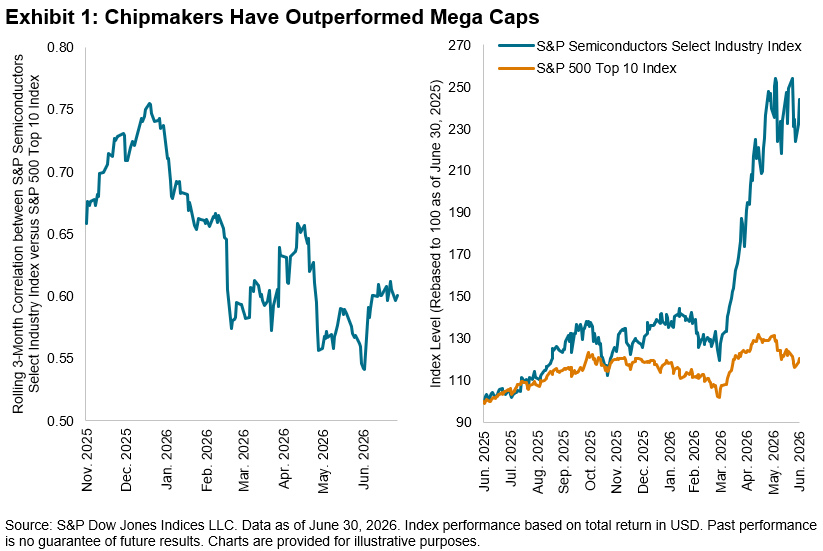

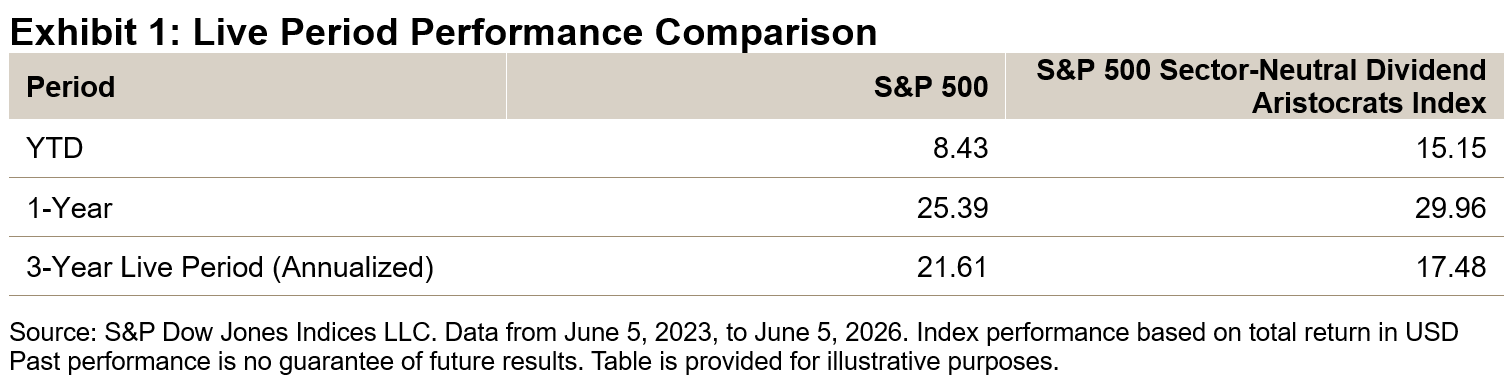

In June 2023, S&P DJI expanded the S&P Dividend Aristocrats® Series with the launch of the S&P 500® Sector-Neutral Dividend Aristocrats Index. The addition proved timely, as over the past three years, the technology-driven Information Technology and Communication Services sectors have fueled much of the S&P 500’s significant gains amid the rise of AI. While most dividend strategies have notably underperformed during this period due to their underexposure to these sectors, the sector-neutral design of the S&P 500 Sector-Neutral Dividend Aristocrats Index has clearly enabled it to keep pace with—and even outperform—the S&P 500 in recent times (see Exhibit 1).

In celebration of the index’s three-year milestone, this blog will review its short- and long-term performance, offer a quick overview of its methodology and highlight its current key attributes—such as dividend yield and valuation—which remain compelling compared to the S&P 500 today.

Performance

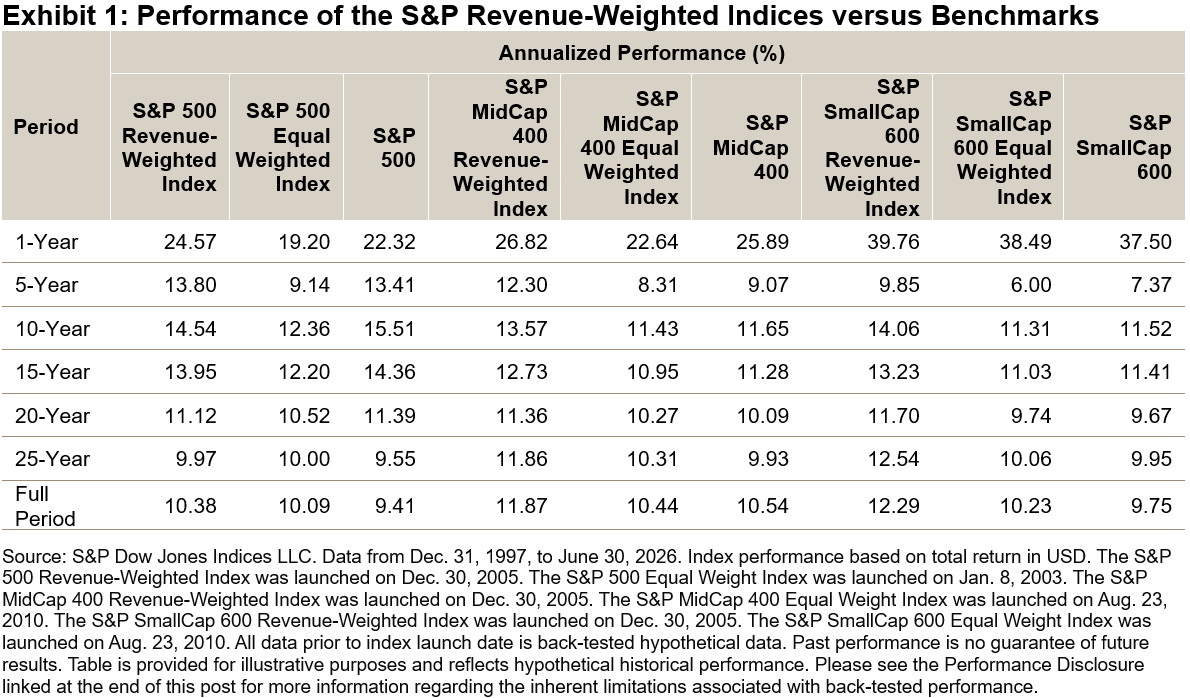

The S&P 500 Sector-Neutral Dividend Aristocrats Index has outperformed the S&P 500 on both a one-year and YTD basis, while also keeping pace with the S&P 500 over the three-year live period (see Exhibit 1). The strong recent performance is notable for a dividend-focused strategy, considering that the S&P 500’s gains have been predominantly driven by high momentum, growth-oriented technology companies capitalizing on the AI boom.

Methodology Overview

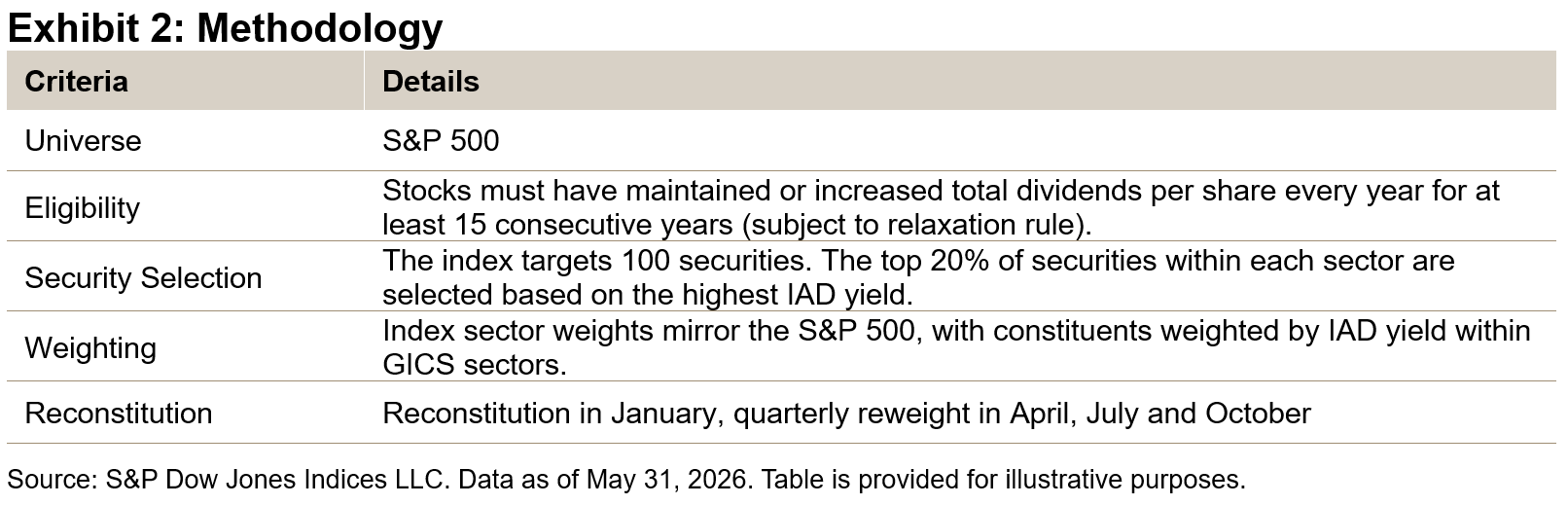

The S&P 500 Sector-Neutral Dividend Aristocrats Index starts by screening for companies that have maintained or increased dividend per share for at least 15 consecutive years, subject to a relaxation rule. From this subset, the index then selects the top 20% of companies within each GICS® sector based on the highest indicated annualized dividend (IAD) yield.

Performance Comparison

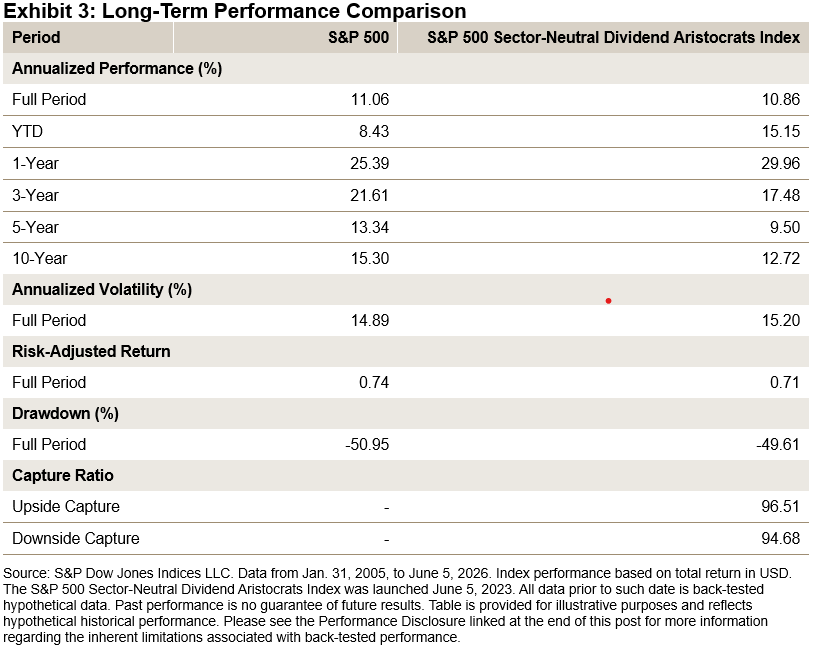

Over the back-tested period since January 2005, the S&P 500 Sector-Neutral Dividend Aristocrats Index has kept pace with the S&P 500, delivering an impressive double-digit annualized gain for more than twenty years. The index delivered this performance while also showing moderate downside protection, as evidenced by its downside capture ratio of 94.68.

Index Characteristics

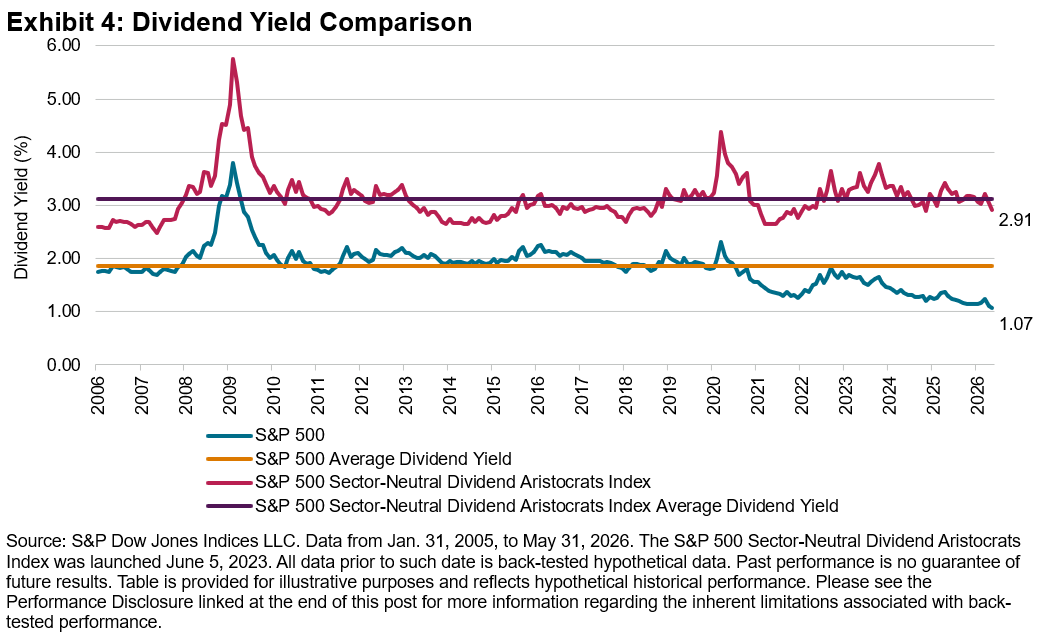

Exhibit 4 shows that as of May 31, 2026, the S&P 500 Sector-Neutral Dividend Aristocrats Index yielded 2.91%—2.7 times the S&P 500’s 1.07%, which is the lowest yield for the S&P 500 since January 2005, the beginning of the studied period. The S&P 500 Sector-Neutral Dividend Aristocrats Index has distinguished itself in today’s market environment by delivering a significantly higher yield than the S&P 500, while steering clear of large sector bets amid this period of technological transformation.

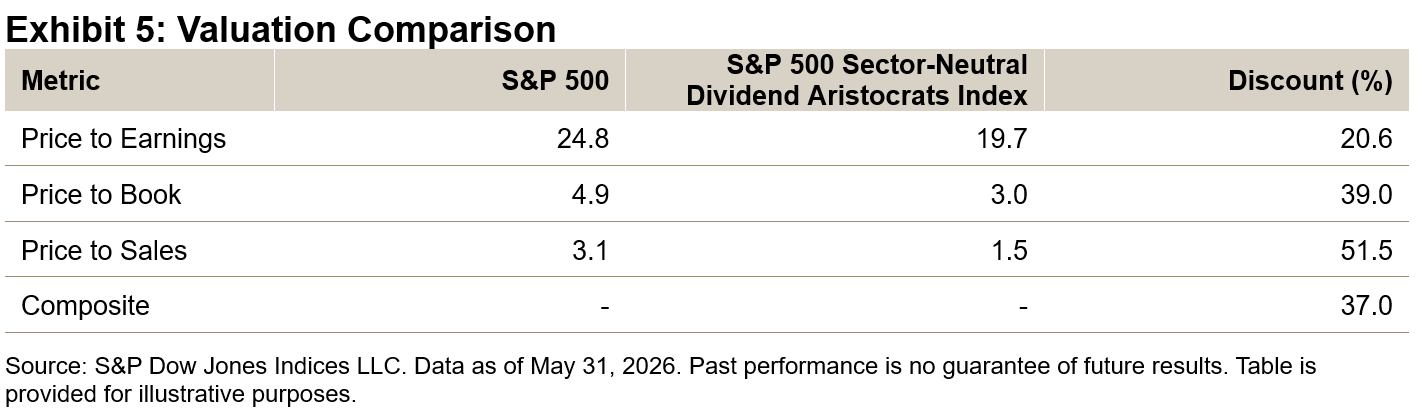

As of May 31, 2026, the S&P 500 Sector-Neutral Dividend Aristocrats Index traded at a significant discount to the S&P 500 across all three major valuation metrics (see Exhibit 5). On average, it traded at a discount of 37% compared to the S&P 500.

Conclusion

The sector-neutral design of the S&P 500 Sector-Neutral Dividend Aristocrats Index has been a significant advantage, allowing it to outperform both the S&P 500 and most other dividend strategies over 2025 and YTD. Currently, the index shows a markedly higher dividend yield than the S&P 500—while also trading at a notable discount. These characteristics are notable, given they are achieved without any sector bets relative to the S&P 500—which could be an important advantage during this distinctive period of technological change.

The posts on this blog are opinions, not advice. Please read our Disclaimers.