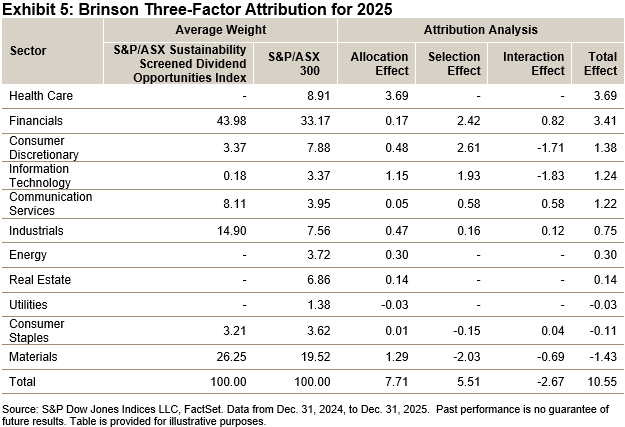

Since the beginning of 2025, the global Financials sector has experienced a significant shift. For several years, across the developed world, the sector had been sailing in roughly the same direction, though generally the U.S. at a higher rate of knots. In 2025, market winds blew the S&P 500 Financials (Sector) and the S&P World Ex-U.S. Financials (Sector) Index in significantly different directions. This piece unpacks the drivers of this divergence.

Exhibits 1 and 2 highlight the recent change. Exhibit 1 shows annual index performance since 2010. In 11 of the 15 years prior to 2025, the U.S. Financials sector outperformed the ex-U.S. sector, and on occasions where the latter outperformed it was never by more than 12%. However, in 2025, the S&P World Ex-U.S. Financials Index outperformed by nearly 25%, and so far in 2026, it is over 7% ahead.

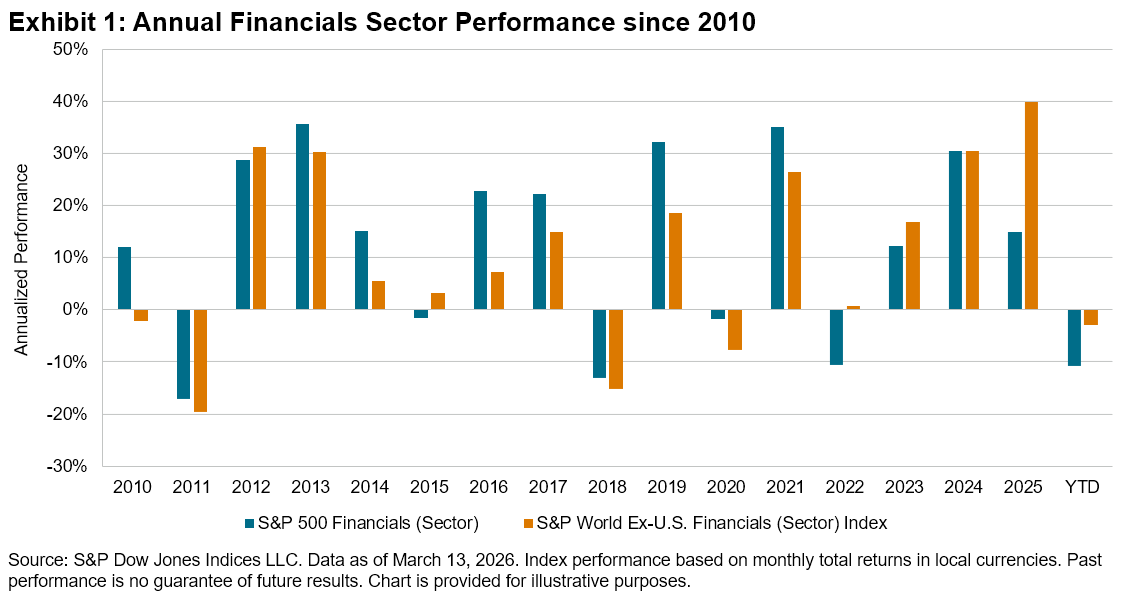

Correlations between the sectors have fallen recently, as shown in Exhibit 2.

Fluctuations are normal and correlations have been lower since 2010, but this, combined with the recent performance, demonstrates a clear change, which begs the question—why? Observing fundamental performance and index composition begins to provide an answer.

Exhibit 3 shows changes in both earnings and P/E since the start of 2025. Both indices saw solid earnings growth, especially the S&P World Ex-U.S. Financials Index at 23% compared to 9% for the S&P 500 Financials. The far larger differentiator, however, was that ex-U.S. P/E multiples saw large expansion, while in the U.S. they contracted slightly.

The performance divergence coincided with the U.S. tariff announcements in mid-February 2025, making them possible contributors to this sentiment shift. However, a more favorable monetary environment and increasing profitability may have also been drivers. Clearly though, market sentiment toward the ex-U.S. Financials sector has shifted significantly, resulting in a rerating relative to their U.S. peers since early 2025.

Despite this, the S&P World Ex-U.S. Financials Index is still a long way from parity with the S&P 500 Financials. Currently, P/E levels are around 14.3 for the S&P World Ex-U.S. Financials Index compared to 17.3 for the S&P 500 Financials.

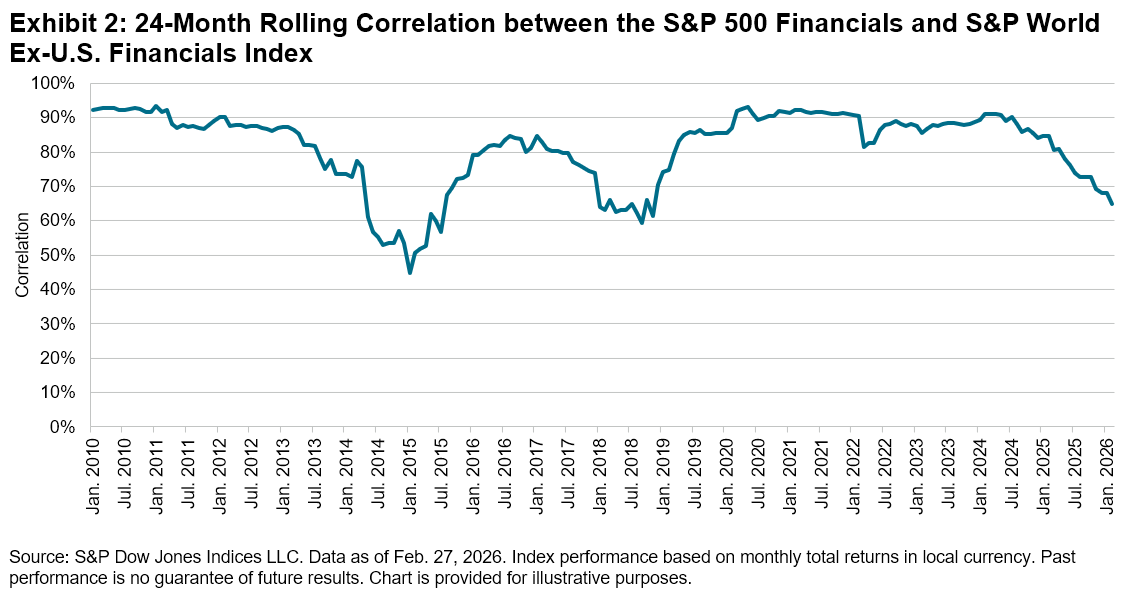

These indices reflect more than just different macro measurements of the same sector. Owing to the differences in the makeup of the Financials sector globally, they have distinct GICS industry weights, as demonstrated in Exhibit 4.

Within the S&P 500 Financials, the sector is diversified across industries, with significant weights in the Capital Markets, Financial Services and Banks industries, spanning a range of companies from investment banks to cryptocurrency exchanges. In contrast, the S&P World Ex-U.S. Financials Index is dominated by the Banks industry.

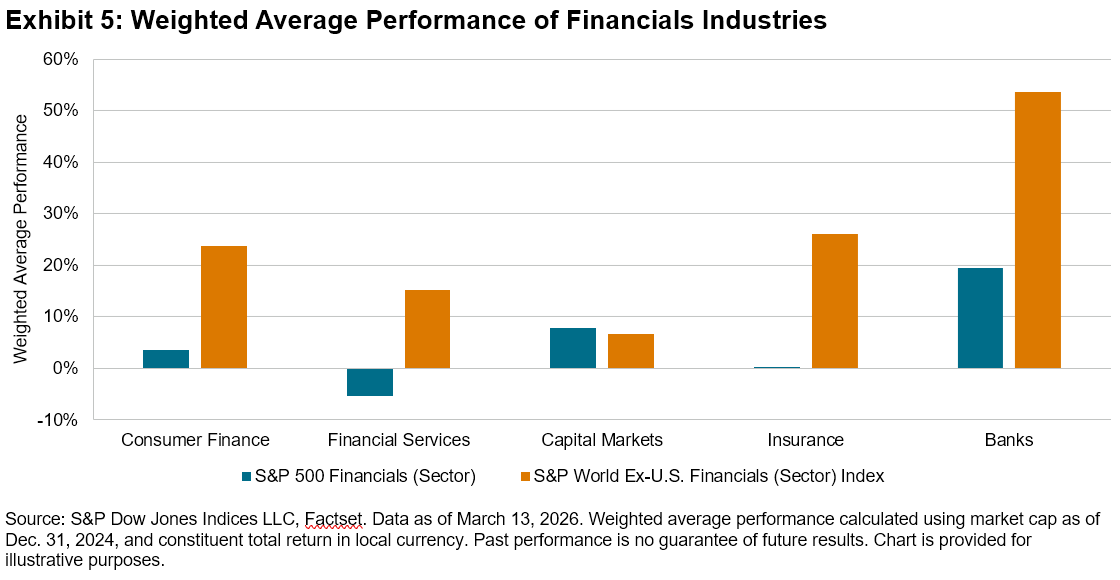

Differences in industry weights give each index distinct sensitivities to market trends, causing potential performance differences. Exhibit 5 shows that, since early 2025, Banks have been the top-performing industry in both regions, benefitting the S&P World Ex-U.S. Financials Index. Additionally, four out of five S&P World Ex-U.S. Financials Index industries outperformed their S&P 500 Financials equivalents, demonstrating the impact of sentiment changes.

Whether 2025 was an anomaly or the beginning of a new regime for Financials remains uncertain. Sustained outperformance of the Banks industry or a lasting shift in sentiment due to geopolitical events could benefit the S&P World Ex-U.S. Financials Index. Conversely, performance may revert to the historical dominance of the S&P 500 Financials. In this uncertain landscape, sector indices provide a valuable perspective on how these dynamics unfold.

The posts on this blog are opinions, not advice. Please read our Disclaimers.