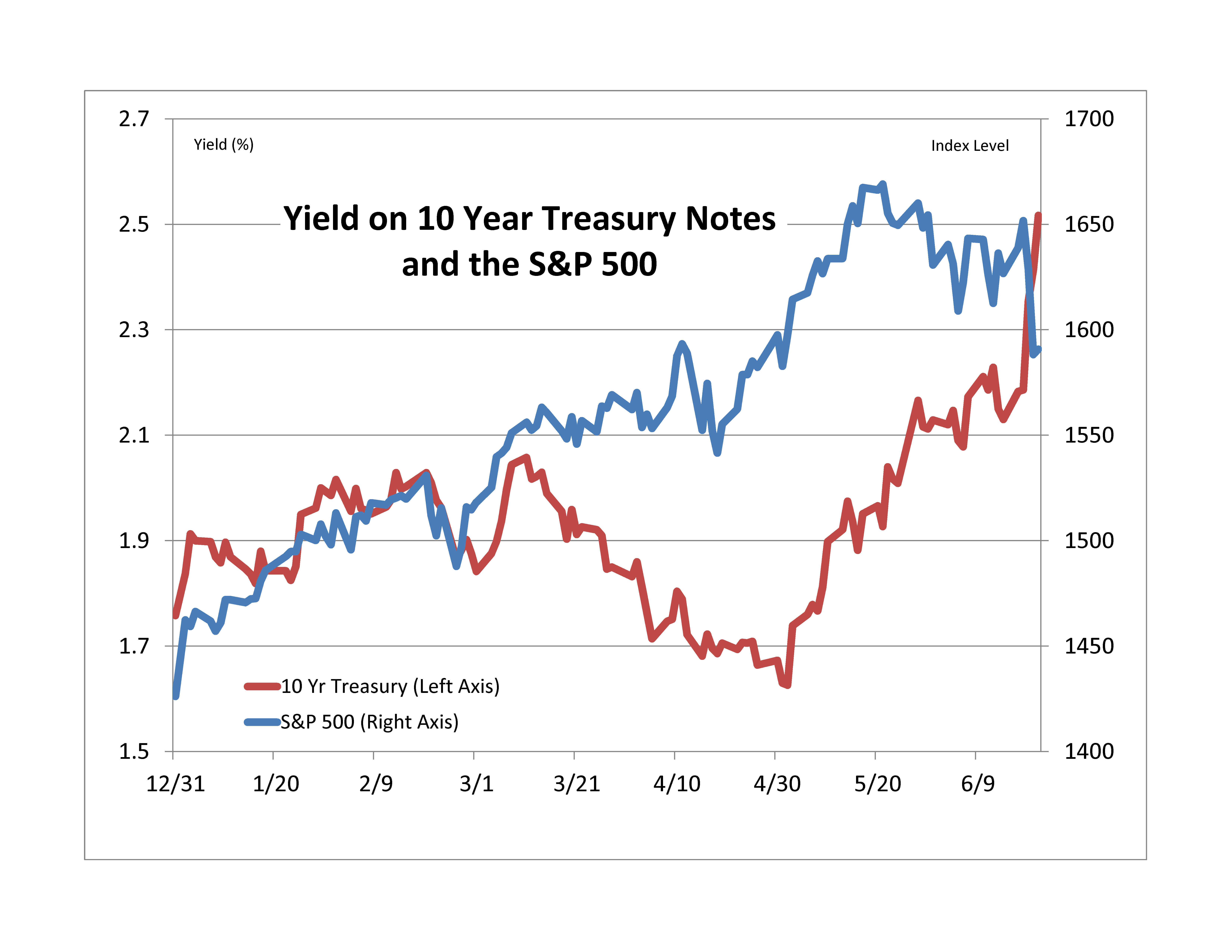

Compared to a month ago, every major developed equity market is down, some by double digits while bond yields have climbed over the same period. The U.S. markets – both stocks and bonds — are among the least damaged. For investors the questions are when will it end?, where can one hide? and why?

When will it end?

Assume that the Fed’s forecast is right and the economy is improving and will continue to improve. Then the fortunes of stocks and bonds are likely to split with stocks recovering while bonds continue to suffer. An improving economy should help stocks turnaround while the Fed’s less generous attitude combined with economic strength means bond yields will rise more. Markets tend to over react and overshoot when shocked as they were last week. Beware a bounce in stocks or bonds creating a false sense of security for all. If the Fed is too optimistic and the economy falters, we will see QE4; but, we might be too nervous to take advantage of it.

Where can one hide?

Not bonds, maybe stocks. Maybe the silver lining is we’ve seen the first tiny steps to being able to earn a (small) return on cash.

What happened?

Everyone knew that one day the Fed would end Quantitative Easing but everyone believed that that day would never come. Then the Fed suggested a date – beginning of the end this fall, the end of the end next summer. If your ten year treasury is worth 100 today and will be worth 90 next summer, you don’t wait to sell it. You sell it now and all that selling makes it worth 90 now. This is what happened. Rather than complaining about the fickle Fed, remember their job is to worry about what could go wrong, lean against the wind and act as “the chaperone who has ordered the punch bowl removed when the party was really warming up.” (The quote is from William McC. Martin, Fed chairman in the 1950s and 1960s, credit to the Conversable Economist blog for the citation and a copy of the speech.)

Scorecard:

S&P 500 down 4.7% and DJIA down 4.3% from the close on Tuesday 6/18 to the close on Monday 6/24. 10 year Treasury note yield rose 38 bp or 17% over same time period.

The posts on this blog are opinions, not advice. Please read our Disclaimers.