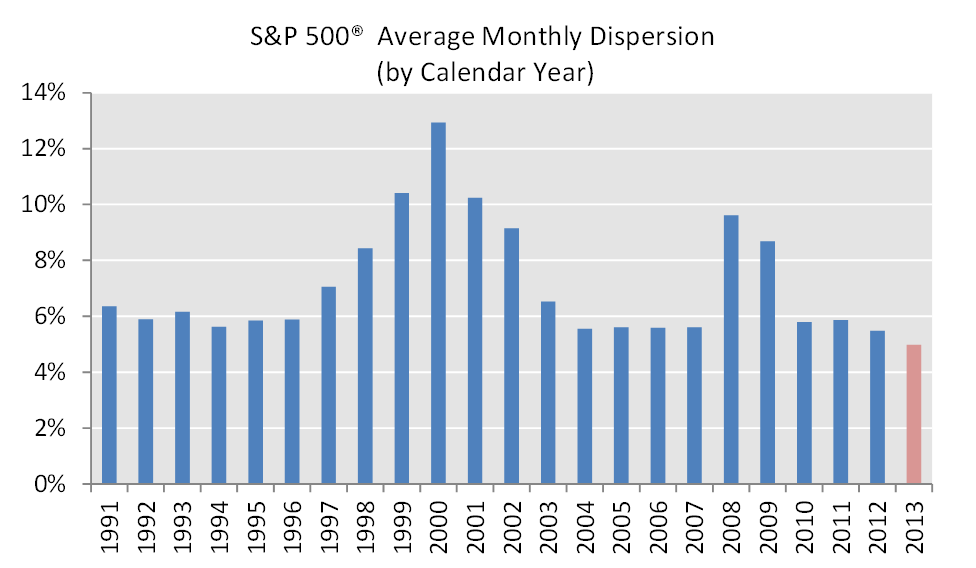

Despite superb returns for the equity markets across the developed world, 2013 was a tough year for active managers. While the average hedge fund recorded fairly solid gains over the year, such performance paled in comparison to the rampant equity markets. It was also a year that saw historic lows for the potential returns available from the expert selection of securities. By some measures, it was the toughest year for stock pickers in decades: rarely in history did the average stock deviate so little from its peers, or from the market1. The average dispersion between S&P 500® stocks over the twelve months of the year was just below 5%, which is the lowest value across the 23-year data set we’ve collected:

Source: S&P Dow Jones Indices, as of January 2014.

In such circumstances, the relative value of active management in the equity markets is constrained. Simply put, accurate bets deliver less alpha. We recently predicted that assets in broad-based index trackers (ETFs in particular) would grow or have already grown larger than the entire hedge fund industry. December’s numbers are now in for both industries2, and it seems that investors have been voting with their feet in favour of our prediction. With the current lack of opportunities facing active managers, who can blame them?

___________________________________________

1. Of course, there were plenty of individual equities that recorded stellar or catastrophic performances. The point is that on average such instances were less commonplace – and less dramatic – than has historically been the case.

2. ETFs assets grew around 2% in December (according to Blackrock)

The posts on this blog are opinions, not advice. Please read our Disclaimers.