Factor investing has continued to gain momentum in recent years, but the strategy has been predominantly adopted in the developed markets, and research on factor-based strategies in emerging markets remains scarce. Emerging markets (as measured by the S&P Emerging BMI) returned -13.52% in 2015 but recouped most of the losses in 2016 with a return of 11.3%, and they advanced 13.62% in the first four months of 2017. With the rebound, market participants may find that there are ample opportunities offering value in emerging markets. As such, a value-based strategy combined with momentum could help identify cheaply priced securities that are on the upswing.

We explored how a factor-based strategy would perform in Latin America by constructing a hypothetical value and momentum portfolio (“Latin America Value Momentum Strategy”). It should be noted that combining value and momentum is the most commonly employed multi-factor strategy due to the negative correlation demonstrated between the two factors. The historical correlation between value and momentum factors in Latin American is -0.44 over the past decade.

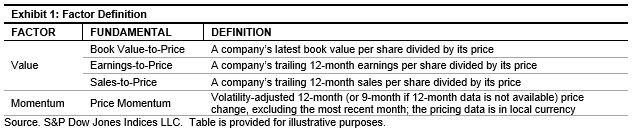

Adopting the metrics behind the S&P Enhanced Value and Momentum indices, we used three fundamentals—book value-to-price, earnings-to-price, and sales-to-price—to proxy the return to value factor, and a stock’s 12-month price change adjusted by its volatility is used to capture the price momentum. The weight of a security in the portfolio is the product of its factor score and its float-adjusted market cap. The portfolios were rebalanced on a semiannual basis in June and December.

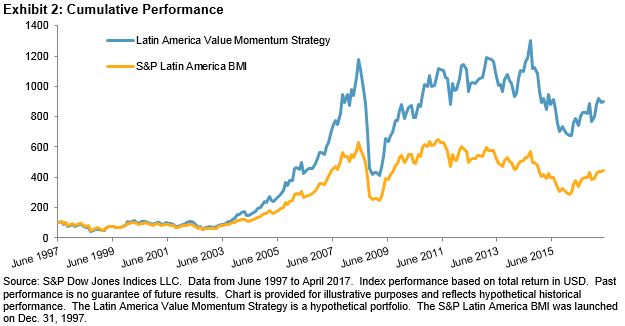

Over the back-tested period, the strategy delivered compelling cumulative returns compared to the broad, market-cap-weighted benchmark. In nearly 20 years, the multi-factor strategy delivered 798% of cumulative return (see Exhibit 2). During the same period, the broad market only produced one-half of the gains that the strategy provided, with 342% of total growth.

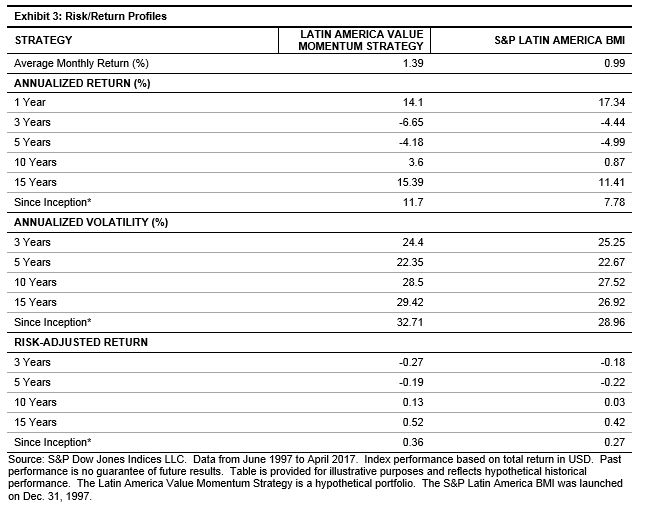

The multi-factor strategy produced an average monthly return of 1.39%, compared to the 0.99% return of the broad market. The most noticeable performance differential can be seen over a longer time frame (five years or more). The strategy demonstrated risk-adjusted returns of 0.13 and 0.52 in the 10- and 15-year periods, respectively. Both figures are significantly higher than benchmark’s 0.03 and 0.42 risk-adjusted returns over the respective periods. The result is less effective in short-term, as shown in three-year time horizon, with a -0.27 risk-adjusted return for the strategy versus the benchmark’s -0.18 (see Exhibit 3).

Our analysis of the combined value and momentum strategy in Latin America shows that factor-based investing can work effectively in the region over the long-term investment horizon. The same strategy may deliver different results in individual Latin American countries due to specific market conditions, which is discussed in our related paper “Value and Momentum Strategies in Latin America” and will be also explored in upcoming blogs.

The posts on this blog are opinions, not advice. Please read our Disclaimers.