Size, momentum, volatility and value have all been shown to be partly responsible for explaining equity returns over the long run but they do not seem to fully capture the returns of some companies. This has therefore given credence to the idea that a fifth factor – quality – exists and, when combined with other risk factors, acts as a good diversifier in investment portfolios. Click here to read our latest research on this topic or sign up for our webinar via this link: http://bit.ly/1ikwEDv

What is Quality?

There isn’t much agreement on what ‘quality’ is or how it should be measured. Some simply equate it to profitability and others, believing it to be a multi-faceted concept, use more complex measures (e.g. the Piotroski’s F score). Regardless of the approach taken, the aim of any quality measure should help estimate a company’s future profitability and understand its source of risk. Broadly speaking, high-quality companies should generate higher revenue and enjoy more stable growth than the average company. This is why we believe that any good quality measure should take into account profitability generation, earnings quality and financial robustness.

How Does Its Performance Stack Up?

Quality strategies broadly outperformed their benchmarks, both on an absolute and risk-adjusted basis. Among all the regions we examined, the out-performance was highest in the US. In addition, quality strategies held up well in bear markets and although their performance lagged in bull markets, they nonetheless participated in bull market rallies (such as 2003 and 2004).

In What Macroeconomic Environment Does It Do Well?

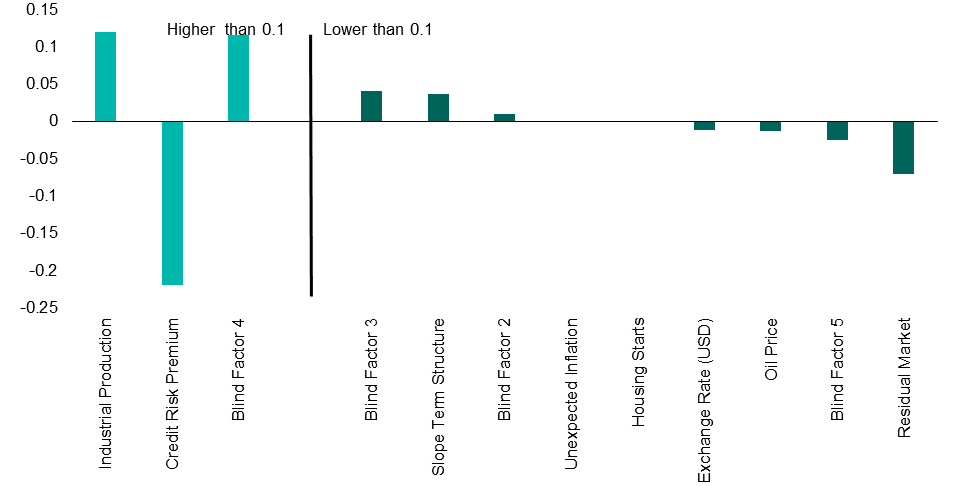

Quality stocks are sensitive to economic growth and tend to deliver higher excess return when the economy slows. That said, their attractiveness diminishes when the economy experiences above-trend growth, although they still deliver positive excess returns. In comparison with the S&P 500, S&P 500 Quality is exposed to industrial production and the narrowing of credit spreads. However, the quality index does not have any significant tilt towards oil prices, inflation, housing starts or the slope of the yield curve.

Source: Figures based on monthly USD total returns between December 1994 and December 2013 on the S&P 500 Quality Index. Charts and graphs are provided for illustrative purposes. Past performance is no guarantee of future results. These charts and graphs may reflect hypothetical historical performance.

OK… There Is Out-performance But Where Does It Come From?

Compared to the S&P 500, S&P 500 Quality has a tilt towards value stocks, lower debt, lower earnings volatility and higher earnings growth – which are attributes usually associated with ‘good quality’ companies.

Source: Figures based on monthly USD total returns between December 1994 and December 2013 on the S&P 500 Quality Index. Charts and graphs are provided for illustrative purposes. Past performance is no guarantee of future results. These charts and graphs may reflect hypothetical historical performance.

More Powerful Together Than Apart?

On the face of it, low volatility and high quality strategies seem very similar but there are important differences between their sources of return. Similarly, because quality strategies also have some tilt towards value stocks, there may be the belief that they are analogous concepts. Results have shown that while quality strategies already perform well by themselves, they appear to be good companions of other alternative beta strategies.

| Combination of Quality and Value Strategies | |||

| Metric | Value | Strategy 1: 50% Value /50% Quality Equal Weight | Strategy 2: Quality on a Value Universe |

| Annualized Return (%) | 5.58 | 6.94 | 11.98 |

| Annualized Risk (%) | 16.63 | 14.93 | 15.13 |

| Return per Unit Risk | 0.31 | 0.46 | 0.79 |

Source: Figures based on monthly USD total returns between December 1994 and December 2013 on the S&P 500 Quality Index and S&P 500 Value Index. Charts and graphs are provided for illustrative purposes. Past performance is no guarantee of future results. These charts and graphs may reflect hypothetical historical performance.

The posts on this blog are opinions, not advice. Please read our Disclaimers.