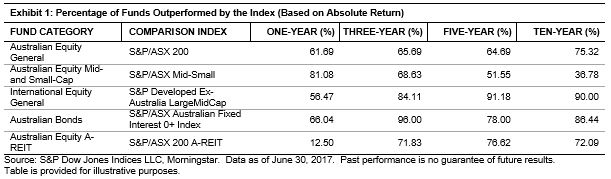

In a recent Financial Planning article,[1] Craig Israelsen advocated using stock market size segments to construct portfolios rather than a total market approach. His conclusion may be perfectly valid for market participants willing and able to bear greater small-stock exposure, but his analysis fails to adequately take account of this source of risk. He compared returns of several index funds and reviewed results of combining them in a couple of different ways. The sample period was from 1999 through 2016, and the funds used in his analysis were:

- Vanguard Total Stock Market Index Investor (VTSMX);

- Vanguard 500 Index Investor (VFINX);

- Vanguard Mid-Cap Index Investor (VIMSX); and

- Vanguard Small-Cap Index Investor (NAESX).

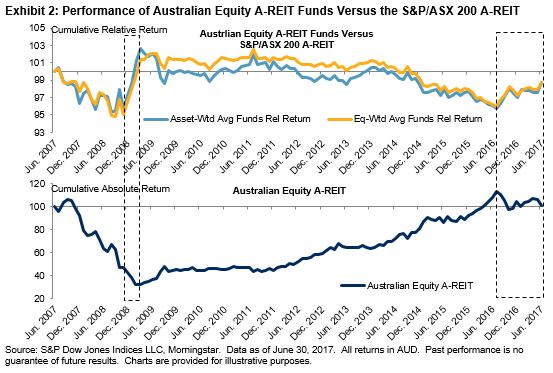

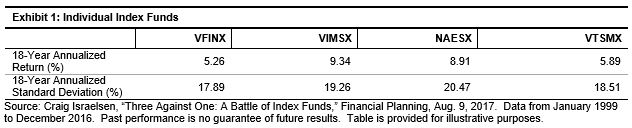

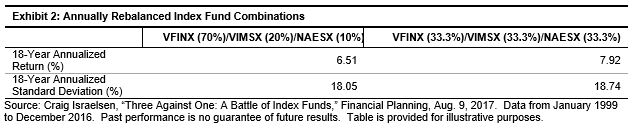

The results over this 18-year period are summarized in Exhibits 1 and 2.

One of the article’s conclusions is that the Vanguard Total Stock Market Index Investor fund failed to meaningfully capture mid- and small-cap returns within its portfolio, because it is dominated by large-cap stocks and experienced historical returns pretty close to those of the large-cap Vanguard 500 Index Investor fund. One can debate what is or is not a meaningful difference in performance, but the Vanguard Total Stock Market Index Investor fund returned 63 bps more per year on average than the large-cap fund. That does not seem insignificant and is slightly greater than the performance pick-up of 62 bps per year that Israelsen found over the Vanguard Total Stock Market Index Investor by approximating its market cap weights with individual size segments, which is the 70/20/10 strategy. This performance enhancement, however, has some dubious underpinnings.

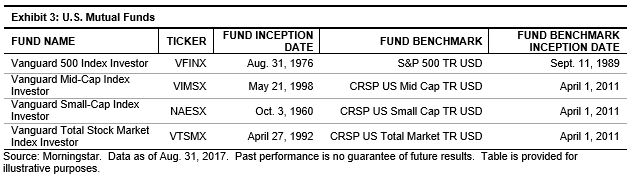

For all of the analysis, including the 70/20/10 strategy, the underlying benchmarks are not all published by the same provider. This has downstream impacts on performance that are not examined in the article. The underlying benchmarks tracked by each index fund are not obvious from the fund names, with the possible exception of the Vanguard 500 Index Investor, which tracks the S&P 500®. This is the only index fund in the list that tracks an S&P DJI index; the others track indices published by the University of Chicago’s Center for Research and Security Prices (CRSP). Combining index funds referencing benchmarks from different index providers often leads to unintended consequences. According to Morningstar, as of June 2017, 240 stocks were held in both the Vanguard 500 Index Investor and the Vanguard Mid-Cap Index Investor. These positions accounted for about 14.2% of the former fund and 78.3% of the mid-cap fund. The overlap is a result of differences in index methodology between S&P DJI and CRSP. Market participants implementing Craig Israelsen’s portfolio recommendations could potentially make unintended bets if they do not realize incompatibilities between underlying benchmarks. With respect to the 33/33/33 strategy, it bears emphasis that the overlap of stocks in the underlying benchmarks skew what looks like equal weighting on the surface.

In addition to benchmark incompatibility, the mid-cap, small-cap, and total market index funds did not track the same benchmark for the entire sample period. Prior to April 1, 2011, they tracked different indices. Exhibit 3 shows each fund’s inception date, current benchmark, and when they switched to their current benchmark.

Since all of these index funds seek to replicate the returns of their respective benchmarks (before expenses), changing benchmarks midstream affects the meaningfulness of the analysis. We don’t know how the index composition of previous benchmarks compares or aligns with composition of current benchmarks. Therefore, we should not assume any kind of relational consistency between observed historical index fund performance and unknown future performance. As a workaround, it may be more useful to do similar analysis using back-tested index returns, if they are available going as far back as 1999, rather than the Vanguard index fund returns.

There is certainly nothing wrong with using size segments to overweight or underweight parts of the stock market, but one does not get a free lunch by doing so. In order to accurately implement a view regarding size or factor tilts, it is beneficial to understand the underlying benchmark methodology and use index funds tracking benchmarks from a single index provider. When there seems to be value added without explanation, look deeper for its reasons. Outsize gains from unexplained sources could imply flawed analysis.

[1] https://www.financial-planning.com/news/three-against-one-a-battle-of-index-funds

The posts on this blog are opinions, not advice. Please read our Disclaimers.