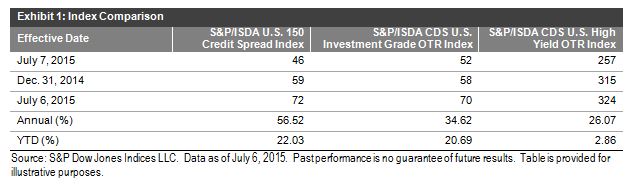

The S&P/ISDA U.S. 150 Credit Spread Index has seen spreads widen by 56.52% since July 2014. This means investors are demanding over 50% more on the notional cost of default insurance on the largest investment-grade corporate bonds tracked by the S&P 500®. CDS “insurers” from the S&P/ISDA CDS U.S. High Yield OTR Index saw spreads widen only 26.07% in the past 12 months, with the major discrepancy coming in 2015. The YTD change in spreads is roughly 10 times higher for investment-grade CDS spreads than high yield…however this only tells half the story.

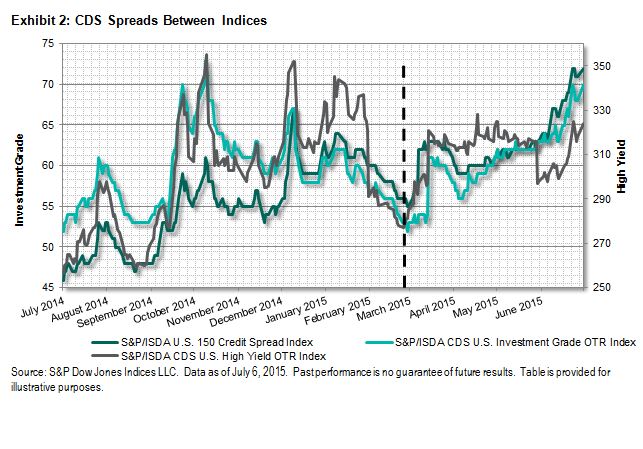

The cost of default insurance for the S&P/ISDA CDS U.S. High Yield OTR Index still costs more than 4.5 times as much as for the S&P/ISDA CDS U.S. Investment Grade OTR Index, as protection on a loan of USD 1 million would cost USD 32,400 and USD 7,200, respectively. The important takeaway is that tumbling investor sentiment is not reserved for the high-yield sector, and this may not bode well for the equity market. Examining the trend for each index since March 2015, spreads are moving only one way…up.

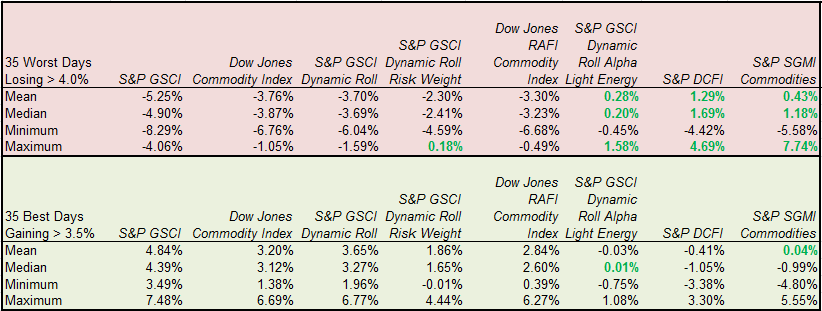

Source: S&P Dow Jones Indices. Ten years of daily data ending July 7, 2015.

Source: S&P Dow Jones Indices. Ten years of daily data ending July 7, 2015.