“A lot of people were hoping this year would turn out to be a stockpickers’ market, but that has turned out to be anything but the case so far” – Troy Gayeski, partner and senior portfolio manager at SkyBridge.

At the beginning of this year, we indicated that despite a chorus of voices to the contrary, 2014 would not prove to be a “stock-picker’s market”. We also speculated that 2014 might well be the first year in which ETF assets overtake those in hedge funds.

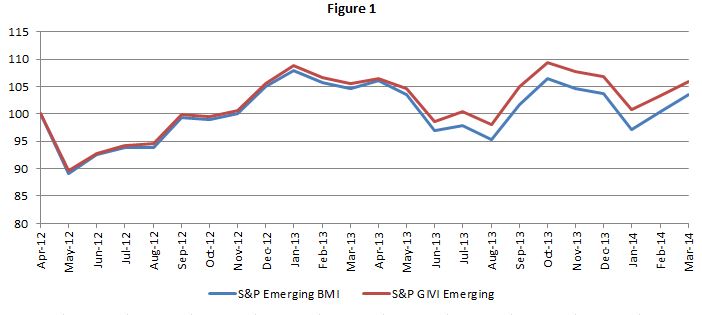

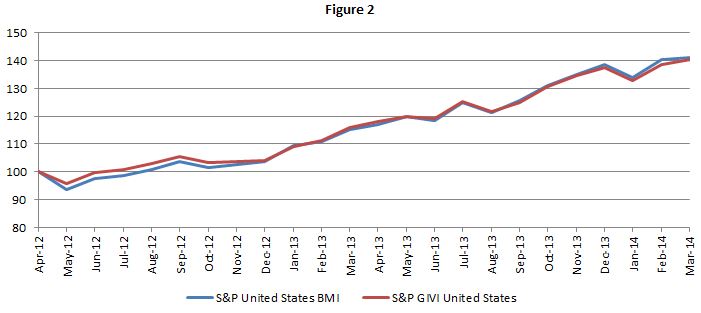

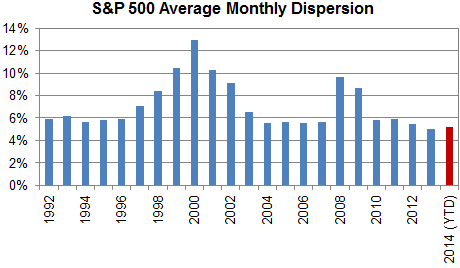

The first prediction was based on the observation that dispersion – a measure of the opportunity set for active management – was at record lows. Combined with dispersion’s historical tendency to change fairly slowly, we anticipated that dispersion would remain low for some time. So far in 2014, it has done:

Source: S&P Dow Jones Indices as of month-end April 2014. Charts provided for illustrative purposes. Past performance is no guarantee of future results.

There are two ways a fund (ETF or otherwise) can gain assets: it can attract new money, or gain new assets through positive returns. Even if hedge funds don’t perform, they may still attract assets; it certainly seems that they have been doing so. On the other hand, the record quarterly flows into hedge funds last quarter were outpaced by assets attracted to ETFs in April alone.

And what of the “stock-pickers” performance? According to today’s Financial Times, so far not so good.

The race is most certainly on…

The posts on this blog are opinions, not advice. Please read our Disclaimers.