The S&P 500® gained 15% in Q2 2026, posting its best quarter since Q2 2020. The steady drumbeat of AI-related enthusiasm propelled the market upward despite numerous obstacles, including the war with Iran, rising inflation and fears of Fed rate hikes. However, the start of Q3 has been rocky, with a sharp sell-off in chipmakers, followed by a bounce back today, as investors struggle to assess the sustainability of the AI trade. Are these market oscillations ephemeral in nature or a sign of a regime shift?

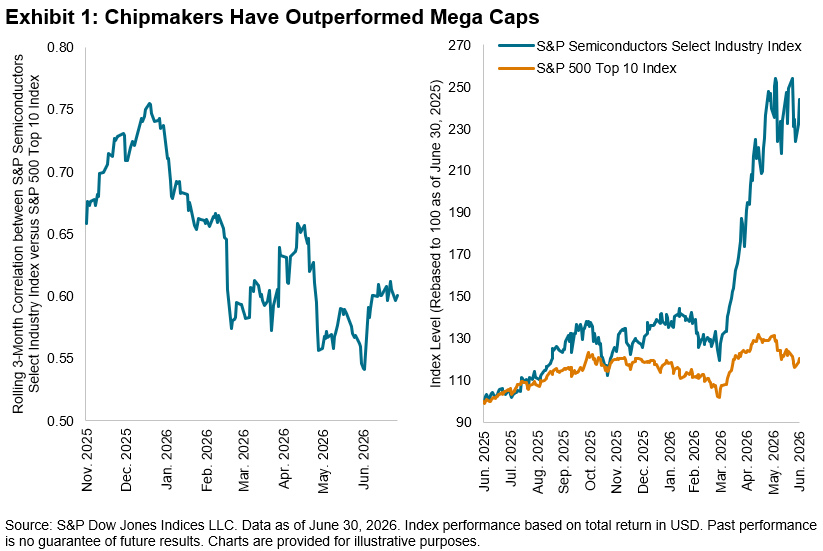

Reflecting on the past year, the recipients of the rewards of investment in AI infrastructure have no longer been confined to the mega-cap adopters, but they are also moving toward rapidly growing memory chip suppliers housed in the semiconductors industry.1 These leaders include Sandisk Corporation, Micron Technology and stalwart Intel, which were the three top-performing stocks in The 500® YTD through June 30.

Naturally, the performance of mega caps versus chipmakers has diverged over the past year, with the S&P Semiconductors Select Industry Index’s gain of 144% trouncing the 20% gain for the S&P 500 Top 10 Index.2 Exhibit 1 shows that three-month performance correlations between the two indices fell steadily over the one-year period.

In a reversal from recent years characterized by large-cap strength, one of the consequences of the shifting performance among participants across the AI value chain has been the broadening of the rally toward smaller caps, with the S&P MidCap 400® and S&P SmallCap 600® up 14% and 20%, respectively, in Q2.

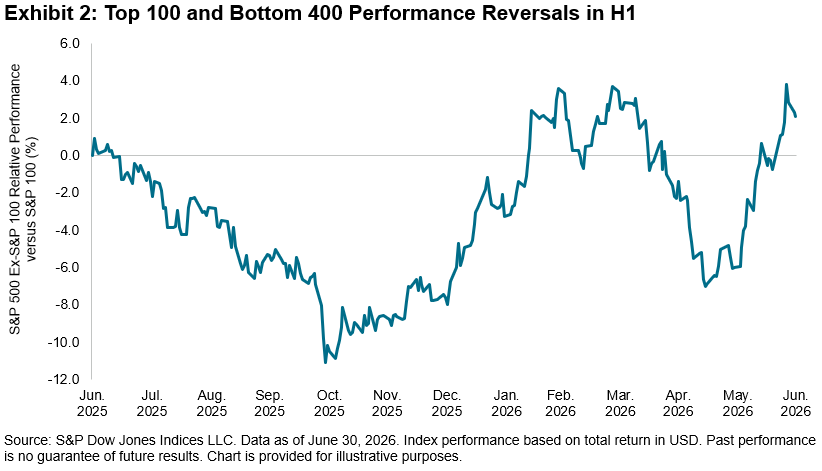

The rally expanded within large caps alone, with the S&P 500 Ex-S&P 100 Index, which not coincidentally includes Sandisk and other leading semiconductor companies like Western Digital, outperforming the S&P 100 by 2% YTD. But the path to outperformance was not linear, as illustrated in Exhibit 2, with the bottom 400 outperforming in Q1, followed by sharp underperformance as mega caps returned to favor and resuming outperformance in June as investors sought refuge among smaller, domestically oriented and defensive stocks.

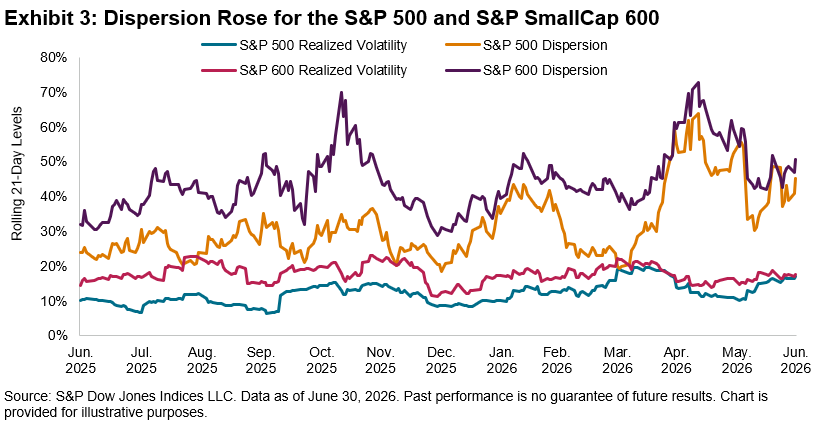

Despite these fluctuations, Exhibit 3 shows that index volatility has remained moderate, with a realized volatility of 17% for both the S&P 500 and S&P 600® for June 2026.3 Meanwhile, cross-sectional volatility—or dispersion, which measures how differently stocks are performing relative to each other—has risen to extreme levels. S&P 600 21-day dispersion reached a peak of 60% in April 2026, outpacing the prior high from November 2025 and the 55% level observed for the S&P 500.

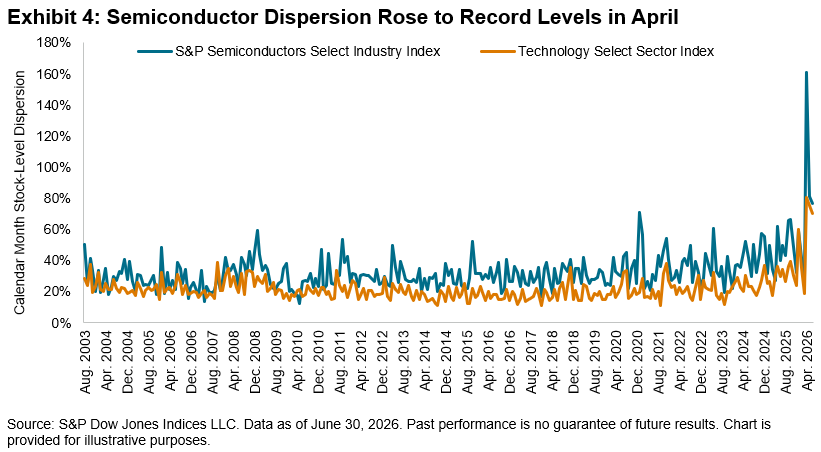

Offering a more granular view is Exhibit 4, which shows that the Technology Select Sector index’s calendar-month stock-level dispersion rose to 80% in April 2026. This level doubled to 161% for the S&P Semiconductors Select Industry Index. The lackluster reaction to Broadcom’s earnings beat and guidance, enthusiastic response to Micron’s blockbuster results, and most recently, the plunge in Samsung’s stock in spite of its earnings beat are prime examples of the increased scrutiny faced by these firms. The value of stock-selection skill rises when dispersion is high, which can mean fruitful conditions for skillful stock pickers to outperform.

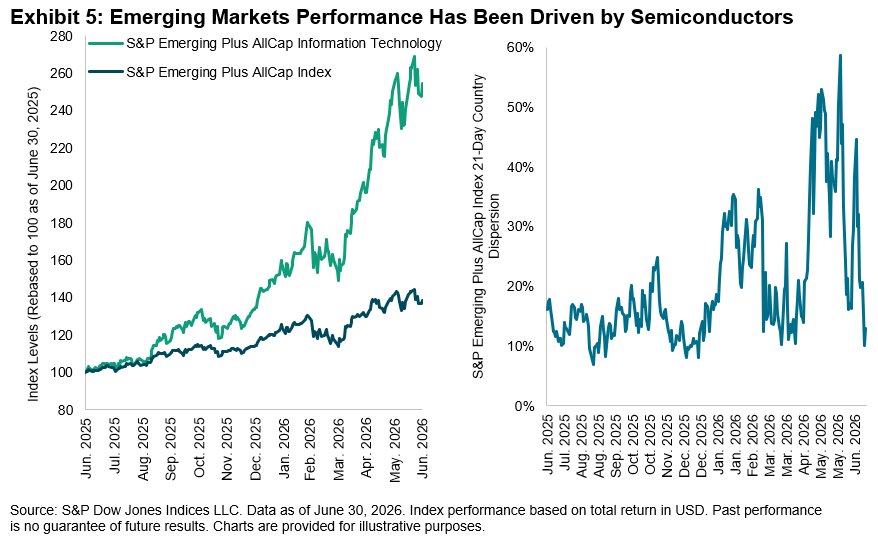

The impact of the AI boom has reverberated globally, most notably in emerging markets. We observe in Exhibit 5 that the S&P Emerging Plus AllCap Information Technology outperformed the S&P Emerging Plus AllCap Index4 by 116% since June 2025.

But the rewards have not been distributed equally across regions. Dispersion, which can also be measured at the country level, widened for the S&P Emerging Plus Index to a high of 58% in early June 2026. Countries with greater sensitivity to semiconductors like South Korea and Taiwan outperformed, although not without their share of jitters, just as we have witnessed in the U.S.

No one knows if the performance gyrations in semiconductors are a temporary blip or the sign of a new regime, but understanding the drivers of these reversals in performance and risk from a size, sector, industry and global lens may provide a nuanced perspective for market participants as they navigate H2.

1 See Ganti, Anu, “Cashing in the Chips?, S&P Dow Jones Indices LLC, June 2, 2026.

2 Performance from June 30, 2025, to June 30, 2026.

3 See Dispersion, Volatility & Correlation Dashboard, S&P Dow Jones Indices LLC, June 30, 2026.

4 Includes securities in emerging markets, plus South Korea.

The posts on this blog are opinions, not advice. Please read our Disclaimers.