Broadly speaking, stocks within the same sector are often exposed to similar risk factors. Investors with large energy sector exposures have certainly been reminded of this over the last six months. This is precisely why segregating the U.S. equity universe by sector has been so appealing to investors over the years. Over the last 16 years, the average annual return differential between the best and worst performing sector has been nearly 40%.

At their core, factor-based equity portfolios are nothing more than groups of securities that share common characteristic(s). For example, the S&P 500 Pure Value Index includes members of the S&P 500 with the most attractive valuations as measured by earnings per share, book value to price value ratio and sales to price ratio.

Putting these two observations together – stocks within a factor portfolio and stocks within a sector sharing risk factors – it should be no surprise that pure factor portfolios can have sector concentrations that differ substantially from market-cap weighted benchmarks.

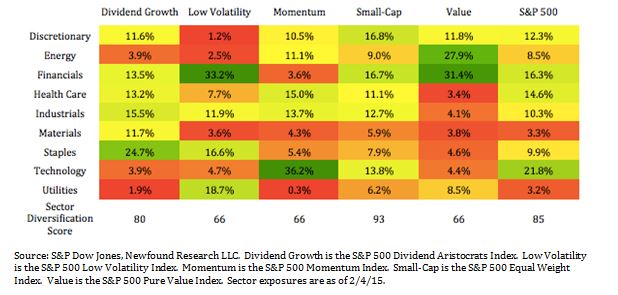

Within our U.S. Factor Defensive Equity strategy, we consider five factors: momentum, value, dividend growth, low volatility and small-cap. The table below presents the current sector weights for five S&P indices that represent these factors. Along with the sector exposures, we calculate a “Sector Diversification Score” for each of the factors as well as the overall S&P 500. A Sector Diversification Score of 0 would indicate 100% exposure to a single sector while a Sector Diversification Score of 100 would indicate equal exposure to each of the nine sectors.

Four of the five factor indices tilt significantly – greater than 10 percentage points – away from the individual sector weights of the S&P 500. This should not be worrying in the least bit. If a portfolio looks exactly like a market-cap benchmark, then we surely can’t expect it to do any better than a market-cap weighted benchmark in helping an investor achieve investment goals.

However, it does highlight the need to keep an eye on sector exposures as factor products are incorporated into investor portfolios.

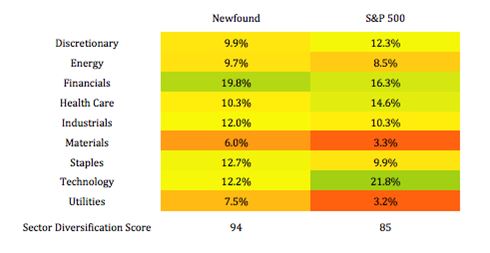

Our U.S. Factor Defensive Equity strategy holds all five of the factors discussed in inverse proportion to their volatility. The weights in our portfolio as of 1/31/15 are shown below.

| Dividend Growth | Low Volatility | Momentum | Small-Cap | Value |

| 22% | 24% | 19% | 19% | 16% |

By building a diversified factor portfolio we are able to increase sector diversification relative to the broad market.

One final point to keep in mind is that by definition factor-based portfolios and indices will rebalance more often than a market-cap weighted benchmark as the characteristics of the stocks in the overall universe change. Naturally, these rebalances mean that the sector allocations will change over time. The velocity of these changes will vary on a factor-by-factor basis. More frequent changes will be seen in factors that have a price component, including value and momentum.

The posts on this blog are opinions, not advice. Please read our Disclaimers.