The market’s malaise and its poor results on Thursday August 15th are being blamed on fears of Fed tapering. Unless the Fed has a surprise change of heart, these fears will be with until tapering starts, so examining them is worthwhile. Most signs suggest the economy will continue to gain strength. Weekly initial unemployment claims continue to fall, signaling both economic strength and raising hopes for a lower unemployment rate. Inflation is under control, but is closing in on the Fed’s 2% target. Housing, which was a powerful positive in the first half, is showing some mixed numbers (see our Housing Views blog), but those may reflect the same interest rate worries. The result is that either the economy takes a sudden, unexpected tumble or the Fed will decide to scale back its bond buying. While timing is unknown, the popular guesses all focus on the month of October.

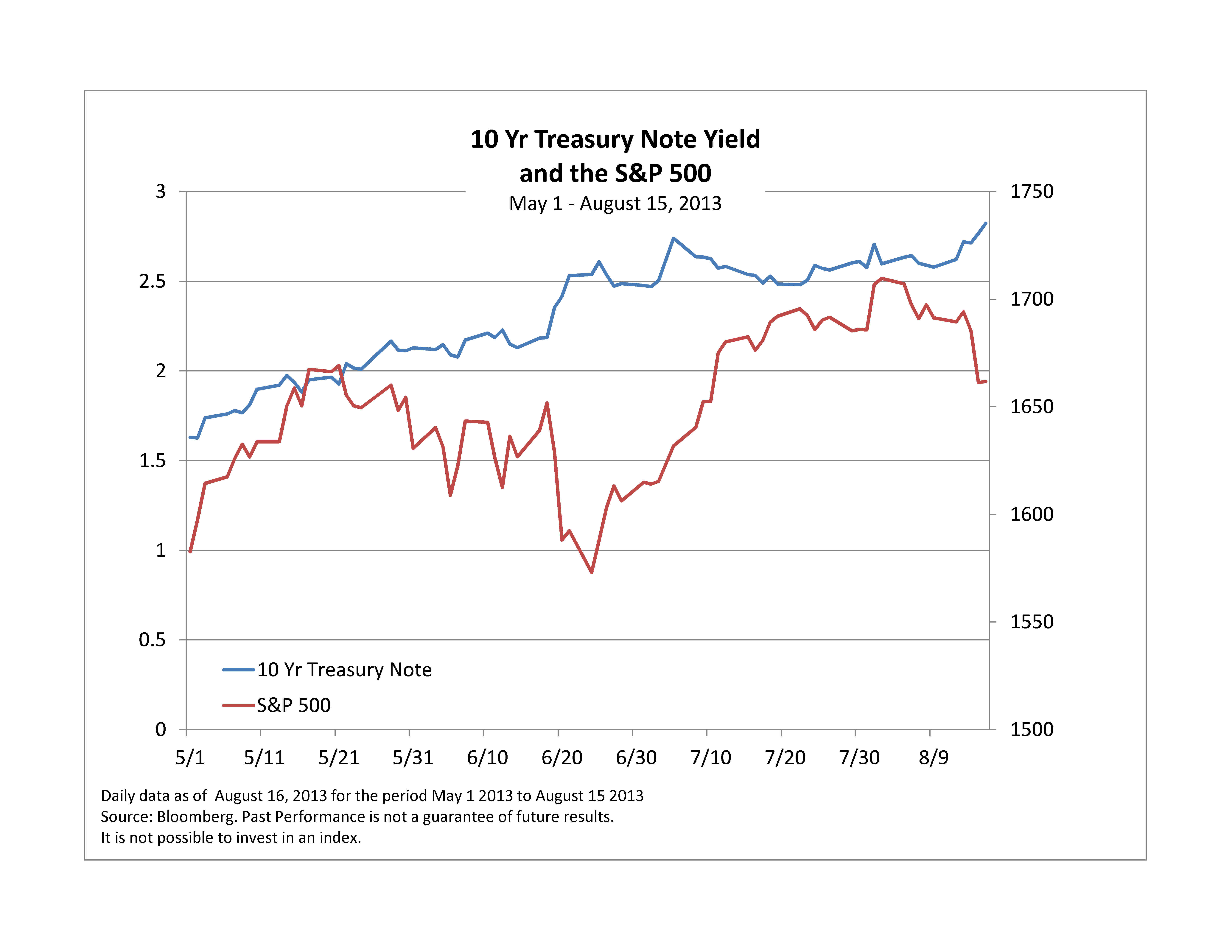

What will happen? The chart shows the 10 year treasury and the S&P 500 since May 1st of this year. Yields will go up. Further, no matter how fast people think they will rise, some of us will be spooked because they’ll rise a lot faster. At almost the same time, stock prices will tumble and VIX will surge. A very rough gauge of the damage can be found in the damage done last May and June. The S&P 500 fell from 1669.16 on May 21st to1573.09 on June 24th losing 5.7% in a bit over a month. The rise in yields was more gradual but also more damaging. The 10 year treasury was yielding 1.63% at the beginning of May. Using almost the same dates as for the S&P 500, the yield rose from 1.93% on May 21st to 2.61% on June 25th, an increase of 68 bp, or more than a third.

The chart shows that the pattern after the initial collapse is quite different for stocks and bonds. The S&P 500 recovered and made new highs in early August; yields continued to rise, pushing bond prices lower. Why did stocks recover while bonds faded slowly? The root cause of all this is the strengthening economy and the Fed’s response. A better economy should be good news for stocks, at least good enough to support something of a bounce back. The same economic news adds support to those expecting tapering from the Fed and limits the recovering in bonds. The last few days shown on the chart suggest we may be in a replay of the May-June game now.

A few bits of caution: first, we’re looking at fears or expectations of tapering; no one – except the members of the Fed’s FOMC – has any real idea of when tapering will happen. Second, as important as the Fed is, it is not the only thing investors are worried about. The top stories and headlines in the last week include more turmoil in the Mid-East which drove oil well above $100/barrel along with more reports that China’s economy is slowing down. And then there’s the upcoming Congressional battle over the debt ceiling. No shortage of things to worry about.

The posts on this blog are opinions, not advice. Please read our Disclaimers.