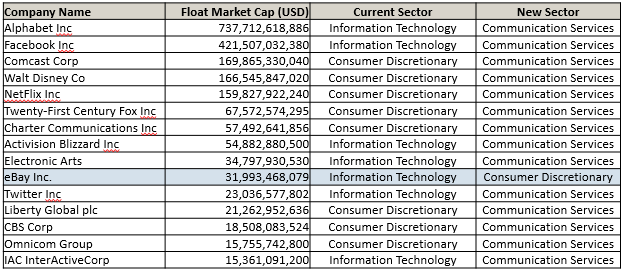

At last Friday’s close, S&P Dow Jones assigned a number of technology and consumer discretionary names into a new “Communication Services” sector classification. Relative to the old Telecommunication Services definitions, the sector has grown from 3 to 22 companies (not counting dual share listings) and is less concentrated in absolute terms. However, Communications Services remains a relatively concentrated sector; its top five largest companies account for nearly three quarters of the sector’s capitalisation.

And although the departure of Alphabet and Facebook has slightly reduced the concentration of the top-heavy IT sector, Amazon’s dominance of the Consumer Discretionary sector has been increased by the departure of names such as Netflix and Disney. In fact, the top 5 names in each sector currently account for more than 50% of capitalisation in 5 out of 11 sectors.

It’s not just sectors that have increased in concentration recently; the overall market has too. At 15.3% of total market capitalisation, the largest five companies (currently Apple, Microsoft, Amazon, Alphabet and Berkshire Hathaway) represent a larger share of the S&P 500 today than at any year-end since the turn of the century.

Changes in market concentration levels have a natural impact on the performance of equal-weight indices. As the largest stocks outperform, the market becomes more concentrated in those names and (all else being equal), cap-weighted indices will outperform equal-weight indices. And as we have previously examined in some detail, the overall performance of equal weight indices seems to be closely tied to trends in concentration, particularly at the sector level.

The present market circumstances, therefore, could present an opportunity for investors to reevaluate equal weight approaches in U.S. equities. If the risks of the market are concentrated into a select few, high-momentum mega-cap names, one way to manage that risk is to de-allocate from the very largest stocks, and rebalance away from recently outperforming constituents. And if the current low-correlation environment continues, equal weight indices may also offer an effective way to benefit from the greater diversification potential of putting fewer large eggs in your U.S. equity basket.

The posts on this blog are opinions, not advice. Please read our Disclaimers.