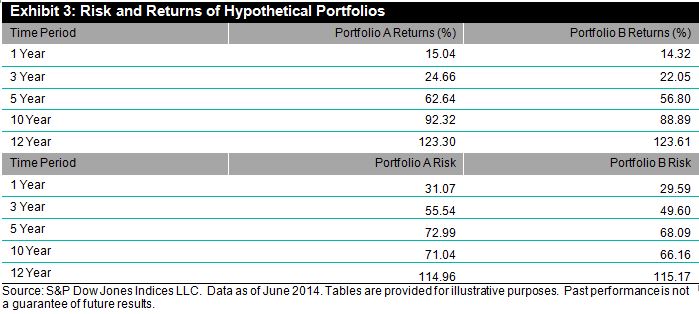

Like many in the northern hemisphere, the S&P 500® felt a bit blue in January. With the traditional winter frost came winds of volatility, which, like many of our holiday guests, overstayed their welcome. On a total return basis, the S&P 500 declined 3% in January, as market volatility from the fall of 2014 lingered into the new year.

All was not lost, however; certain factor-based strategies thrived in the volatility. The conditions were ideal for defensive strategies, as the markets were both choppy and directionless (since September 2014, the S&P 500 (TR) is essentially flat). Both high dividend and low volatility strategies have generally provided historical downside protection in volatile markets.

The S&P 500 Low Volatility Index comprises the 100 least-volatile constituents of the S&P 500, while the S&P 500 Dividend Aristocrats® contains the S&P 500 companies that have increased dividends every year for the past 25 consecutive years. Finance 101 taught us that companies that issue consistent dividends are usually mature, low-growth (read: less volatile) companies. Therefore, in periods when the S&P 500 performs poorly, we could typically expect both the S&P 500 Low Volatility Index and the S&P 500 Dividend Aristocrats to outperform, as both indices are made up of low volatility stocks.

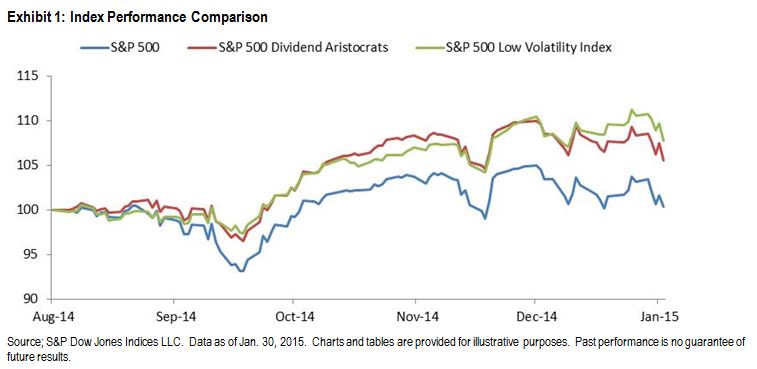

The recent bout of market weakness provided an opportunity to test this hypothesis. While the S&P 500 was flat from September 2014 through January 2015, the S&P 500 Low Volatility Index and the S&P 500 Dividend Aristocrats were up 7.83% and 5.57%, respectively.

Obviously, these strategies are not perfect downside hedges. Over the long term, however, both the S&P 500 Dividend Aristocrats and the S&P 500 Low Volatility Index have tended to offer patient investors protection from declining markets, while providing some exposure to the upside. Though both of these indices tend to underperform the S&P 500 during bull runs, they provide some shelter when the sky starts to fall.

The posts on this blog are opinions, not advice. Please read our Disclaimers.