As readers of our SPIVA® Scorecards know, beating the market is difficult. Finding those few managers capable of doing so consistently may be even harder. Of the 933 active equity funds domiciled in Japan, more than 80% underperformed their respective benchmarks in 2025.1 Yet even among the minority that did outperform, the bigger question remains: how many were able to repeat that success?

If an active manager possesses genuine skill, one would expect their funds to outperform with some consistency over time. However, our research shows that active outperformance tends to be fleeting, regardless of asset class or geography.

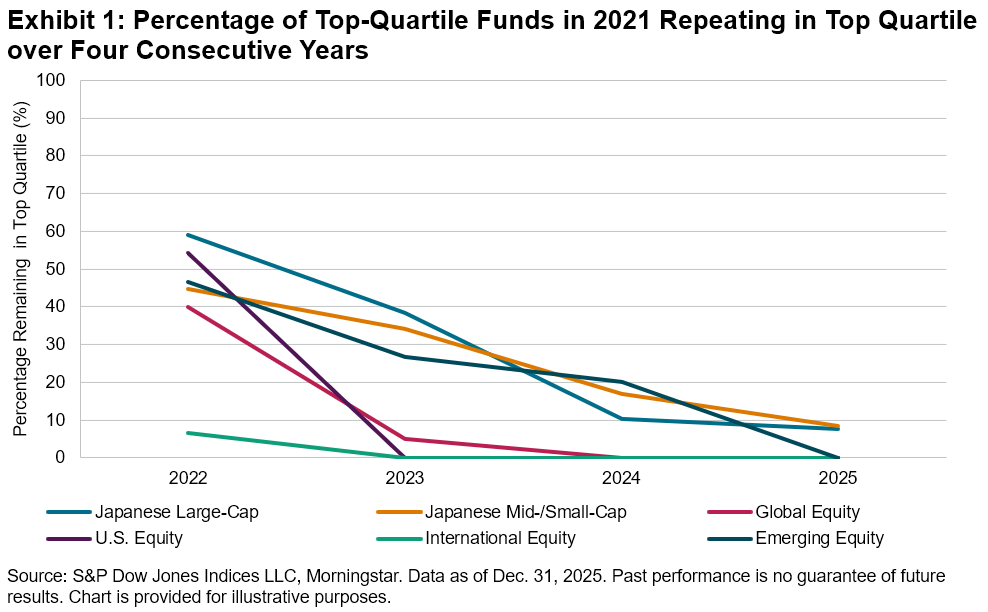

Japan was no exception. Based on the universe of funds covered in the SPIVA Japan Scorecard, most of the funds that ranked among the best performers in one period failed to maintain that position in the years that followed. Of the 78 Japanese Large-Cap and 47 Japanese Mid-/Small-Cap funds that placed in the top quartile in 2021, only 8% (including 6 Japanese Large-Cap and 4 Japanese Mid-/Small-Cap funds) remained in the top quartile in each of the four subsequent years. Across the non-domestic equity fund categories examined, not a single fund managed to rank in the top quartile for five consecutive years (see Exhibit 1).

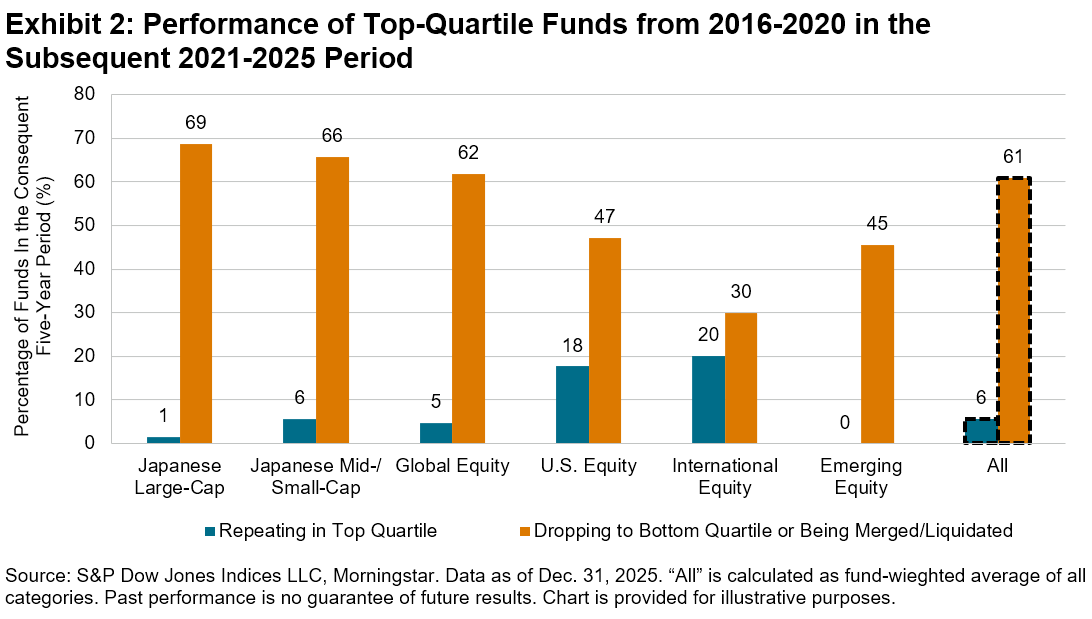

The picture became even starker over longer time horizons. As shown in Exhibit 2, among the top-quartile funds across all reported Japanese fund categories for the five-year period ending in December 2020, only 6% maintained their top-quartile status over the subsequent five-year period, while 61% fell to the bottom quartile or were merged or liquidated.

These shifts were particularly pronounced in domestic equity funds. Only 1% of the top-quartile Japanese Large-Cap funds in 2016-2020 remained in the top quartile in 2021-2025, while 69% dropped to the bottom quartile or were merged or liquidated.

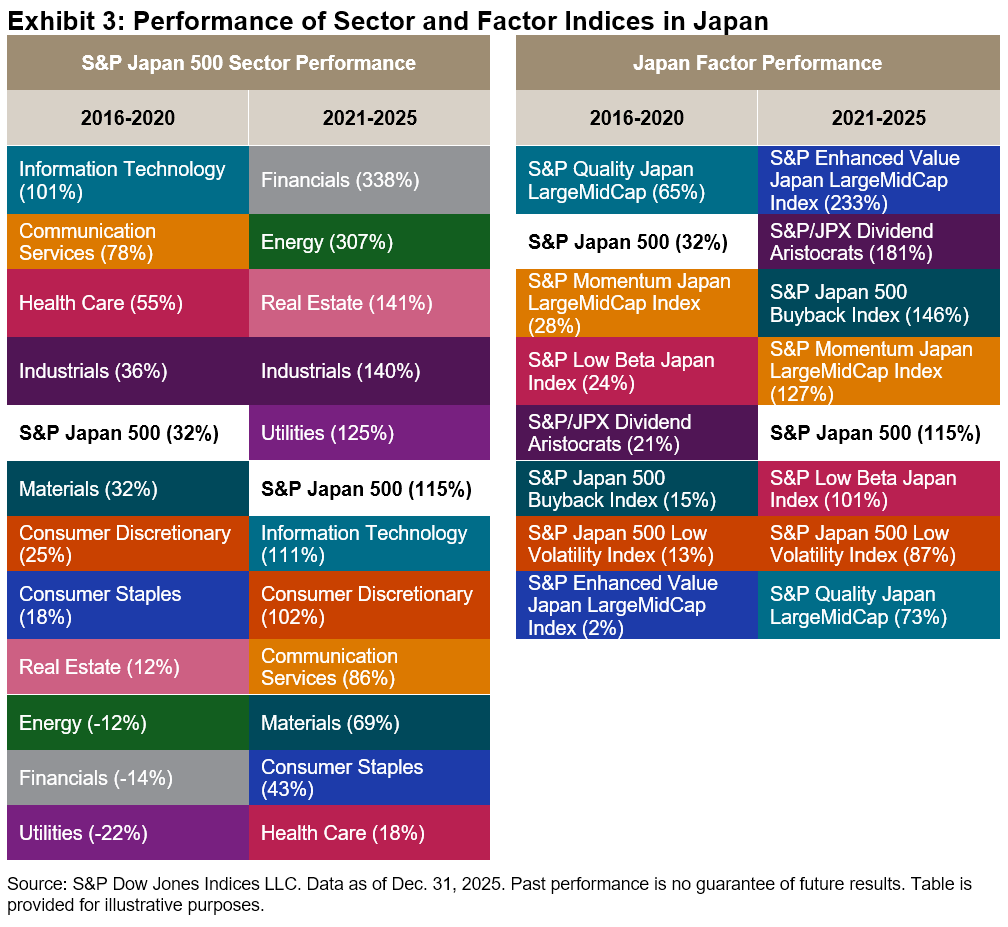

Examining market trends over these two five-year periods may provide some insights into the sharp turnover in fund rankings. Comparing the performance of Japanese sector and factor indices2 between the two five-year periods (see Exhibit 3) reveals meaningful rotations in leadership. For example, the top-performing sectors in 2016-2020—Information Technology, Communication Services and Health Care—all lagged in 2021-2025, while Financials and Energy, which were among the worst-performing sectors in 2016-2020, posted strong outperformance in the subsequent five-year period.

A similar reversal was evident at the factor level. Quality moved from the top of the table in 2016-2020 to the bottom in 2021-2025, while Value, Dividend and Buyback moved in the opposite direction, leading the market in the most recent five years (see Exhibit 3). Taken together, the lack of persistence among active funds and the sharp rotation in market drivers suggest that many active domestic equity managers struggled to adapt to the changing conditions in the Japanese equity market.

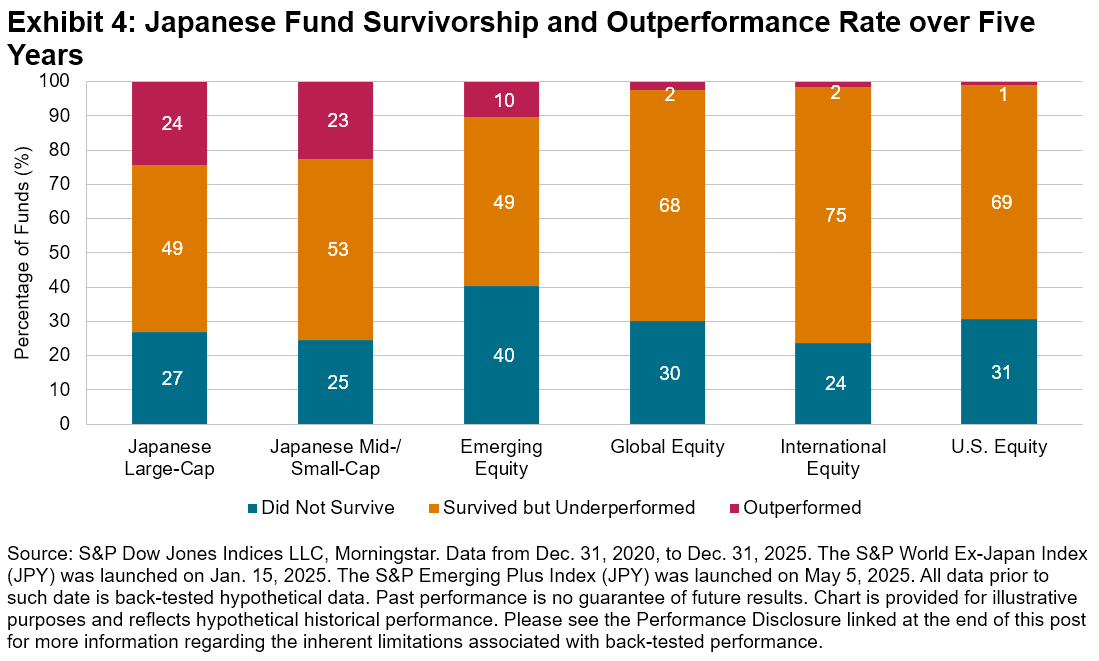

Over the recent five-year period, a firm majority of actively managed equity funds in Japan underperformed across all reported categories (see Exhibit 4). While domestic equity funds fared relatively better, with roughly one in four funds outperforming, identifying these outperformers in advance would likely have been difficult, particularly for fund selectors relying on historical fund performance as a guide.

1 Lee, Sue et al., “SPIVA Japan Scorecard Year-End 2025,” S&P Dow Jones Indices LLC, March 9, 2026.

2 See the Index Dashboard: Japan for the list of sector and factor indices in Japan.

The posts on this blog are opinions, not advice. Please read our Disclaimers.