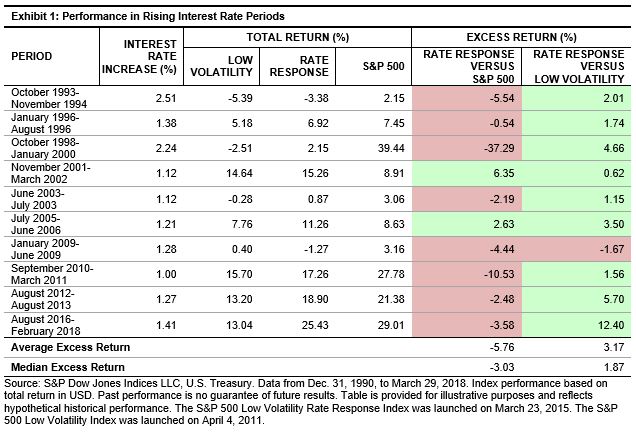

Previously, we highlighted that the S&P 500® Low Volatility Rate Response Index fared better than the S&P 500 Low Volatility Index when interest rates increased. The objective of low volatility portfolios is to deliver lower portfolio volatility than the broad market benchmark, leading to higher risk-adjusted returns over a long-term investment horizon.

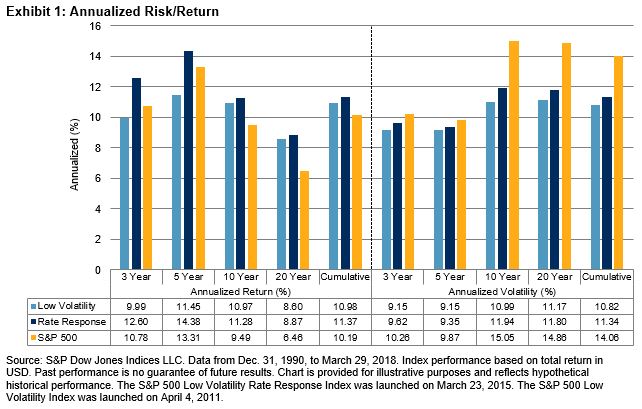

In this blog, we demonstrate that minimizing the interest rate exposure does not have to come at the expense of portfolio volatility reduction. We first look at a multi-horizon risk/return chart for the two indices compared with the S&P 500, going back to 1991 (see Exhibit 1).

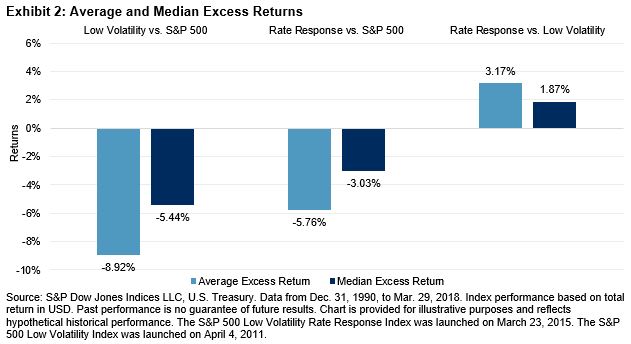

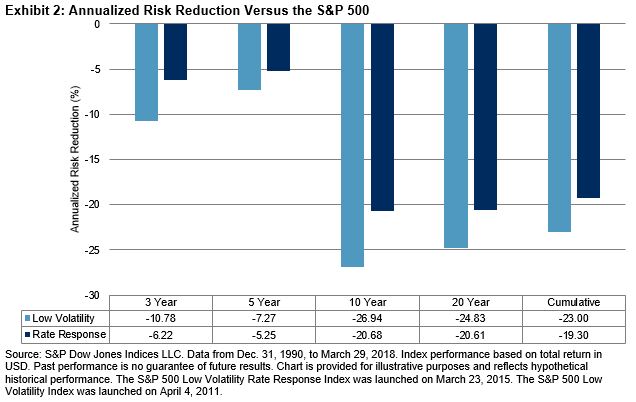

Over the longer time horizons, the low volatility and rate response indices outperformed the S&P 500, with lower volatility. In fact, the rate response index performed better than both the low volatility index and the S&P 500 for all measured periods. The rate response index was slightly more volatile than the low volatility index—nevertheless, it had a cumulative risk reduction of 19.3% relative to the S&P 500 (the low volatility index had a risk reduction of 23%). Exhibit 2 shows the annualized risk reduction of the two strategies compared with the S&P 500 for the different periods.

Exhibit 2 shows that both the rate response and low volatility indices had lower volatility than the S&P 500 across different lookback periods. In recent years, stocks have been in one of the longest-running bull markets with low volatility, leading to somewhat moderate volatility reduction for the two indices. However, for the time horizons that cover at least one full market cycle (bull and bear markets), the risk reduction of the two indices versus the S&P 500 was more evident.

Together with the analysis provided in the first blog, we have seen that the rate response index has been able to perform better than the low volatility index in periods of rising interest rates, while also retaining the volatility reduction characteristics of a low volatility strategy. In a future post, we will further examine the relative exposure of interest rate changes between the rate response and low volatility indices.

The posts on this blog are opinions, not advice. Please read our Disclaimers.