The current cold snap that has descended upon the east coast of the U.S. has winter temperatures on par with its neighboring country to the north. In addition to the weather, the Canadian bond market has seen its share of interest, as on Jan. 21, 2015, the Bank of Canada (BOC) cut rates by 25 bps to an overnight lending level of 0.75%. The need for the BOC to act was created by sliding inflation, weaker crude prices (which threaten domestic sand oil production), and lagging employment growth.

After the news, Canadian sovereign bonds, as measured by the S&P Canada Sovereign Bond Index, rallied by 0.45%, and this continued into Jan. 23, 2015, with a 0.30% daily total return. The index closed the month of January at 3.77%, and it has returned 3.86% YTD as of Feb. 2, 2015. In comparison, the S&P/BGCantor US Treasury Bond Index has returned 2.00% YTD as of Feb. 2, 2015.

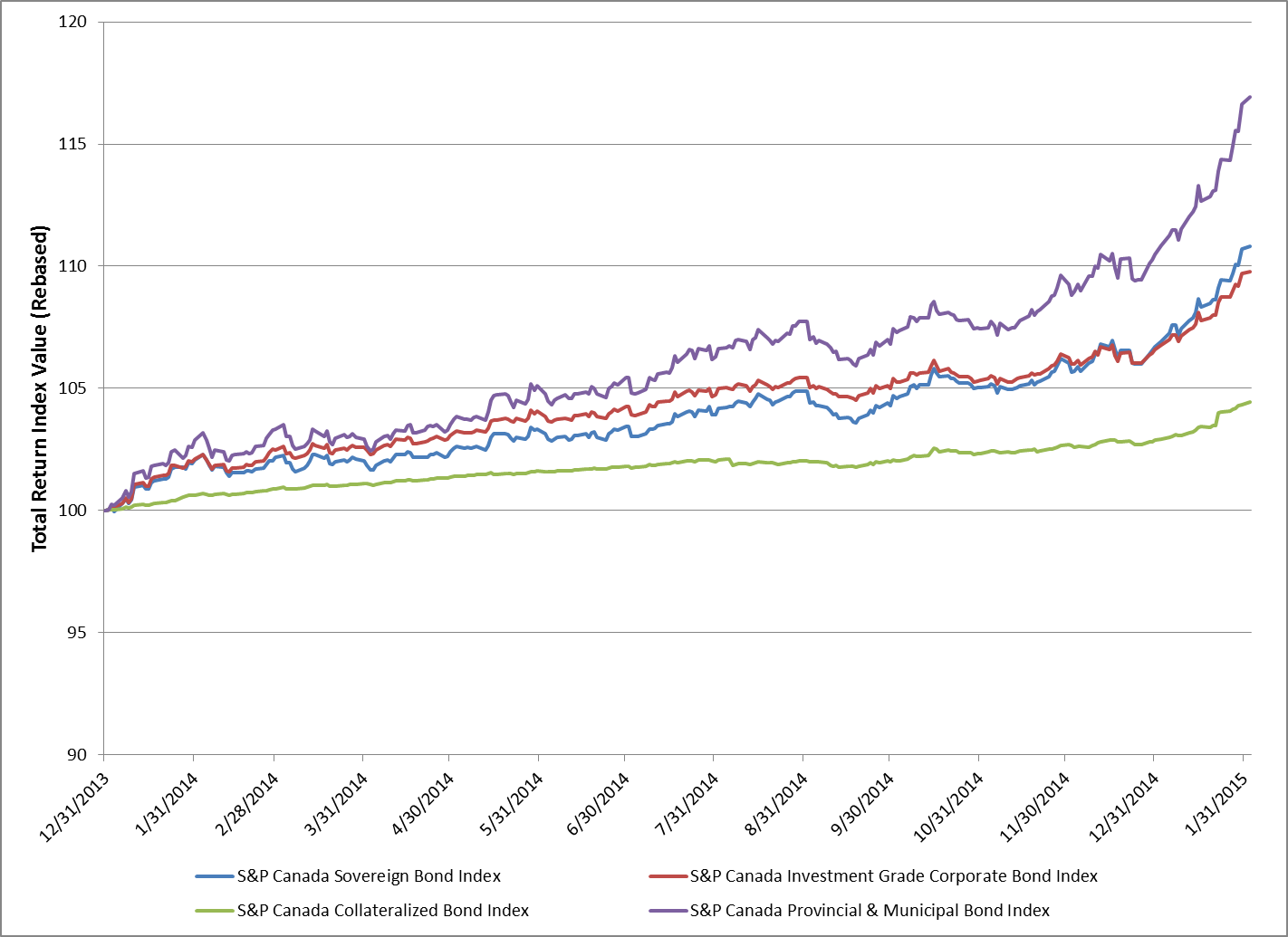

Along with sovereigns, performance of additional segments of the Canadian fixed income market has been just as impressive. Exhibit 1 shows that over the course of the last year, investment-grade corporates (as measured by the S&P Canada Investment Grade Corporate Bond Index) have tracked sovereigns tightly and recently began to underperform sovereigns. As of Feb. 2, 2015, the S&P Canada Investment Grade Corporate Bond Index has returned 3.01% YTD. Since the beginning of the year, the performance for all components of the S&P Canada Aggregate Bond Index has been strong. The leader of the pack (including sovereigns, provincials and municipals, corporates, and collateralized bonds) has been the S&P Canada Provincial & Municipal Bond Index. After returning 10.48% in 2014, this segment of the Canadian market has returned 5.83% YTD (as of Feb. 2, 2015). The combination of yield and a government guarantee has led to significant 2015 performance for securities in this index, with issuers such as Canada Mortgage and Housing, the Province of Quebec, Saskatchewan, British Columbia, and Ontario being some of the top performers.

The laggard of the group is the S&P Canada Collateralized Bond Index, which has returned 1.54% YTD as of Feb. 2, 2015, but the index represents less than 1% of the S&P Canada Aggregate Bond Index.

Exhibit 1: Total Returns of Canadian Bond Indices

Source: S&P Dow Jones Indices LLC. Data as of Feb. 2, 2015. Charts and tables are provided for illustrative purposes. Past performance is no guarantee of future results.

The posts on this blog are opinions, not advice. Please read our Disclaimers.