The recent launch of our S&P Dow Jones Indices India Index Dashboard brought to my notice the S&P BSE Small Cap Index. While the month’s report card was mostly green for the Indian indices due to the optimism in the Indian stock markets, the S&P BSE Small Cap Index did shine through.

- The S&P BSE Small Cap Index returns as on May 30, 2014 was 54.36% (based on total return index) and 51.69% (based on price index). Further, the year to date return was 37.91% while it clocked in a one-month return of 20.41%.

- During the one-year period ending May 30, 2014 the top 3 sectors attributing to this growth were Industrials, Materials and Consumer Discretionary.

- The top contributors to the growth of the index in the one year ending May 30, 2014 were PMC Fincorp Limited and Sulabh Engineers & Services Ltd. Please see the list of top 10 below.

| Security Name | Stock Price Change (%) | Stock Total Return (%) | Contribution To Index Return |

| PMC Fincorp Limited | 501.07% | 501.66% | 2.23% |

| Sulabh Engineers & Services Ltd. | 212.82% | 212.82% | 1.41% |

| Risa International Ltd. | 110.47% | 110.47% | 1.19% |

| Amtek Auto Limited | 178.94% | 179.95% | 1.12% |

| Tilak Finance Limited | 190.74% | 190.74% | 1.11% |

| CCL International Limited | 275.42% | 275.42% | 1.05% |

| Kelvin Fincap Ltd. | 254.49% | 254.49% | 1.02% |

| Sintex Industries Limited | 329.37% | 329.37% | 0.95% |

| VA Tech Wabag Limited | 155.53% | 159.54% | 0.95% |

| PTC India Limited | 97.36% | 97.36% | 0.90% |

Source: Asia Index Pvt. Ltd. Holdings Data as of S&P BSE Small Cap 31 May 2013 through 30 May 2014

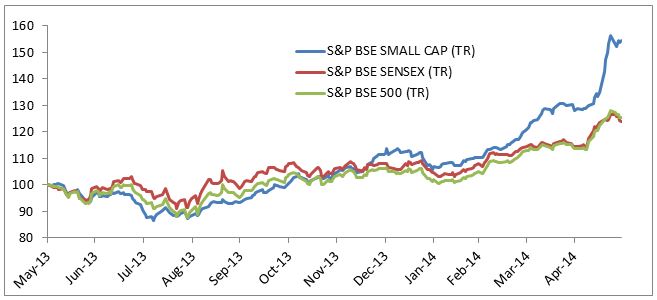

If we compare the S&P BSE Small Cap Index with the benchmark S&P BSE SENSEX or even the broad market representative S&P BSE 500 for this one year period, the outperformance to both these broad market indices is clear.

Source: Asia Index Private Limited, One year total return Performance for the period ending 30 May, 2014

| Indices | One year Total Returns % |

| S&P BSE SMALL CAP (TR) | 54.36% |

| S&P BSE SENSEX (TR) | 24.04% |

| S&P BSE 500 (TR) | 25.52% |

Source: Asia Index Private Limited. One year returns for the one year period from 31 May 2013 to 30 May 2014

| S&P BSE Small Cap Index | |

| Annualized Total Returns | 54.37% |

| Annualized Standard Deviation | 15.17% |

| Return per unit of risk | 3.58 |

The S&P BSE Small Cap performance since inception has been 23.75% (Total return performance dated April 1, 2003 to May 30, 2014)

S&P BSE Small Cap Index is definitely displaying a new trend and one always needs to put this in perspective with the long term performance statistics to gain a better understanding of overall performance.

Capturing sector performance can be easily achieved through passive investing. Passive or index Investing allows investors to gain access to such index returns with very little effort and the ability to track the trends in the sector through its historical performance. In India, the trend of index investing is just about picking up with the existing offering of index funds and ETFs.

The posts on this blog are opinions, not advice. Please read our Disclaimers.

Source: S&P Dow Jones Indices, June 11, 2014

Source: S&P Dow Jones Indices, June 11, 2014