Single-factor indices have historically outperformed over the long term, but their performance tends to be cyclical, varying with macroeconomic conditions. This has driven demand for multi-factor indices, which combine factors such as quality, value and momentum to leverage their low correlations. By diversifying across multiple factors, these indices seek to enhance long-term risk-adjusted performance and provide more stability.

In this blog, we introduce the S&P 500® Quality, Value & Momentum Multi-Factor Index and explore its construction, review its historical performance, analyze sector composition and assess its factor weights to provide a comprehensive overview of its characteristics.

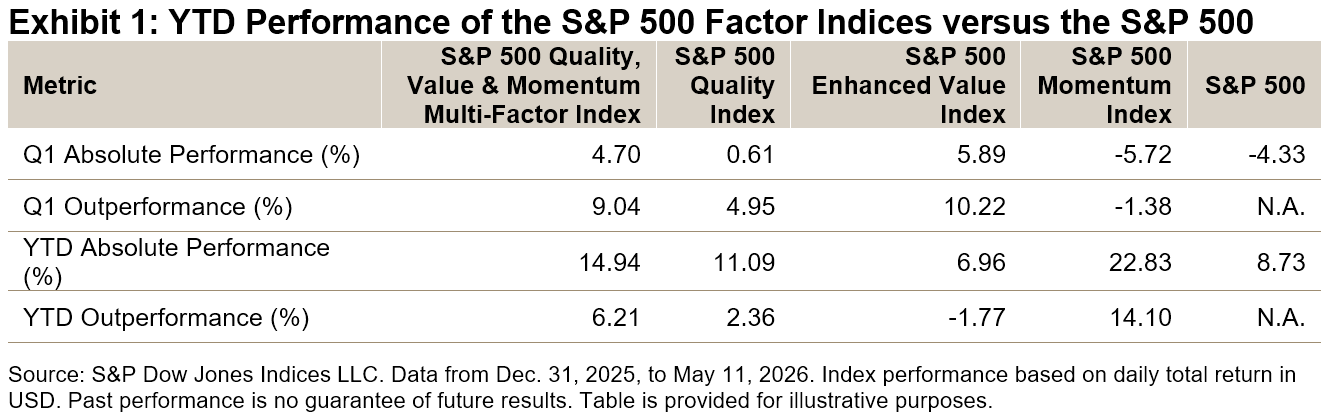

YTD Outperformance

The S&P 500 Quality, Value & Momentum Multi-Factor Index outperformed the S&P 500 in Q1 and YTD 2026 (see Exhibit 1). Despite increased volatility in Q1, it proved resilient, outperforming the S&P 500 by about 9%. As markets rebounded from March lows, the multi-factor strategy maintained its outperformance, while indices like the S&P 500 Enhanced Value Index lagged.

Methodology Overview

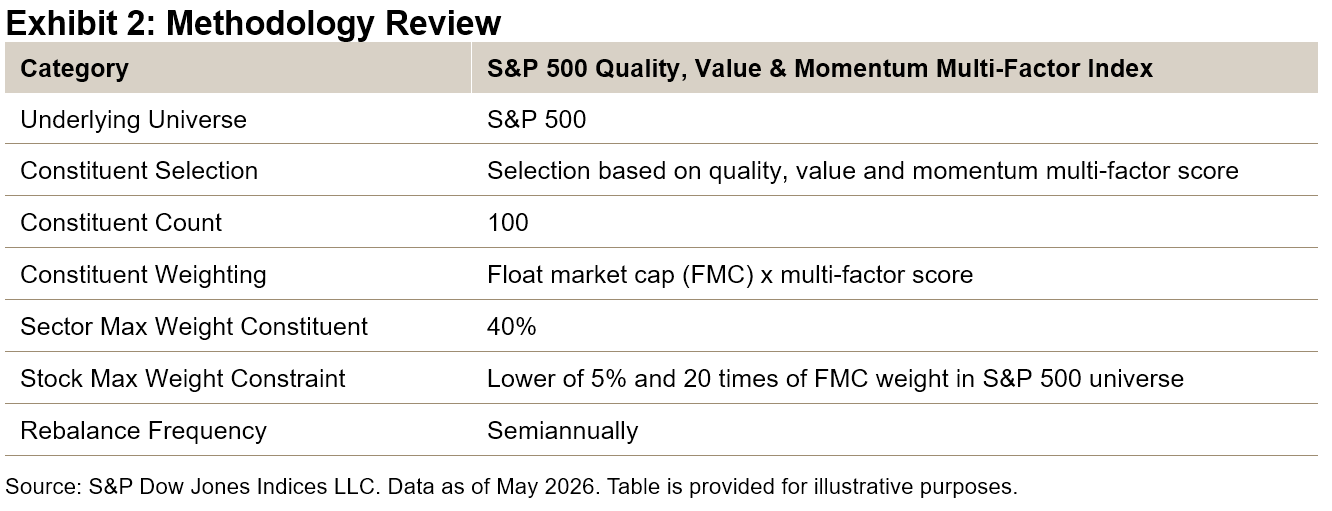

The S&P 500 Quality, Value & Momentum Multi-Factor Index uses a bottom-up approach, selecting the top 20% of S&P 500 stocks based on a composite multi-factor score1 (see Exhibit 2). This score averages individual quality, value and momentum scores, targeting a concentrated group of “all-rounders”—stocks that exhibit strength across multiple factors.

Constituents are weighted by the product of their market capitalization and multi-factor score, balancing size and factor strength.2 The index is rebalanced semiannually in June and December to maintain its targeted multi-factor scores and adapt to changing market conditions.

Harnessing Complementary Factors

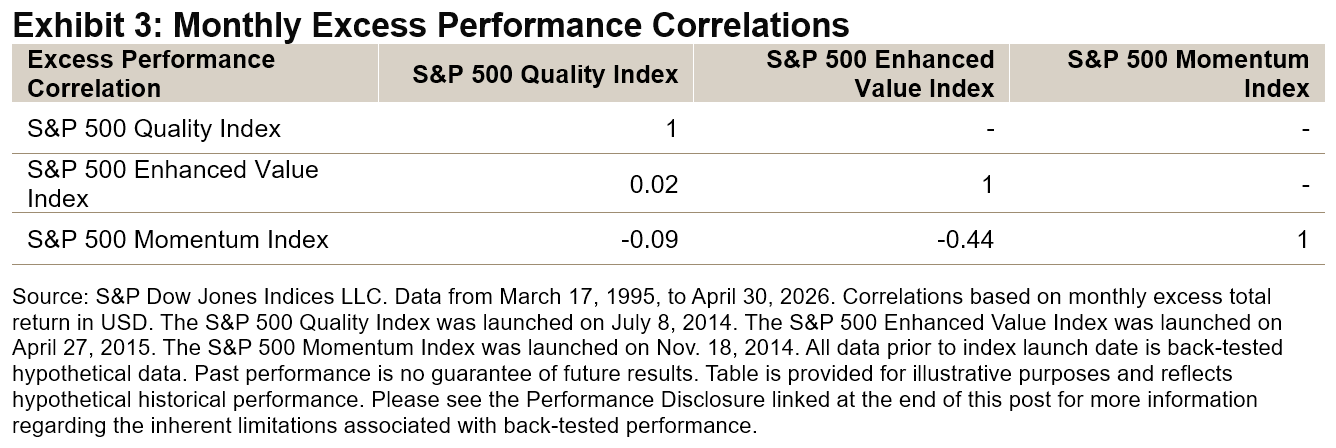

Factor combinations are generally grounded in economic rationale. Quality, value and momentum have historically tended to respond complementarily across different phases of the business cycle: quality is defensive and tends to outperform during economic slowdowns; value is procyclical, performing well during recoveries; and momentum benefits from persistent market trends. As shown in Exhibit 3, the excess performance of the S&P 500 Quality Index, S&P 500 Enhanced Value Index and S&P 500 Momentum Index exhibited low or even negative correlations, underscoring their diversification potential.

Performance Comparison

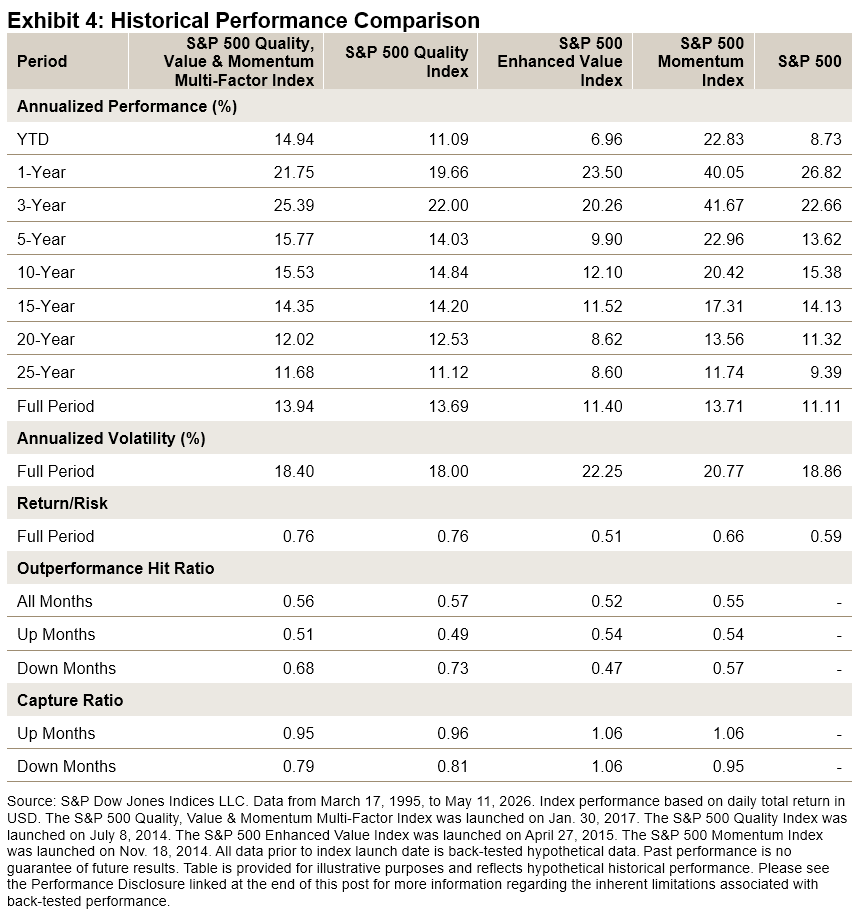

The S&P 500 Quality, Value & Momentum Multi-Factor Index consistently outperformed the benchmark over both short and longer back-tested horizons, in total and risk-adjusted performance. It also exhibited greater resilience than single-factor strategies, as evidenced by the performance hit ratio and capture ratios (see Exhibit 4), highlighting the historical advantage of combining complementary factors to reduce cyclicality.

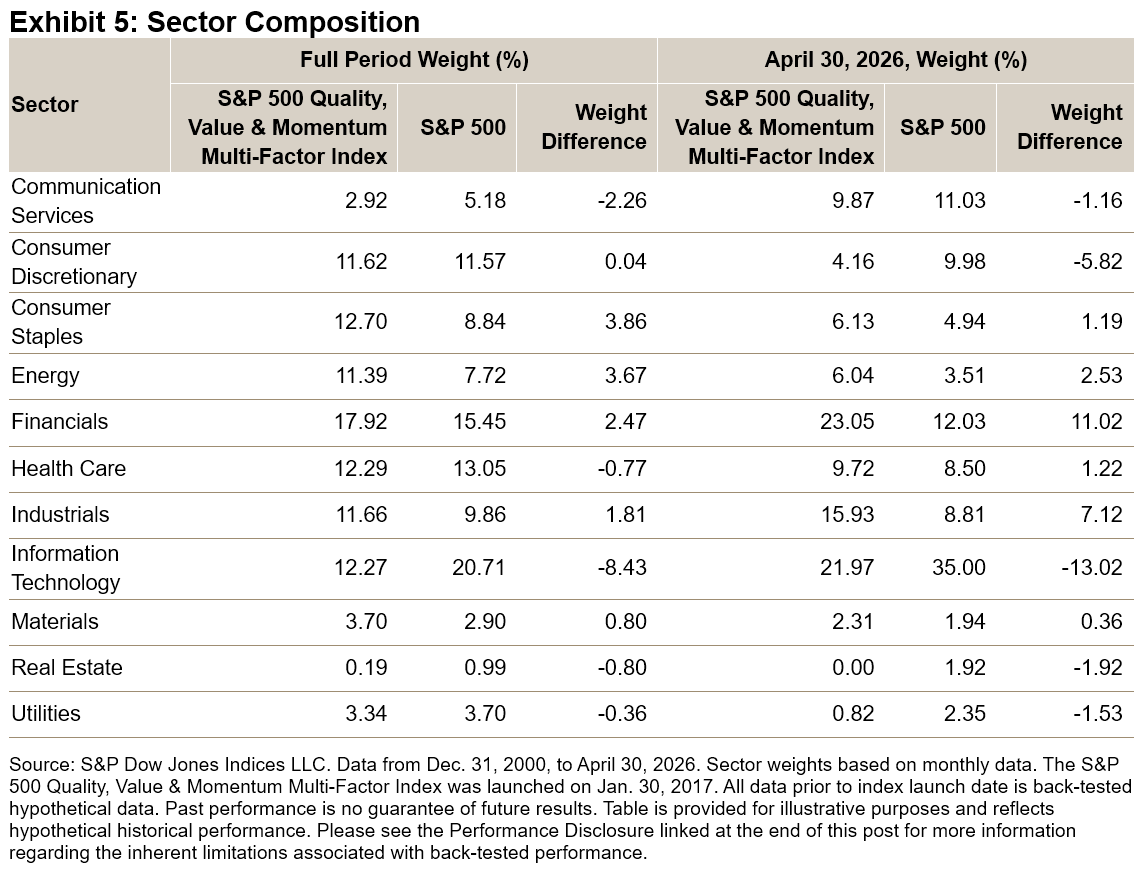

Sector Composition

Exhibit 5 shows the sector weights of the S&P 500 Quality, Value & Momentum Multi-Factor Index versus the S&P 500. The S&P 500 Quality, Value & Momentum Multi-Factor Index has historically overweighted Consumer Staples, Energy, Financials and Industrials, while underweighting Information Technology and Communication Services. This sector tilt contributes to the index’s distinct risk and performance profile compared to the S&P 500.

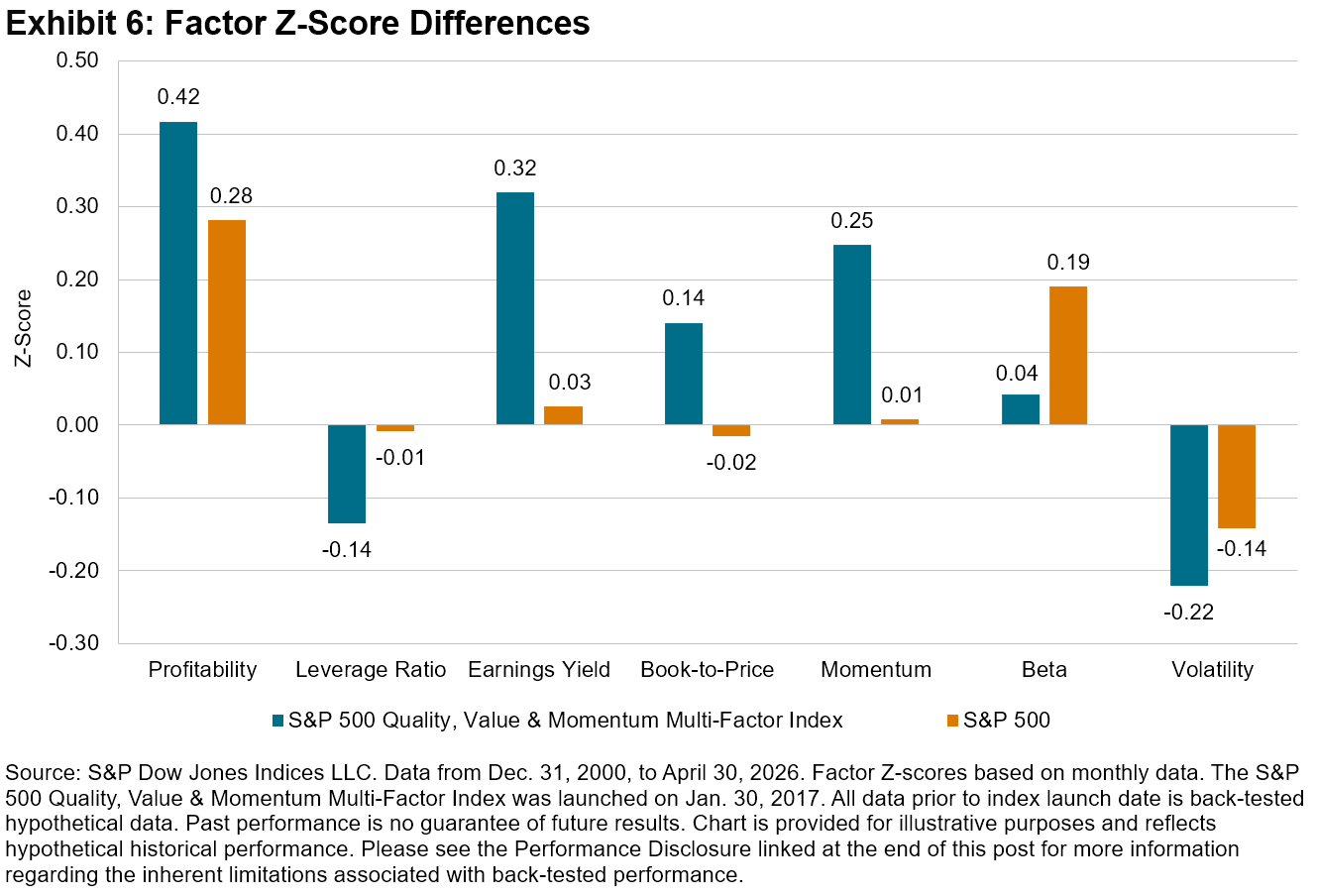

Factor Z-Scores

Exhibit 6 highlights the factor Z-score differences between the S&P 500 Quality, Value & Momentum Multi-Factor Index and the S&P 500, using FactSet Risk Model Z-scores. As expected, the S&P 500 Quality, Value & Momentum Multi-Factor Index had higher Z-scores in quality (higher profitability and lower leverage), value (earnings yield and the book-to-price ratio) and momentum. It also shows spill-over into lower beta and lower volatility.

Conclusion

The S&P 500 Quality, Value & Momentum Multi-Factor Index showcases a diversified approach that can help with navigating varying market conditions. By blending complementary factors, the index aims to enhance risk-adjusted performance and reduce cyclicality, providing an alternative to traditional single-factor or market-cap-weighted strategies.

1 Andrew Innes, “The Merits and Methods of Multi-Factor Investing,” S&P Dow Jones Indices LLC, April 2018.

2 For more detailed information, please refer to the S&P 500 Quality, Value & Momentum Multi-Factor Indices Methodology.

The posts on this blog are opinions, not advice. Please read our Disclaimers.