This week (starting July 27, 2015), the bond market has been off to a strong start, with the yield of the U.S. 10-year Treasury bond at 2.22%. U.S. bond prices have moved up as Chinese stock prices have plunged. Last week saw Treasury yields move lower, as dropping commodity prices followed the weaker CPI numbers that were released on July 17, 2015. Since June 30, 2015, the price of crude oil futures has dropped from 59.83 to its current level of 47.49. The yield-to-worst of the S&P/BGCantor Current 10 Year U.S. Treasury Index has moved lower by 9 bps throughout this week. As of July 27, 2015, the index has returned 1%, after starting off in the red. The index has returned 0.71% YTD, inching closer to the 1% return it had at the beginning of the month, but it was nowhere near January 2015’s 5.26% YTD return.

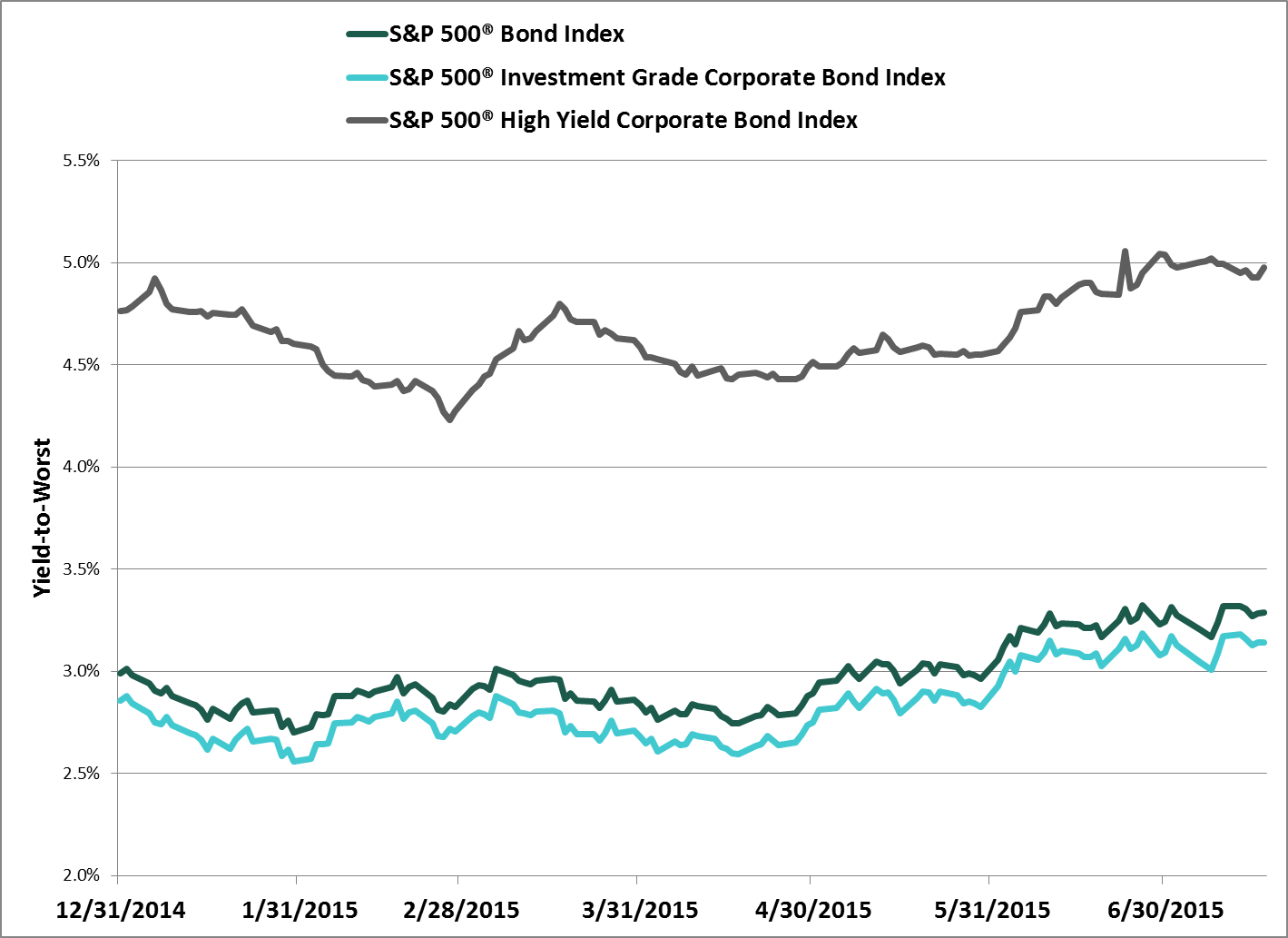

The S&P 500® Bond Index has seen its performance improve over the last week, as the month-to-date return, which had been negative since July 10, 2015, was able to recover and pushed out of negative territory on July 22, 2015, to reach 0.312%. The index was still negative YTD, at -0.323%, but it is not as low as the -1.125% that was posted on July 13, 2015. The broader, investment-grade index (S&P U.S. Investment Grade Corporate Bond Index) has returned 0.28% MTD and -0.18% YTD as of July 27, 2015.

High-yield bonds, as measured by the S&P U.S. Issued High Yield Corporate Bond Index, have seen their yield-to-worst widen by 24 bps just in the four days before July 27, 2015. The energy sector accounts for a 15% weight of the index and has underperformed by -5.94% MTD. The overall index has returned -0.97% MTD and 1.52% YTD.

The performance of the S&P/LSTA U.S. Leveraged Loan 100 Index has followed that of the high-yield index, but at a more conservative pace. The index has returned -0.18% MTD and 1.58% YTD. The crossover at which loans started outperforming high yield on a YTD basis occurred just last week, on July 23, 2015.

Source: S&P Dow Jones Indices LLC. Data as of July 24, 2015. Leverage loan data as of July 26, 2015. Past performance is no guarantee of future results. Chart is provided for illustrative purposes.

The posts on this blog are opinions, not advice. Please read our Disclaimers.