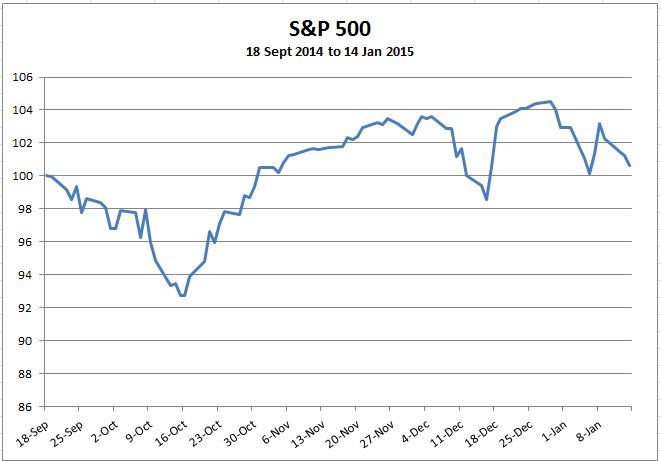

Since last fall, the S&P 500 has gone through three distinct downdrafts. Between September 18 and October 15, the index fell by 7.3%. It recovered that lost ground, and then some, rising

11.8% through December 5. Then a second, less severe, decline began, as the index fell 4.9% between December 5 and December 16, followed by a 6.0% recovery through December 29. This brought the S&P 500 to its (so far!) all-time high. From December 29 through yesterday’s close, the index is down an additional 3.7%. Patterns in the S&P MidCap 400 and S&P SmallCap 600 Indices have been very similar to those in the 500.

The net of these gyrations is a total return of 0.6% in the 82 days since September 18, but with heightened volatility; the standard deviation of daily returns for the S&P 500 was 14.5%. In the 82 days prior to September 18, the standard deviation of daily returns was only 8.0%. So we have just come through a period that is relatively directionless but quite choppy; investors who are preoccupied by the chop may not even notice that their total returns are still positive.

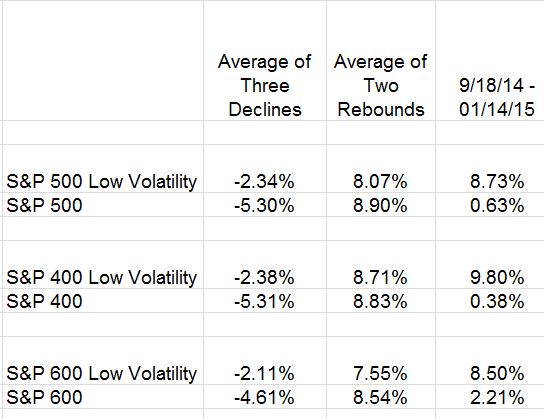

One of the notable things about directionless, choppy markets is that defensive strategies tend to do surprisingly well. The S&P 500 Low Volatility Index, e.g., rose by 8.7% since September 18 — mitigating the three periods of decline, while lagging the S&P 500 during its rebounds. This pattern of protection in down markets and participation in up markets is typical of low volatility strategies, and seems to occur on a global basis. The low volatility flavors of the S&P 400 and S&P 600 also provided protection in the recent down periods and participation in the up moves. It’s not perfect protection, obviously, and it’s not full participation, but the record shows that all three low vol indices performed as we would have expected.

We’re dealing with only four months of data, of course, and past performance is never a guarantee of future results. And it’s fair to say that low vol strategies have historically lagged in a strong market advance. But for investors who want equity exposure, would prefer a smoother ride, and are willing to underperform in a strong market — low volatility strategies may offer a comfortable port in the storm.

The posts on this blog are opinions, not advice. Please read our Disclaimers.