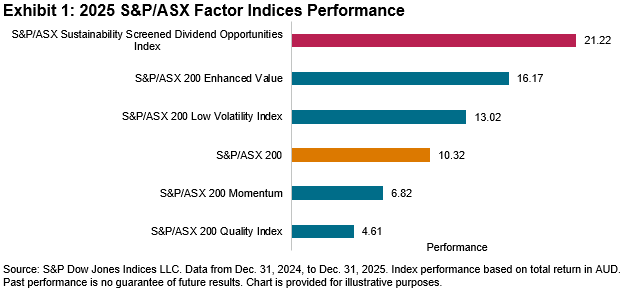

The S&P/ASX Sustainability Screened Dividend Opportunities Index delivered a standout performance in 2025, establishing itself as the best performer among all the S&P Factor Indices in the Australian equity landscape. The index posted a robust calendar year return of 21.22%, outpacing the S&P/ASX 300 by 10.9% (see Exhibit 1).

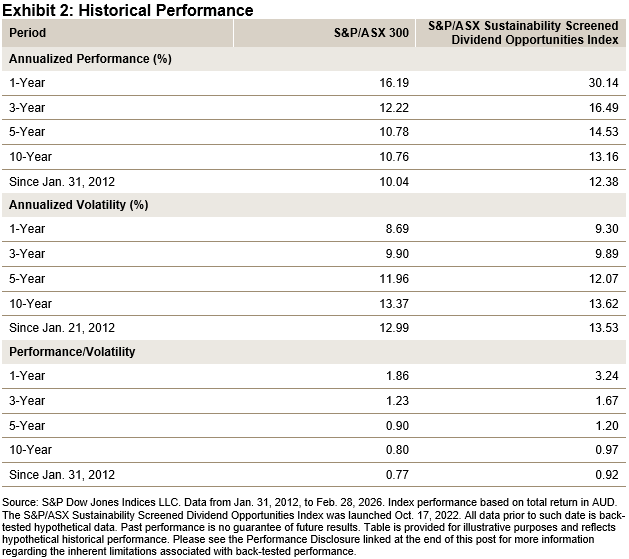

In addition to its recent outperformance, the S&P/ASX Sustainability Screened Dividend Opportunities Index consistently outperformed the S&P/ASX 300 over the mid and long term as well. As Exhibit 2 shows, it outperformed the S&P/ASX 300 over the 1-, 3-, 5- and 10-year periods, and over the full 14-year back-tested history since Jan. 31, 2012. Since its launch on Oct. 17, 2022, the index has achieved an excess annual return of 4.43% compared to the S&P/ASX 300.

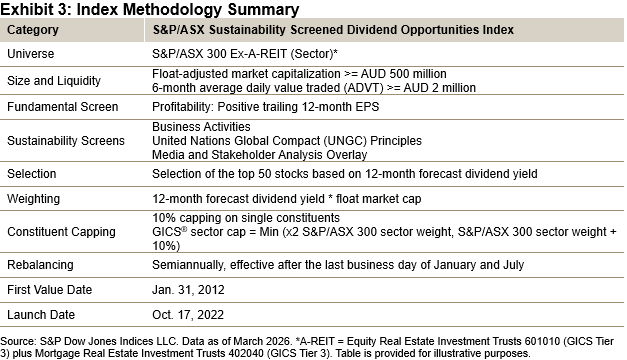

Index Construction

The construction of the S&P/ASX Sustainability Screened Dividend Opportunities Index is underpinned by a transparent, rules-based approach that reflects both income and sustainability considerations (see Exhibit 3).1 The process begins by considering all stocks in the S&P/ASX 300 universe, excluding REITs. First, all stocks go through eligibility screens that include market size, liquidity and earnings-per-share (EPS) filters to avoid illiquid and unprofitable stocks. Second, the eligible stocks go through a series of sustainability screens to exclude companies involved in traditional energy, including oil & gas and thermal coal, and controversial businesses such as gambling, alcohol, tobacco, etc. After the eligibility and sustainability screens, the 50 stocks with the highest 12-month forecast dividend yield will be selected as index constituents. Constituents are weighted by the product of float-adjusted market cap and dividend yield, subject to single-stock and sector caps.

Sector Characteristics

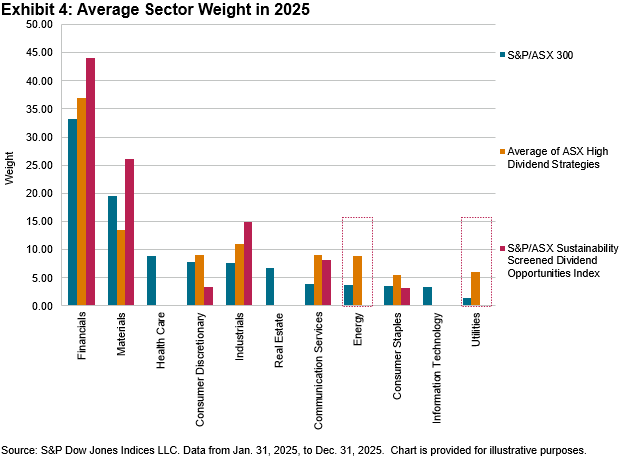

A closer look at the sector composition of the S&P/ASX Sustainability Screened Dividend Opportunities Index reveals both commonalities with and distinctions from other high dividend strategies. Exhibit 4 compares the index’s sector weights with those of the S&P/ASX 300 and with the average of two other S&P/ASX indices that focus on high dividend yield.2

Like many dividend-focused indices, the S&P/ASX Sustainability Screened Dividend Opportunities Index tends to overweight Financials, Materials and Industrials—sectors that have historically provided robust dividend streams and stable earnings. Conversely, it is underweight in Health Care and Information Technology relative to the S&P/ASX 300.

While high dividend strategies often have significant allocations to Energy and Utilities—sectors known for high dividend payouts—the S&P/ASX Sustainability Screened Dividend Opportunities Index had no weight in these sectors in 2025. This exclusion is a direct result of the sustainability criteria.

Performance Attribution

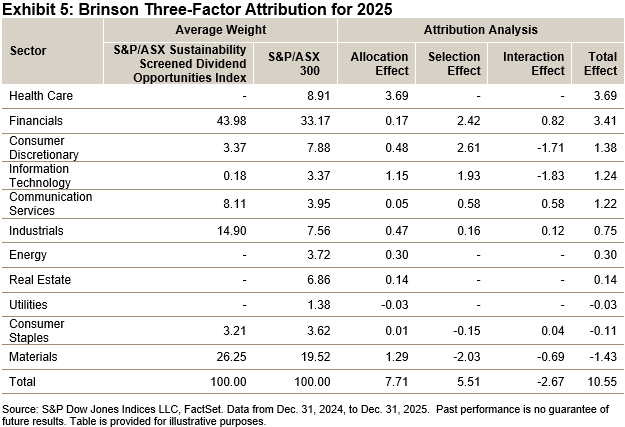

The index’s outperformance in 2025 was driven by a combination of allocation and stock selection effects. Exhibit 5 shows the sector attribution analysis of the S&P/ASX Sustainability Screened Dividend Opportunities Index against the S&P/ASX 300.

One of the most significant contributors was the index’s underweight position in Health Care and Information Technology. Facing considerable headwinds in the Australian market during 2025, Health Care and Information Technology were two sectors within the S&P/ASX 300 that posted negative performance for the year. Given that the sectors collectively accounted for around 12% of the S&P/ASX 300’s average sector weight, the near-zero exposure in the S&P/ASX Sustainability Screened Dividend Opportunities Index helped to boost its performance in 2025. In addition to sector differences, stock selection within Financials and Consumer Discretionary also played a crucial role.

The S&P/ASX Sustainability Screened Dividend Opportunities Index has historically demonstrated that incorporating sustainability screens could lead to distinctive characteristics compared to pure high dividend yield indices, which may contribute to the index performance. The S&P/ASX Sustainability Screened Dividend Opportunities Index is a unique benchmark for tracking high dividend yield stocks in the ASX market while incorporating sustainability considerations.

1 For more detailed information, please see the index methodology.

2 The S&P/ASX Dividend Opportunities Index and S&P/ASX 200 High Dividend Index

The posts on this blog are opinions, not advice. Please read our Disclaimers.