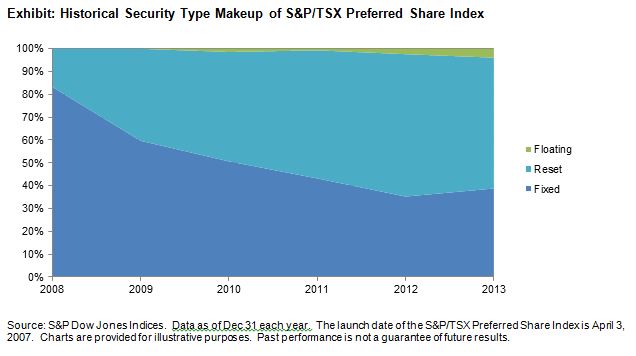

Shift in the Makeup of the Preferred Market

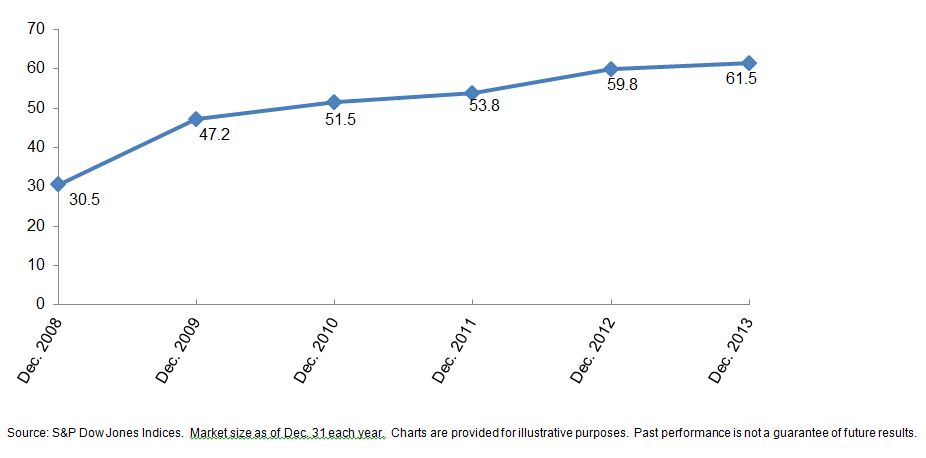

As we noted in an earlier post, the Canadian preferred share market has undergone a significant expansion over the past five years, approximately doubling in market size. In addition to the growth of the market, the Canadian preferred market has seen a shift from most outstanding preferreds being fixed-dividend to a majority being rate-resets. The proliferation of fixed-rate-reset preferreds and their unique distribution characteristics make it possible for investors to get a degree of protection in a rising interest rate environment.

If we take a look at the S&P/TSX Preferred Share Index, which is a proxy for the Canadian Preferred market, by count rate-reset preferreds made up one-sixth of the index in 2008. At the end of 2013, over half of the index was made up of rate-resets.

Types of Preferred Shares Explained

Perpetuals have no set maturity date. The dividend rate is determined at the issuance date and is fixed for the life of the preferred share. With the long time horizon and fixed dividend amount, perpetual shares carry the highest interest rate risk amongst all preferred types.

Retractables pay a fixed dividend and have a pre-determined maturity date, usually redeemable at par value. Most redemption payments are via cash, while some issuers also have the option to pay the equivalent amount in common shares.

Rate Resets are variable dividend payment preferreds, where the dividend rate is reset every five years. The initial dividend rate is determined by adding a spread above a reference rate, most using the Bank of Canada’s five-year bond yield. This spread amount is based on several factors such as the credit quality of the issuer and present market conditions. At each reset date, the dividend rate is adjusted by taking the current interest rate of the reference instrument and adding the spread determined at issuance. Most issuers also hold the option to call the security on each reset date. Because the dividend rate resets based on current market interest rates, the duration and thus interest rate risk, of rate-resets are lower than perpetuals and retractables.

Floating Rate preferreds feature a dividend that floats at each payment, based on a spread above a prime interest rate, such as LIBOR. Typically, a minimum dividend rate is promised to investors to protect them against low market interest rates.

For more on preferreds in Canada, read our recent paper, “Looking Under the Hood of Canadian Preferred Indices.”

The posts on this blog are opinions, not advice. Please read our Disclaimers.