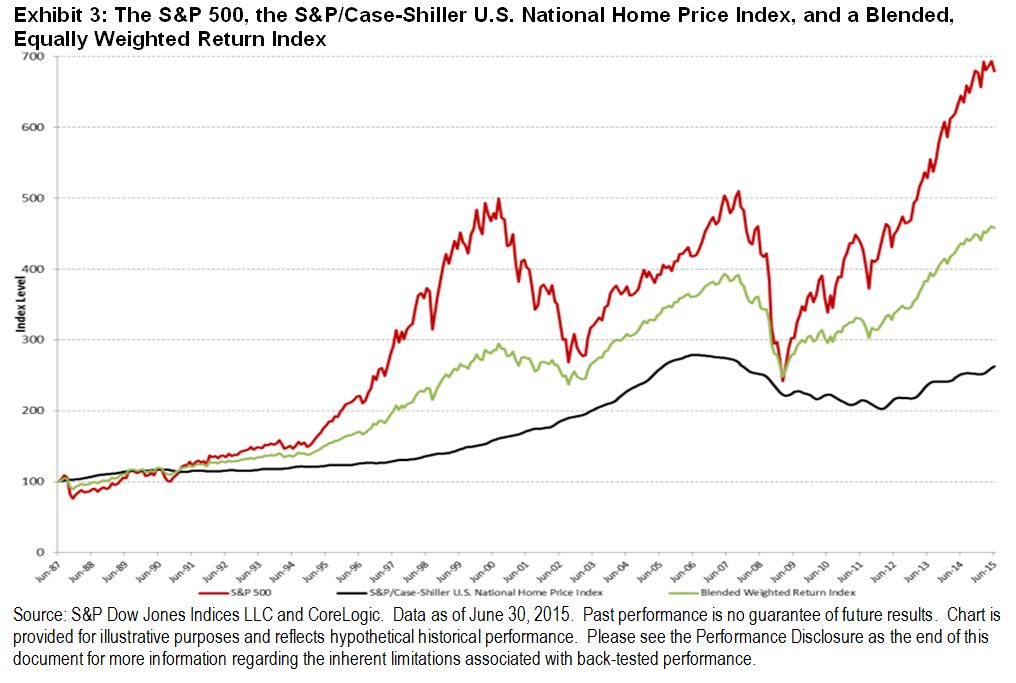

Just as food for thought, Exhibit 3 shows the levels of the S&P 500 and the S&P/Case-Shiller U.S. National Home Price Index against a blended, of the two indices (50% allocation in each index). The blended index enjoyed some benefits from the equity portion, gaining as much as 5.45% in December 1991, but it is less volatile than the equity index as is illustrated.[1]

[1] It should be noted that investors cannot invest directly in an index.

The posts on this blog are opinions, not advice. Please read our Disclaimers.