Continued lackluster U.S. economic activity right up until today’s slower personal consumption expenditures (PCE) report may have pushed rates lower during the last week of the month and into June’s start. The yield of the S&P U.S. Investment Grade Corporate Bond Index moved lower by 8 bps during the last week of the month to close at 2.89%. The May closing yield was still 6 bps higher than the April closing yield of2.83%. The index fell 0.47% for the month, and returned 1.10% YTD. With the move down in Treasury rates, corporate issuance continued at an active pace as new issue deals from Home Depot (USD 2.5 billion), PNC Bank (USD 3 billion), Time Warner (USD 2.1 billion), UBS (USD 3 billion), and many more were launched.

Vigorous issuance also occurred in the high-yield market, as ArcelorMittal (USD 1 billion), CommScope Tech (USD 2 billion), MarkWest Energy (USD 2.45 billion), and WellCare Health (USD 0.3 billion) all issued last week. The yield of the S&P U.S. High Yield Corporate Bond Index closed May lower by 6 bps, at 6.11%, compared with 6.16% at the start of the month. Year-to-date, the yield of the index is 73 bps tighter than the Dec. 31, 2014, yield of 6.84%. The index returned 0.51% for the month and returned 4.8% YTD. Outside of a slightly negative March (-0.19%), the high-yield index continues to provide positive monthly performance. The continued “kick the can down the road” approach to the Fed’s rate hike may have caused yield-craving investors to bide their time in the sector. High-yield bonds appear likely to return 5% in 2015, according to Martin Fridson, a veteran follower of the asset class and CIO of Lehmann Livian Fridson Advisors.[1]

In the shadow of the high-yield index’s YTD performance, the S&P/LSTA U.S. Leveraged Loan 100 Index returned 2.64% YTD. For May, the index returned 0.05%. Like the investment-grade and high-yield markets, issuance activity ramped up after the long Memorial Day weekend with 10 issuers tapping the market for a combined USD 8.72 billion.

After an increase of 11 bps in April 2015, the yield of the S&P/BGCantor Current 10 Year U.S. Treasury Bond Index continued its upward trend throughout most of May. The 10-year U.S. Treasury Bond regained support during the last week of the month as yield came back down to 2.13% after being as high as 2.29% during the month. Post month-end trading continues to move yields lower as the Fed’s preferred measure of inflation unexpectedly slowed in April (Core PCE year-over-year, 1.2% versus 1.3% prior). Overall for the month, the S&P/BGCantor Current 10 Year U.S. Treasury Bond Index closed 9 bps wider than its start of 2.04%. For the month, the return of the index was -0.62%, while YTD it returned 1.61%.

U.S. TIPS, as measured by the S&P U.S. TIPS Index, fell by 0.95% for May, as the YTD return closed out the month at 0.97%. Like nominal Treasuries, the TIPS index gained 0.27% the last week of May to help offset some of the prior three weeks of losses. The report of a slower PCE index makes it harder for the Fed to begin raising rates as inflation remains low.

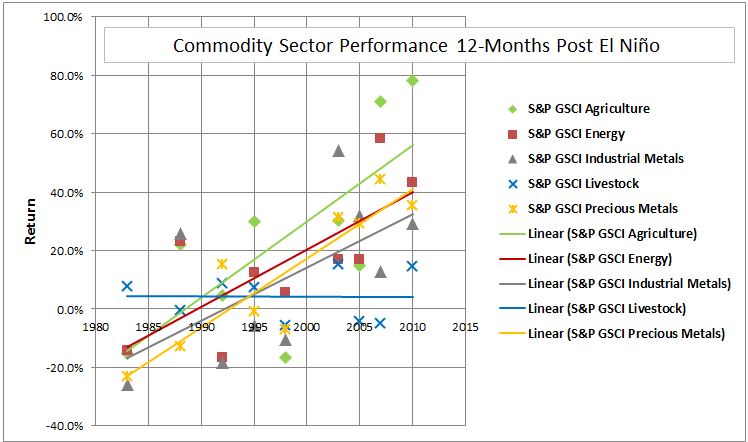

Source: S&P Dow Jones Indices LLC. Data as of May 29, 2015, leverage loan data as of May 31, 2015.

[1] The Street: High-Yield Bonds May Outperform Stocks in 2015 Despite Oil Price Fears, Jan. 16, 2015.

The posts on this blog are opinions, not advice. Please read our Disclaimers.