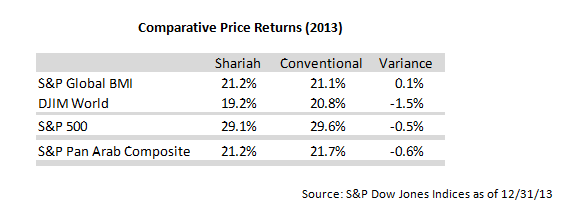

S&P Dow Jones Shariah-compliant benchmarks covering the U.S., MENA and global equity markets performed in line with their conventional counterparts in 2013. In fact, the S&P 500 Shariah, S&P Pan Arab Composite Shariah, and the S&P Global BMI Shariah, each closed the year within 50 basis points of their non-Shariah counterparts – quite remarkable in a year with such high absolute returns. Likewise, the Dow Jones Islamic (DJIM) Market World Index trailed the Dow Jones Global Index by just 1.4% for the year.

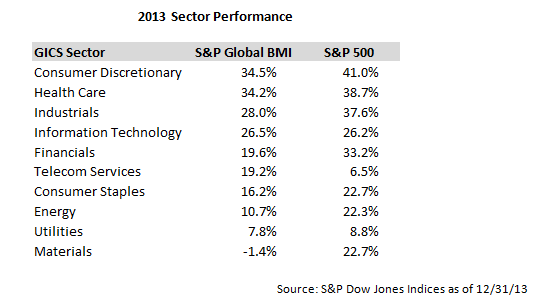

For those unfamiliar with the construction of Shariah-compliant indices, the primary driver of performance differentials stems from the exclusion of most financial services firms from Shariah-compliant benchmarks. As a result, in times when the Financial sector significantly over- or underperforms the overall market, the performance of Shariah-compliant benchmarks tends to diverge from that of conventional indices. In 2013, the Financial sector in the U.S. and global equity markets was roughly in the middle of the pack leading to comparable standard and Shariah-compliant performance.

The DJIM World Index gained 19.2% in 2013, driven by strength in the U.S. and Europe, while DJIM Asia Pacific (4.1%) and DJIM Emerging Markets (-2.2%) significantly underperformed. The blue-chip DJIM Titans 100 performed comparably to its broad market counterpart posting a 21.9% price return for the year.

In the Middle-East, the S&P Pan Arab Composite Shariah gained 21.2% in 2013, driven by the 23.3% return of the S&P Saudi Arabia Shariah, which comprises approximately half of the index.

The U.A.E. was the star performer for the year in the GCC and globally, as the S&P U.A.E. Shariah Index more than doubled in 2013. The country’s stock market was buoyed by continued recovery in its real estate market and the announcement of an upgrade from frontier to emerging market status from several major index providers, including S&P Dow Jones Indices.

To find out more about our Shariah Indices Click Here

The posts on this blog are opinions, not advice. Please read our Disclaimers.