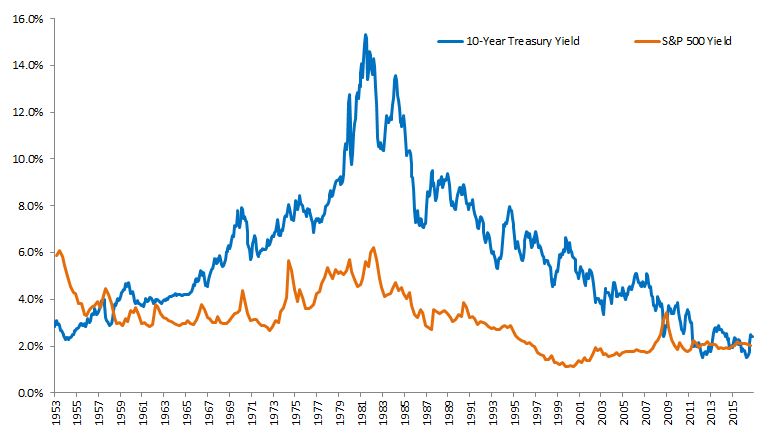

This morning’s Wall Street Journal reported, rather breathlessly, that “U.S. bond yields are topping a key measure of the dividends that large U.S. companies pay—a shift that has broad implications for investors….” The headline was triggered by the observation that the 2.50% “yield on the 10-year U.S. Treasury note…exceeded the 1.91% dividend yield on the S&P 500.”

Does this fact have important implications? On the contrary, we’d argue that this isn’t news, and that it tells us nothing about the market’s future direction. For historical context consider the chart below:

In September 1958, the yield on the 10-year Treasury note rose above that of the S&P 500, a condition which continued unabated for the next 50 years. Stock yields rose above bond yields briefly at the end of 2008, but have remained below bond rates for most of the time since then. In other words, for the vast majority of recent history, the yield on bonds has exceeded the yield on stocks.

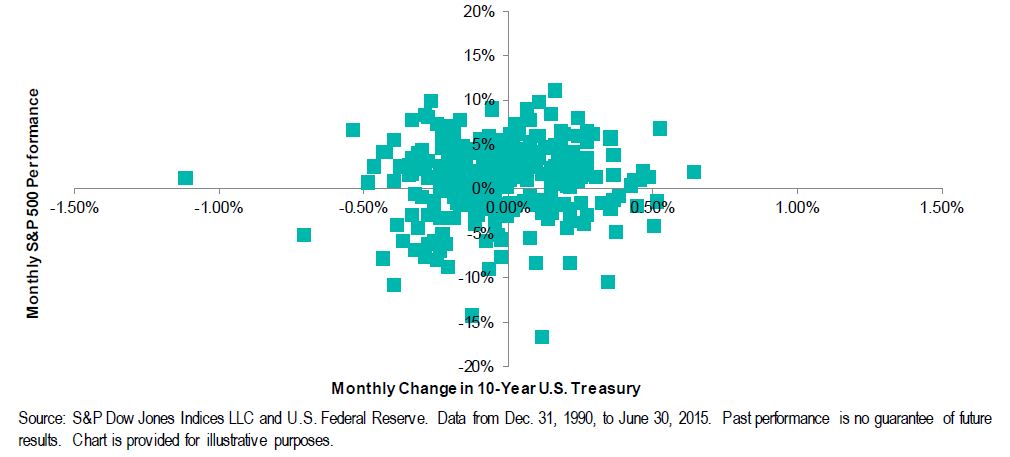

Does the current upward move in interest rates pose “a threat” to the stock market, as the Journal suggests? The historical evidence here is ambiguous; since 1991, the average return for the S&P 500 has been higher in months when interest rates rose than in months when rates fell. There is clearly no concrete relationship between the direction of rates and the direction of the stock market, as the chart below makes clear:

It’s certainly possible that increased competition from higher bond rates will cause weakness in the equity market. It’s equally possible that the economic strength which is producing higher bond yields will also sustain earnings and stock prices. In either event, the news that bonds yield more than stocks hardly qualifies as news at all.

The posts on this blog are opinions, not advice. Please read our Disclaimers.