From a U.S. equities perspective, the first month of 2026 started on a different trajectory compared to years past. S&P 500® performance trailed much of the rest of the world (as measured by the S&P World Ex-U.S. Index), and within the U.S., the performance of the S&P 500 Information Technology (“U.S. Tech”) ranked in the bottom half among all 11 GICS® sectors. Fears of trade tensions tied to geopolitics, rising worries of an AI bubble and tepid economic datapoints dragged on overall market performance, with The 500® falling for much of the month before finishing up 1.5%, while U.S. Tech fell 1.7%.

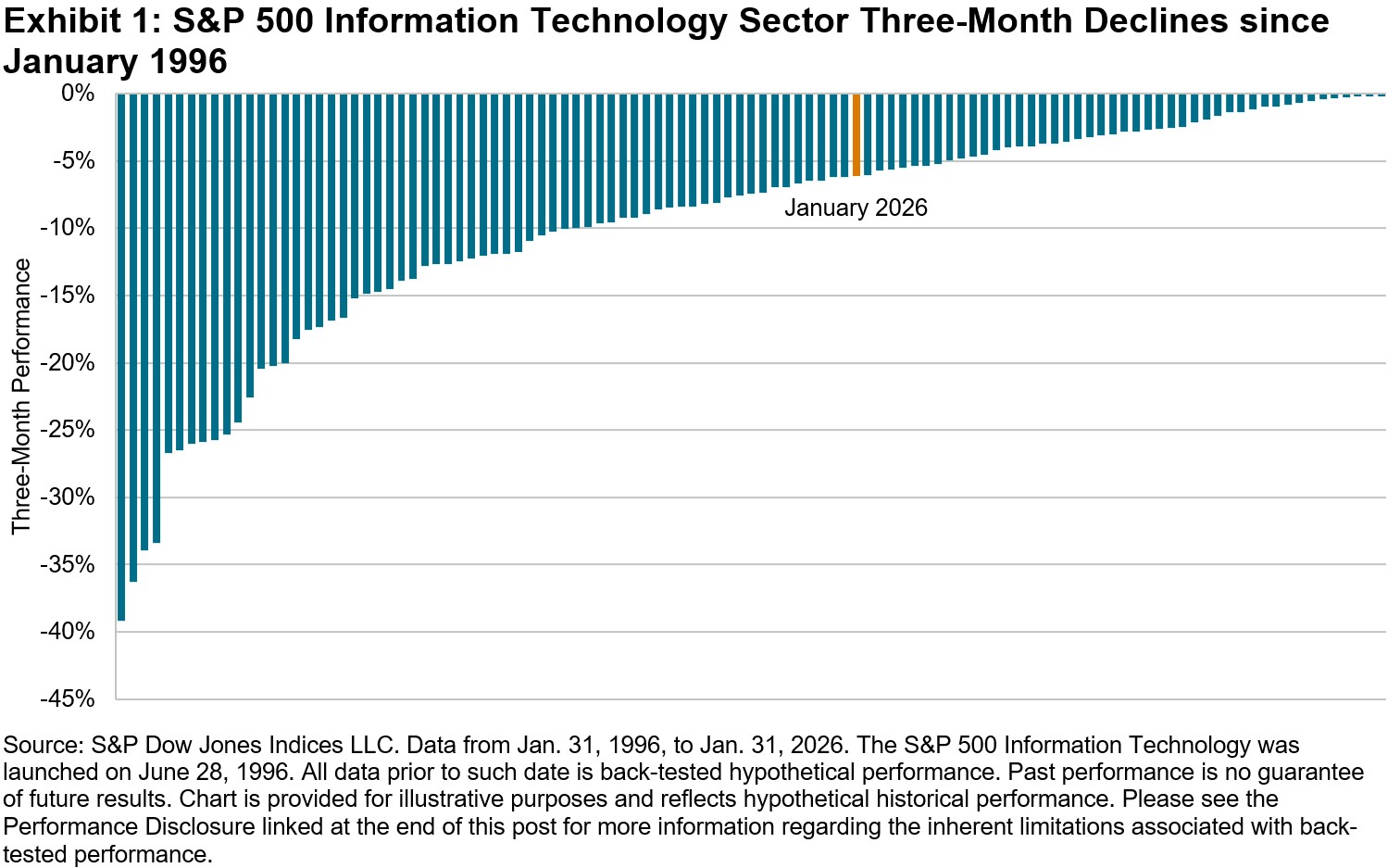

It was just over three months prior that U.S. Tech had reached an all-time high in October 2025, before sliding down 6.1% over the three months ending in January. U.S. Tech’s latest decline is noteworthy, but certainly not unprecedented, as the sector produced negative three-month performance 109 times over the last 30 years, with more than half of those periods even worse than January’s result, as shown in Exhibit 1.

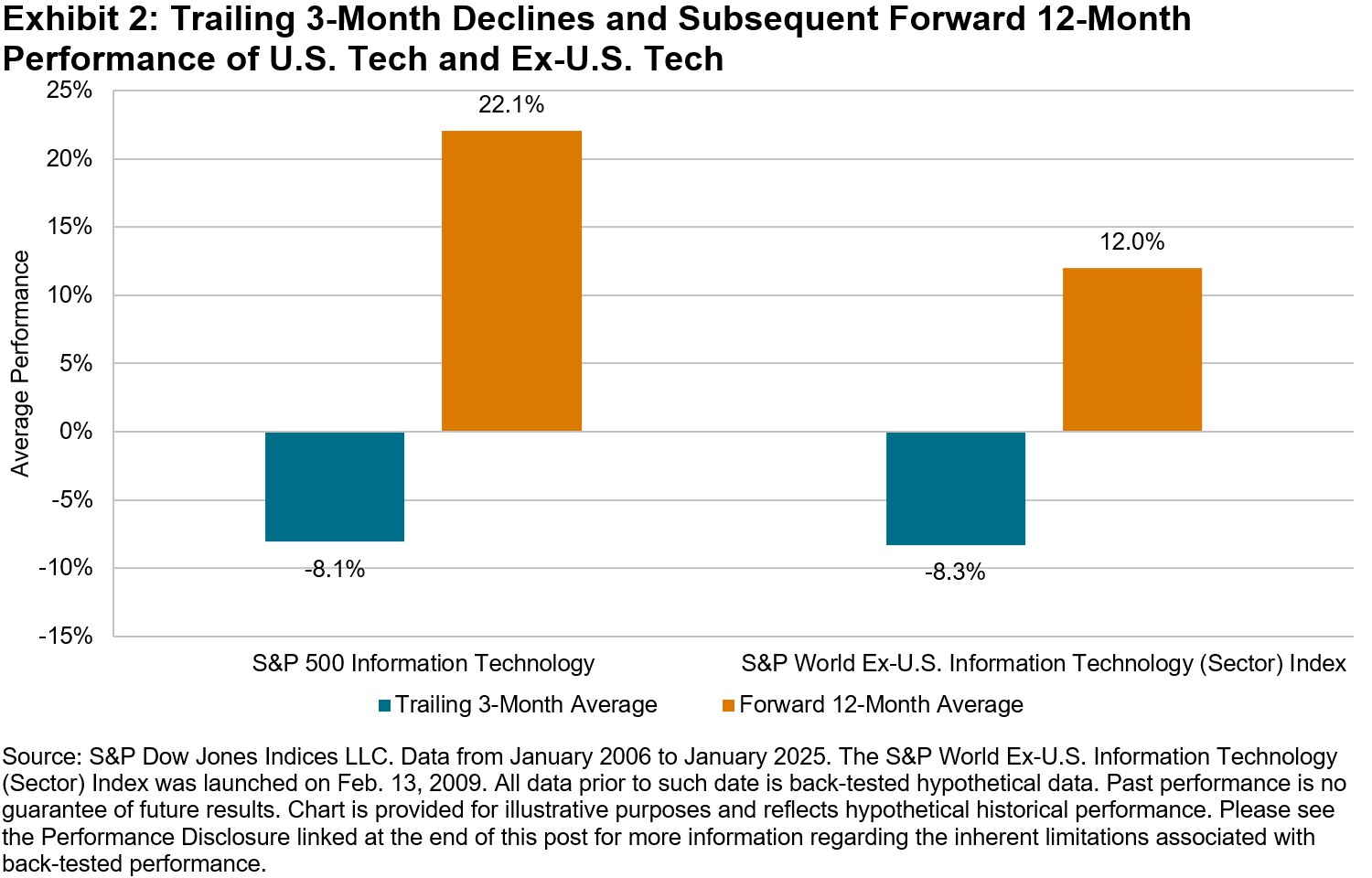

One might fairly ask what happened to U.S. Tech after previous three-month declines, and how its performance compared to the same sector around the rest of the world at those times. As it turns out, Information Technology showed resilience worldwide, but particularly so in the U.S. Exhibit 2 plots performance of two sector indices, the S&P 500 Information Technology and the S&P World Ex-U.S. Information Technology (Sector) Index (“Ex-U.S. Tech”) over 12-month periods after 3-month declines since January 2006. Following periods of three-month declines, U.S. Tech typically rebounded at a greater magnitude than did Ex-U.S. Tech, increasing an average of 22.1% over the subsequent 12 months and outperforming The 500 by 7.6%, while 3-month drops in Ex-U.S. Tech were followed by average total performance of 12.0% and 1.5% excess performance versus the S&P World Ex-U.S. Index.

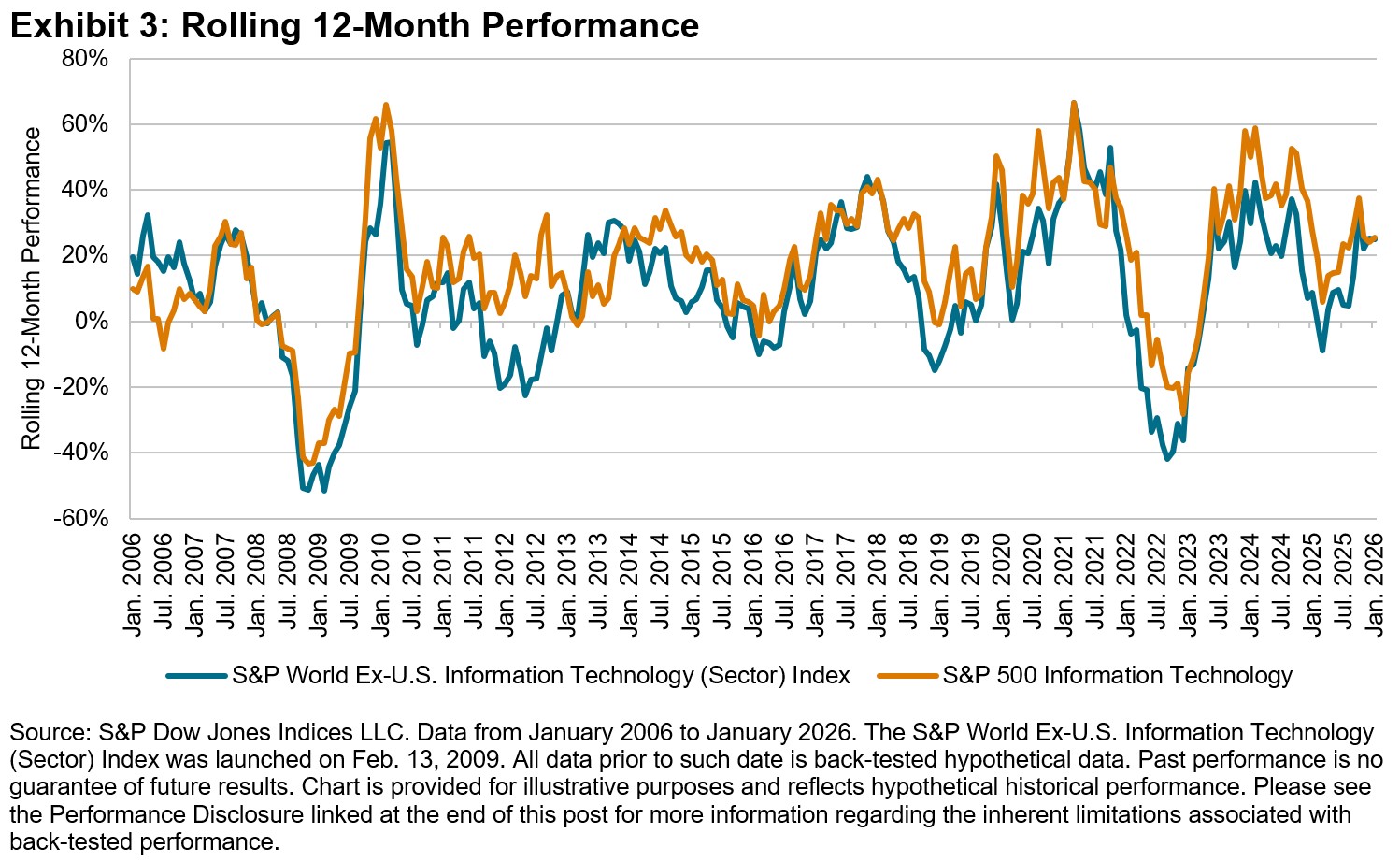

Shifting focus away from periods of decline and instead evaluating all periods in the last 20 years, we find that U.S. Tech often tended to lead its global counterparts. During 12-month periods when U.S. Tech was in an outperformance cycle relative to The 500, it simultaneously outperformed the rest of the world (as measured by the S&P World Ex-U.S. Index) 91% of the time, as shown in Exhibit 3. In such periods, U.S. Tech also generated higher performance than Ex-U.S. Tech 88% of the time.

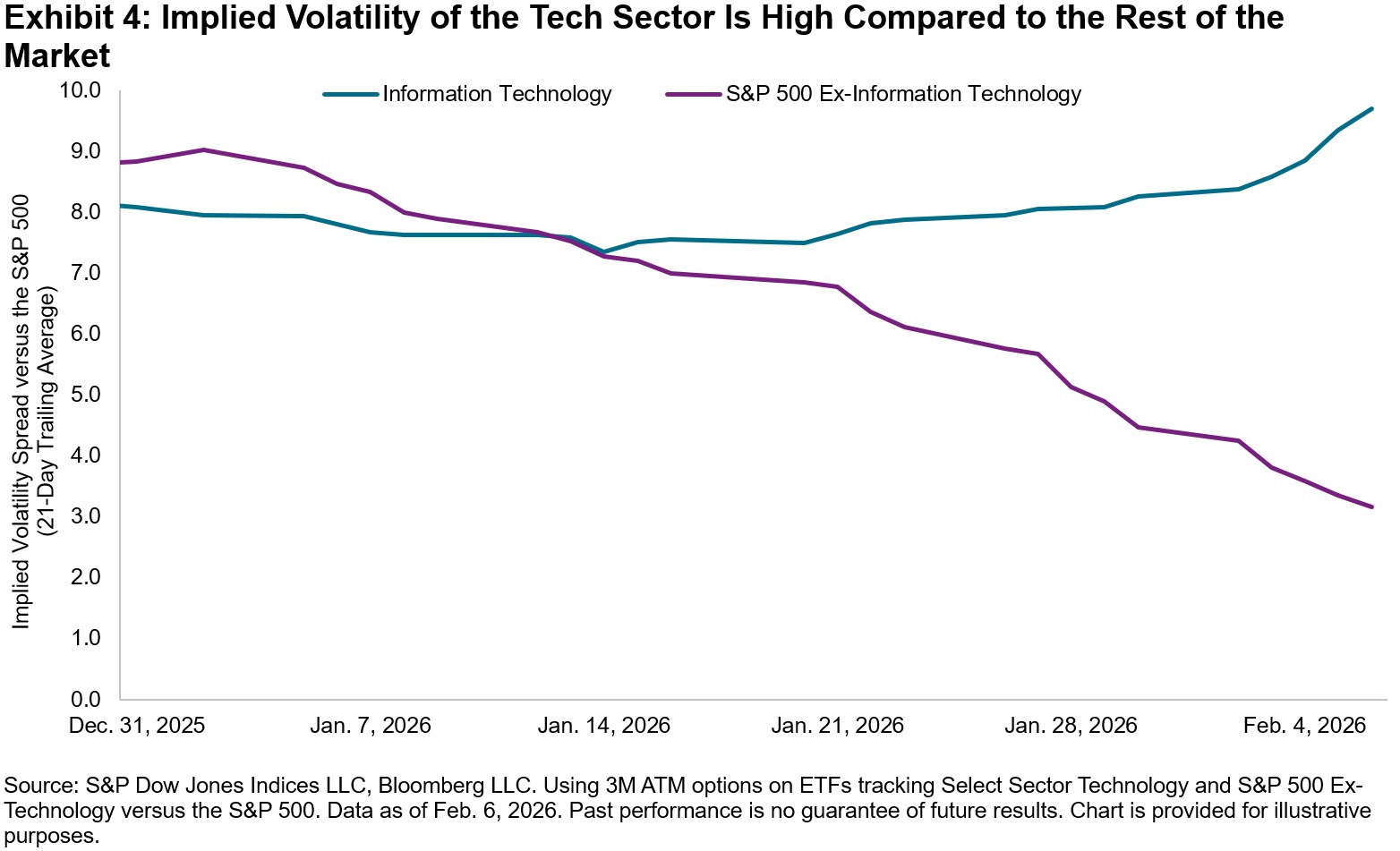

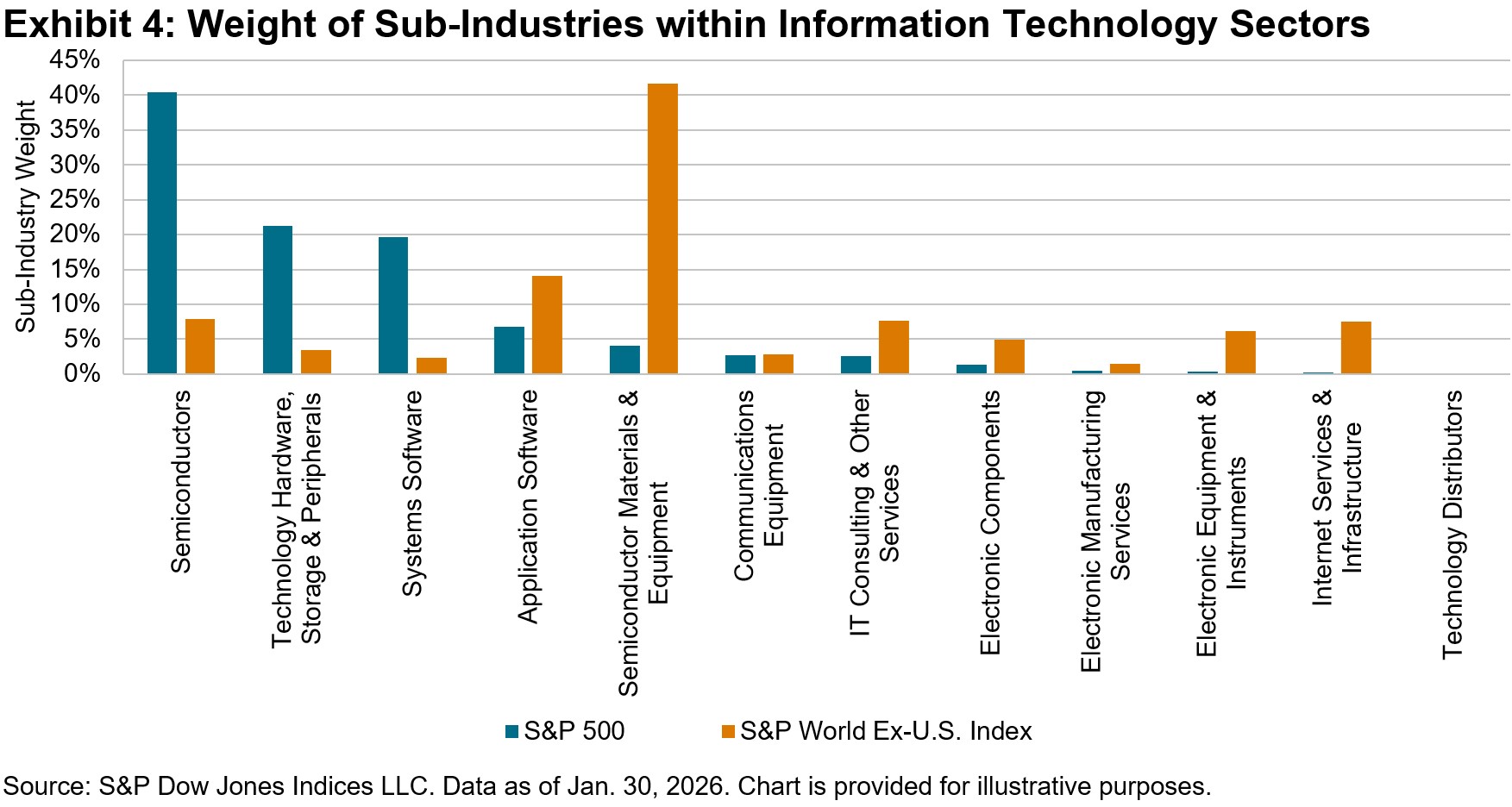

While sector membership explains a significant portion of constituent performance across different parts of the market and the economic cycle, variations in same-sector performance across geographies reveal the importance of understanding more granular constituent categorizations. In Exhibit 4, we begin to uncover potential drivers of U.S. Tech performance relative to its Ex-U.S. Tech counterpart, illustrating significant differences in GICS sub-industry weights. Specifically, the Semiconductors sub-industry comprised over 40% of U.S. Tech’s weight, yet only 8% of Ex-U.S. Tech’s, which held its largest weight (42%) in Semiconductor Materials & Equipment. Among the two sub-industries, Semiconductors significantly outperformed, aided by greater margins and pricing power for firms further down the AI chip value chain.

History has shown that periods of U.S. Tech underperformance have often been followed by periods of relative strength, and drivers of such sector resilience can be better understood through considering additional dimensions of geography and sub-industry composition. Like other sectors, Information Technology continues to evolve and reveal new clues that help to understand and navigate global markets.

Notes:

The S&P World Index comprises S&P World Ex-U.S. Index and S&P United States LargeMidCap.

The author thanks Tom Olins for his research contributions to this blog.

The posts on this blog are opinions, not advice. Please read our Disclaimers.