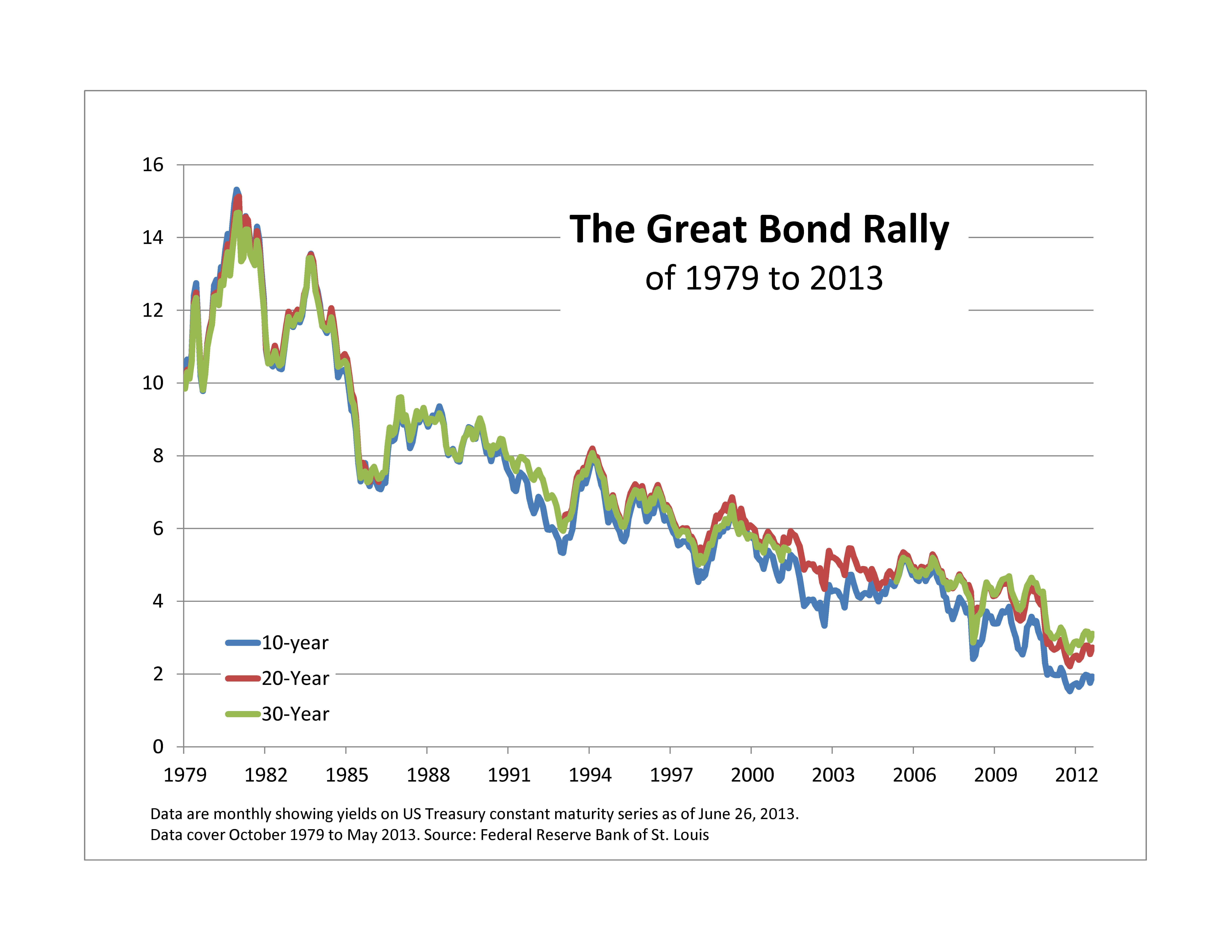

Whenever you want to argue that rising interest rates are bad for the stock market, count June 2013 as a point in your favor. The long end of the US Treasury yield curve notched a -4.07% decline in June (following May’s -6.71% tumble), as rates on the S&P/BGCantor 20+ Year US Treasury Index rose by 66 basis points from their April low. Equities followed suit, with the S&P 500, e.g., off -1.34% for the month.

June, in that sense, feels like a conventional down month (unlike May, when equities rallied despite wretched bond performance). Defensive sectors (Telecom, Utilities) were the best performers, while more cyclically-sensitive sectors (Materials, Information Technology, Energy) were the worst. The US outpaced the rest of the developed world (with the sole exception of Japan) in June and for the first six months of 2013, and emerging markets lagged even further behind. US equities might not be, as we’ve suggested previously, the very best house in a bad neighborhood, but they’re not far off that mark.

The brightest spots in June’s US performance came from defensive strategy indices. The S&P 500 Low Volatility Index actually rose (+0.60%) in June, and yield-sensitive strategies like the S&P 500 Value or the Dow Jones US Select Dividend Indices outperformed broad market gauges. Volatility was the month’s biggest winner, as the S&P 500 VIX Short-Term Futures Index gained +7.26%. Volatility’s performance also benefited the S&P 500 Dynamic VEQTOR Index, which allocates between stocks and vol, and rose +0.42% in June.

The posts on this blog are opinions, not advice. Please read our Disclaimers.