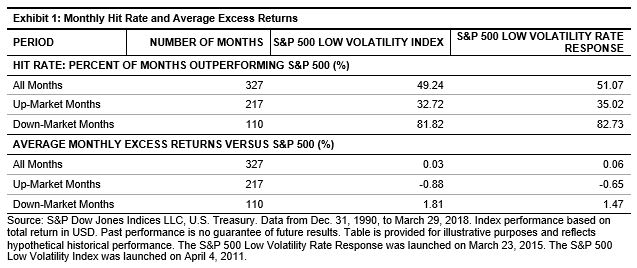

In the second blog of this series, we saw that the S&P 500® Low Volatility Rate Response generally achieved similar levels of volatility reduction as the S&P 500 Low Volatility Index. In our paper Inside Low Volatility Indices (published in 2016), the low volatility index historically outperformed the S&P 500 during severe market downturns (Exhibit 5 in the paper) due to lower beta to market and lower realized portfolio volatility. In this final blog, we examine if the rate response strategy achieves a similar level of volatility reduction as the low volatility strategy in those down-market periods.

We first looked at monthly up-market and down-market hit rates, along with the average excess monthly returns (see Exhibit 1).

For all periods, the two strategies had similar hit rates of about 50%, with the rate response index having a slightly higher hit rate (51% to 49%). While these two indices underperformed the S&P 500 half of the time, the returns seen in the first blog show that the rate response and low volatility indices outperformed the S&P 500 on a cumulative basis over the long-term investment horizon. What could be the cause of this? We investigated by looking at the monthly returns broken down between up markets and down markets.

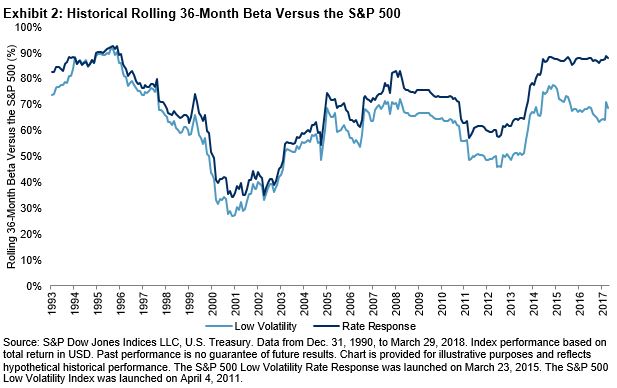

In up markets, the low volatility and rate response indices underperformed the S&P 500 the majority of the time. This is not surprising, given their beta to market—Exhibit 2 shows the historical rolling 36-month betas of the two low volatility strategies compared with the S&P 500. The average 36-month beta for the rate response index was 69.9%, compared with 62.2% for the low volatility index. Nevertheless, the higher beta exhibited by the rate response index means upside participation of the strategy could be higher than that of the low volatility index. In fact, the average monthly underperformance for the low volatility index was 0.88% and 0.65% for the rate response index.

In down markets however, both indices outperformed the S&P 500 more than 80% of the time. The average excess return in down markets for the rate response index was 1.47%, slightly lower than the low volatility index (1.81%). Therefore, the relative outperformance of both indices versus the S&P 500 in down-market periods was markedly higher than the underperformance in up markets.

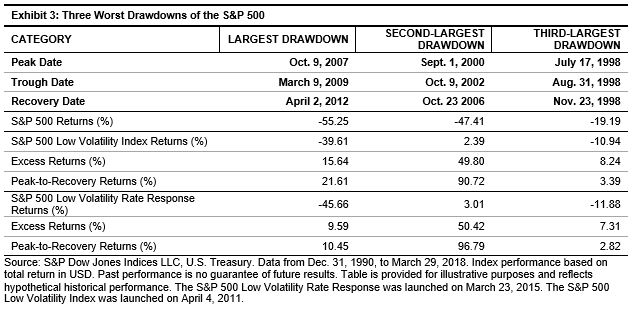

In addition, a simple compounding mathematical rule requires that for a given percentage portfolio decline, a higher percentage gain is required to get back to even. This compounding effect also helps explain the cumulative positive excess returns. Next, to study extreme bear markets, we looked at the three largest drawdown periods for the S&P 500 since 1991.

The rate response strategy performed similarly to the low volatility index—outperforming the S&P 500 in all three periods. The largest performance difference came during the tech bust in the early 2000s. While the S&P 500 dropped by over 47%, the rate response and low volatility indices had positive absolute returns. The cumulative outperformance impact relative to the S&P 500 can been understood by calculating the peak-to-recovery period return. For this date range, the low volatility index outperformed the S&P 500 by 91%, while the rate response index outperformed by 97%.

The analysis in this post shows that the rate response index was able to deliver similar historical performance as the low volatility index—more importantly, their down-market returns were similar. Along with the analysis shown in prior posts in this series, the S&P 500 Low Volatility Rate Response is a variation of the S&P 500 Low Volatility Index, designed for rising interest rate environments. The index reduces rising interest rate risk, while still delivering lower realized portfolio volatility—a salient characteristic of low volatility investing.

The posts on this blog are opinions, not advice. Please read our Disclaimers.