What Lies Beneath the Headline Names in the S&P 100?

Introducing the S&P 100 Ex-Top 20 Select Index, which measures the performance of companies within the S&P 100, excluding the largest 20 constituents ranked by float-adjusted market capitalization. This blog examines the depth, diversification and shifting leadership that can be obscured by the dominance of the very largest names.

The “Next 80” Make Up a USD 13.4 Trillion Segment

As shown in Exhibit 1, the companies outside the largest 20 make up a USD 13.4 trillion segment, over twice the size of Japan’s equity market and nearly four times larger than the U.K. market and the U.S. mid-cap segment (as measured by the S&P MidCap 400®). Far from a niche slice of the U.S. equity landscape, the “next 80” represent a major portion of the global equity opportunity set.

Beyond its global scale, comparing this segment with the S&P 100 offers additional insight. While the top 20 names often dominate market headlines, the remaining 80 companies represent a meaningful share of the mega-cap U.S. equity segment. Since 2001, these companies have accounted for approximately 45% of the S&P 100’s total weight on average, ranging from 32% to 56% (see Exhibit 2). This variability reflects shifts in mega-cap leadership and reinforces the concept of examining the “next 80” as a distinct lens.

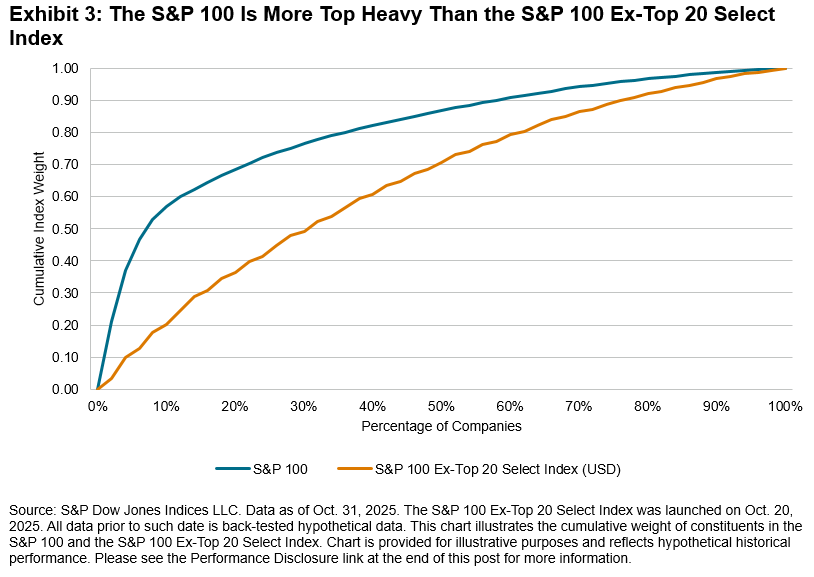

The S&P 100 Ex-Top 20 Select Index offers a more evenly distributed profile compared with the S&P 100, which is heavily concentrated in its largest names. Exhibit 3 shows that the top decile of constituents accounted for 55% of the S&P 100’s weight, versus about 22% in the S&P 100 Ex-Top 20 Select Index. This shows how steeply weight accumulates at the top of the S&P 100, highlighting the extent to which its performance can be driven by a relatively small set of names.

Broadening the Sector Profile

Differences in index size and constituent concentration are also reflected in sector weights. As shown in Exhibit 4, Information Technology represents nearly 25% of the S&P 100 Ex-Top 20 Select Index, well below the 42% weight in the S&P 100. This lower weight in Tech is paired with greater representation across other sectors, most notably Health Care (18%), Financials (17%) and Industrials (14%). Removing the largest 20 names resulted in a more balanced sector profile, reducing concentration in a few dominant sectors and broadening representation across the drivers of mega-cap U.S. equity performance. While the S&P 100’s Tech weight rose from about 20% in 2010 to over 40% in 2025, the S&P 100 Ex-Top 20 Select Index increased moderately from roughly 9% to about 20%. Meanwhile, sectors such as Health Care, Financials, Industrials and Materials had higher weights in the S&P 100 Ex-Top 20 Select Index.

Performance trends aligned with each index’s sector composition. The S&P 100 outperformed in recent years as concentrated mega-cap Tech leadership led performance, while the S&P 100 Ex-Top 20 Select Index tended to hold up better during periods when market leadership broadened.

Conclusion

The S&P 100 Ex-Top 20 Select Index offers a complementary lens on the S&P 100 by highlighting a large, diversified segment beyond the top 20 names. Its meaningful scale and broader sector mix provide additional perspective on the composition, concentration dynamics and long-term characteristics of the mega-cap U.S. equity landscape.

The posts on this blog are opinions, not advice. Please read our Disclaimers.