This is a series of blog posts relating to the in depth analysis of performance differential between the S&P SmallCap 600 and the Russell 2000.

Benchmarks are designed to represent a passive strategy in a given universe. Given that purpose, the risk/return profiles among various benchmarks in the same universe should be relatively similar in nature. This similarity appears to be borne out in the U.S. large-cap equity universe when comparing the returns of the Russell 1000® and the S&P 500®. Using monthly total returns from 1994 to 2014, Exhibit 1 charts the growth of a hypothetical investment of USD 1.00 in the S&P 500 and the Russell 1000, as well as in the S&P SmallCap 600 and the Russell 2000. In the U.S. large-cap universe, USD 1.00 invested in the S&P 500 and the Russell 1000 from January 1994 through December 2014 would have returned USD 6.63 and USD 6.80, respectively. However, in the small-cap universe, the returns of the Russell 2000 and the S&P SmallCap 600 are considerably different. An investment of USD 1.00 in the S&P SmallCap 600 over the same time period would have returned USD 8.59, while it would have returned USD 6.18 if invested in the Russell 2000.

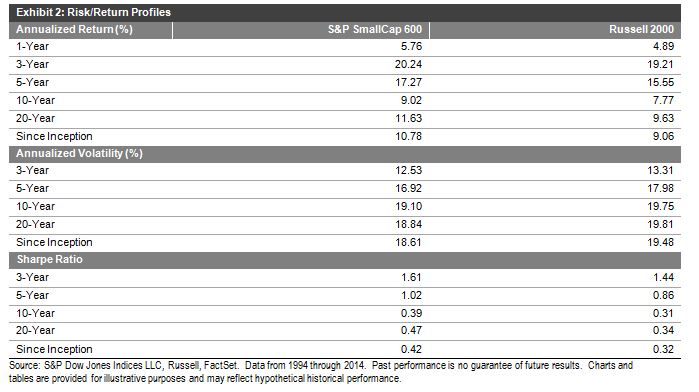

Since its launch in 1994, the S&P SmallCap 600 has outperformed the Russell 2000 in 14 of 21 calendar years. From January 1994 through December 2014, the returns of the S&P SmallCap 600 exceeded those of the Russell 2000 by 1.72% on an annualized basis. It is also important to note that the S&P SmallCap 600 has exhibited lower volatility than the Russell 2000 historically, leading to a higher Sharpe Ratio. These results are similar to what was seen in the previous research paper on this topic (2%), when the time range reviewed was from 1994 to 2009. Exhibit 2 highlights the risk/return profiles of the two indices.

The continued return differential between the two small-cap indices merits further study, and an understanding of the factors contributing to the divergence. We will be covering those in detail in upcoming blog posts!

The posts on this blog are opinions, not advice. Please read our Disclaimers.

{kind=link}