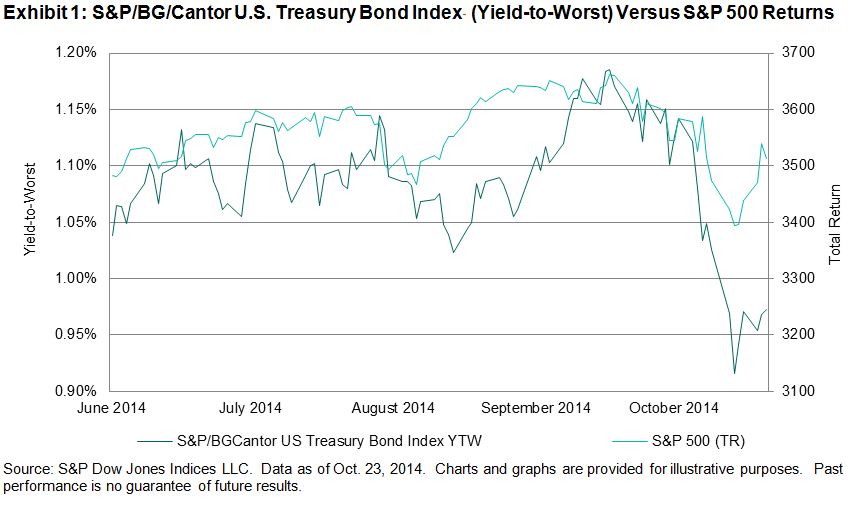

Twenty years from now, some bright young analyst looking at data for the U.S. stock market could be excused for thinking that the S&P 500’s 2.4% total return for October 2014 was no big deal – just one more routine good month in a long bull run. If the analyst is particularly inquisitive, he might wonder why strategies that we typically regard as defensive outperformed – for example, the S&P 500 Dividend Aristocrats (up 4.4%), or the S&P 500 Low Volatility Index (up 4.9%). That’s not what we expect to see in an up month like October – and therein lies our tale.

The key, of course, is to remember that October encompassed two radically different market regimes. Through October 15, the market was in a sharp downdraft, with the S&P 500 falling 5.5%. This was followed by an even sharper recovery in the last half of the month, as the 500 rallied by 8.4%.

We all learn in elementary finance that volatility can reduce returns. If you lose 50% and then make 50%, your compound return is -25%; if you lose 10% and then make 10%, your compound loss is only -1%. Other things equal, lowering volatility can raise returns over time. October is a fine example of that principle in action:

The table shows the performance of the S&P 500 and of three factor or “strategic beta” indices derived from it. All three of these indices can rightly be considered “defensive,” although they achieve their defensive character in different ways. The S&P 500 Dividend Aristocrats Index comprises stocks which have increased their dividends for at least 25 consecutive years, and can be thought of as both a yield and quality play. The S&P 500 Low Volatility Index holds the 100 least volatile stocks in the S&P 500 and tries to exploit the well-known low volatility anomaly. Dynamic VEQTOR is a multi-asset index which owns both the S&P 500 and a long position in VIX index futures.

What defensive indices have in common is that they aim to offer protection from declining markets and participation in rising markets. It’s not perfect protection (the Aristocrats and Low Vol both lost money in the first half of October), and it’s not full participation (all three indices lagged the S&P 500 in the last half of the month). But when the market is choppy, lowering volatility can enhance returns while also lowering risk.

The posts on this blog are opinions, not advice. Please read our Disclaimers.